How to Invest in CDs: 3 Strategies

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

Key takeaways for CD investing

CD strategies involve opening multiple CDs to take advantage of different rates and term lengths.

A CD ladder is a common way to invest in CDs from short to long terms, usually staggering the end dates.

A CD barbell involves short- and long-term CDs without midrange terms, while a CD bullet consists of CDs of different terms that all mature around the same time.

When choosing a certificate of deposit, you might ask yourself — or the internet — whether you’re getting the best rate. After all, once you have a CD, you lock in that rate for months or years.

You can’t predict exactly what CD rates will look like in the future, but you can use strategies to reduce the risk of missing out when higher rates appear. At the same time, you still get the guaranteed returns and federal insurance that CDs offer.

Here’s a look at three main ways to invest with CDs.

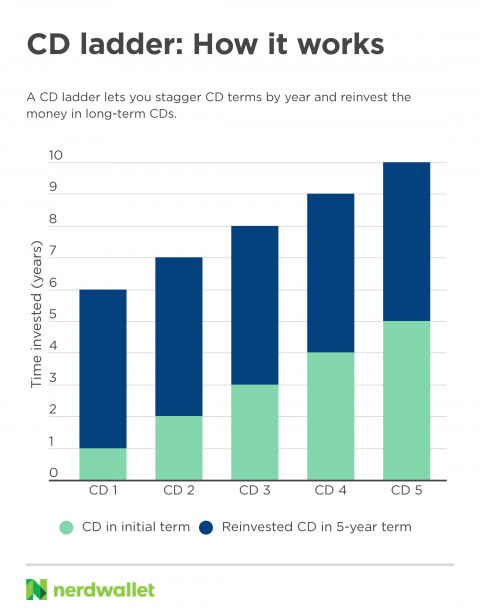

Strategy 1: CD ladder

A CD ladder consists of an investment divided up, usually in equal amounts, into multiple CDs of staggered term lengths. Each CD term is a rung of the ladder, and usually they’re equally spaced apart. When each CD matures, you reinvest in a long-term CD.

How it can work: Divvy up your investment — say $10,000 — into five CDs:

$2,000 in a one-year CD.

$2,000 in a two-year CD.

$2,000 in a three-year CD.

$2,000 in a four-year CD.

$2,000 in a five-year CD.

When the one-year CD matures, take that $2,000 plus the interest it earned and reinvest it into a five-year CD. Ideally, you repeat this until you have a five-year CD maturing every year. But if you need funds one year, you can opt to withdraw the next CD to mature, meaning you don’t renew or reinvest funds into a new CD. (While you can withdraw early from any bank CD, you’d likely be subject to an early withdrawal penalty.)

» Learn more about CD ladders, including mini-ladders and uneven splits

What a CD ladder is good for: A CD ladder lets you diversify across CD terms to take advantage of short-, midrange and long-term CDs. Typically the longer a CD term, the higher the rate. But if you stick with only long-term CDs, you lose access to that money for years.

Flipping the traditional trend, rates on one-year CDs lately have been higher than on five-year CDs.

A CD ladder provides a middle-of-the-road approach: regular access to some funds while earning long-term CD rates. Ideally, rates rise over time so you capture increasingly higher long-term rates, but if that doesn’t happen, a CD ladder still provides a solid mix of yields. A CD ladder can reduce the stress of trying to choose a CD at the right time.

What to remember: A CD ladder works best if you don’t withdraw money. Make sure you have an emergency fund before investing in CDs.

» Curious about past trends? See historical CD rates

Member FDIC

Barclays Online CD

5.00%

1 year

Member FDIC

Discover® CD

4.70%

1 year

Strategy 2: CD barbell

A CD barbell involves splitting an investment into short- and long-term CDs — the two ends of the CD spectrum — but no midrange terms. When the short-term CDs mature, you either reinvest in short- or long-term CDs, depending on whether rates across the industry have risen.

How it can work: Divide your investment, such as $10,000, into two CDs:

$5,000 into a six-month CD.

$5,000 into a five-year CD.

When the six-month CD matures, check on rates at various banks or, if applicable, your brokerage. If five-year rates have gone up, reinvest the money in a five-year CD. Or, if rates haven’t risen enough or at all, reinvest the $5,000 plus the interest it earned into another six-month CD. Half your funds might stay in short-term CDs awhile if rates stay flat or drop. Thanks to frequent maturities, though, you can choose to put that money elsewhere.

» Learn more about when to choose which CD term

What a CD barbell is good for: When you’re waiting for rates to rise, a CD barbell gives you frequent access to some cash until you’re ready to lock in for a longer term. You also hedge bets by taking advantage of current long-term rates. Generally the overall return tends to be an average of short- and long-term CDs.

What to remember: A CD barbell is less diversified than a CD ladder, which makes it riskier in the sense that you might miss out on higher rates in the future. You can put more money on the short- or long-term end of a barbell, but this might make sense only if you understand — or speak to a financial advisor about — how current financial markets impact the direction of CD rates. To keep things simple, you can start with equally weighted amounts on both ends of the barbell.

Strategy 3: CD bullet

A CD bullet strategy focuses on CDs that mature around the same date. If you open CDs over time, new terms will be shorter than the initial CD. Unlike with ladders or barbells, you don’t reinvest.

How it can work: Say you plan to buy a house in five years, so you put money in a five-year CD. Two years in, you can afford to put another chunk of money into a CD, and choose a new one that will mature around the same time as the initial CD. Four years in, you put more savings into another, much shorter CD. Once the fifth year ends, all CDs mature.

$10,000 in a five-year CD.

$5,000 in a three-year CD in the second year.

$5,000 in a one-year CD in the fourth year.

What a CD bullet strategy is good for: Usually you’ll use funds from CD bullets for a big expense, such as a wedding or down payment on a house. CDs tend to have higher rates than other bank accounts do, but most CDs don’t allow you to add money gradually. A CD bullet strategy can be a workaround: You can get shorter CDs over time, almost like a reverse CD ladder, to earn more interest on funds that you saved up since the initial CD.

What to remember: This strategy has more risk since you’re not reinvesting or diversifying across longer CD terms over time; your focus is on a future purchase. This risk refers to missing out on higher rates in the future, not losing money like you can when investing in stocks. In addition, many banks automatically renew CDs, so keep an eye on when your CDs mature to avoid missing your window of time to withdraw your money for free.

How to get started investing in CDs

Knowing the strategies can help you determine when and how many certificates of deposit will work for you. CDs are available at banks and credit unions as well as brokerages. (Brokered CDs work slightly differently than regular CDs.) If you need guidance on opening a CD, see this step-by-step guide.

Whichever strategy you choose, remember that CDs work as designed when they’re held until maturity. If you withdraw early from a bank CD, an early withdrawal penalty can cost you.

See CD rates by term and type

Compare the best rates for various CD terms and types:

How do CDs work?

Learn more about choosing CDs, understanding CD rates, and opening and closing CDs.

For choosing CDs:

For understanding CD rates:

For opening CDs:

For closing CDs:

See CD rates by bank

Here’s a quick list of CD rates at traditional and online banks and a brokerage:

On a similar note...