Does Applying for or Opening a New Credit Card Hurt Your Credit?

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

Opening, or simply applying for, a new credit card can temporarily ding your credit score. But getting a new card can also come with a few advantages for your credit, such as raising your credit limit. Here’s what to know.

Does applying for a credit card hurt your credit?

When a card issuer looks at your credit information because you’ve applied for a credit card, it is a so-called hard pull. That can lead to a slight drop in your credit score, whether you are approved or not. A new inquiry typically takes less than five points off your FICO scores, according to FICO.

A hard pull, or hard inquiry, stops impacting your credit score in a few months to a year, but it stays on your credit report for about two years. Your credit reports show inquiries. You can check your credit reports from each of the three major bureaus weekly for free at AnnualCreditReport.com.

Why does applying for a credit card hurt your score?

Statistically speaking, a new application can represent more risk for the card issuer. The impact is greatest if you have just a few accounts or a short credit history. A relatively small portion of your credit score (whether the dominant FICO score or its rival, VantageScore) is determined by how recently you have applied for credit.

Does opening a new credit card hurt your credit?

Applying for a new card can cause your score to slip a bit, but opening a new card and using a lot of that line of credit can result in a bigger drop. Getting a new card can also negatively impact your score if you have only one or two other cards, and they are only a few years old, because it will decrease the average age of your credit.

Here’s how opening a new card might hurt your credit:

It can lead to higher balances

A new credit card might hurt your score if you make a big purchase or get a balance-transfer card and transfer your higher-interest debt to the card so that you have high credit utilization. The amount of your credit limit that you use is weighted heavily. Credit utilization is calculated both per-card and overall.

Experts recommend going no higher than 30% on any card, and lower is better.

However, it’s smart to look at overall finances, not just your credit score. Accepting a drop in your score due to high credit utilization because you got a 0% balance transfer card deal to pay off debt may be worth it.

It may lower the average age of your accounts

How long you’ve had credit also affects your score. Your new card can reduce the average age of your credit. If you have few credit cards, it will have a bigger impact than if you have many.

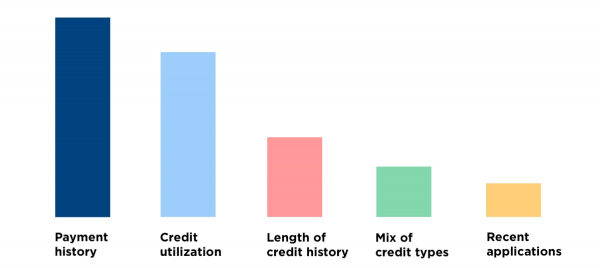

Length of credit history, however, is a relatively minor factor in credit scores. It counts as 15% of your FICO score. VantageScore lists “depth of credit,” the age of your credit accounts, as making up 21% of your VantageScore 3.0 score.

How opening a new card can help your credit

A new line of credit can also help your credit profile.

It can give you a better track record

Paying on time, every time is essential for good credit. Payment history accounts for 35% of FICO credit scores, the ones most commonly used in credit decisions. Competitor VantageScore says it makes up 40% of your 3.0 score.

If you’re trying to build credit, nothing is more important than consistent, on-time payments. A new account gives you another opportunity to build up a record of on-time payments.

It gives you more room on credit cards

A new card will increase your overall credit limit. If your spending stays the same, your overall credit utilization will be lower, and that could help your score.

It can create credit diversity

Credit scores award points for showing you can manage more than one type of credit. If you have an installment loan but do not have an existing credit card, successfully managing your new credit card is likely to help. But if you already have several credit cards, adding one more is not as likely to have much of an impact.

Before you apply for a credit card

Consider these factors:

Whether your application is approved or rejected makes no difference in your score. That’s why it makes sense to be almost certain you will qualify before you apply. You don’t want to lose points and still not have the credit you needed.

Applications can affect people’s credit differently. For example, an applicant with a high credit score and a long history of on-time payments is unlikely to lose as many points as someone with a lower score and a shorter, imperfect track record.

Points lost as a result of credit applications are likely to return in about six months. So if you are planning to apply for a loan for, say, a car or home, it’s a good idea not to apply for any other credit for at least six months before that loan’s final approval.

Want to try out a few scenarios about applying for credit and how it might affect your score? As part of NerdWallet’s free credit score tool, you can use the credit score simulator to estimate the effect of various actions.

When you apply for a credit product that involves a hard inquiry on your credit, you may get an influx of marketing messages from lenders. This happens because credit bureaus sell marketing lists triggered by hard inquiries. But you can opt out, either permanently or for five years. Visit OptOutPreScreen, a service of credit bureaus Equifax, Experian, TransUnion and Innovis, or call 888-567-8688. The bureaus say your request will be effective within five days. Note that you may still receive marketing offers from lenders that use other sources. Opting out does not affect your credit score or your ability to apply for credit or insurance.