What Is a Credit Limit? Credit Limit vs. Available Credit

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

You’ve applied for a credit card and were approved (congrats!), but that doesn’t mean you have unlimited spending power.

It’s important to know your card’s credit limit, which is the maximum amount you can spend on your card. Also important: your available credit, which is the limit minus your current balance. These numbers both play a big role in your credit score.

What is a credit limit and where can you find it?

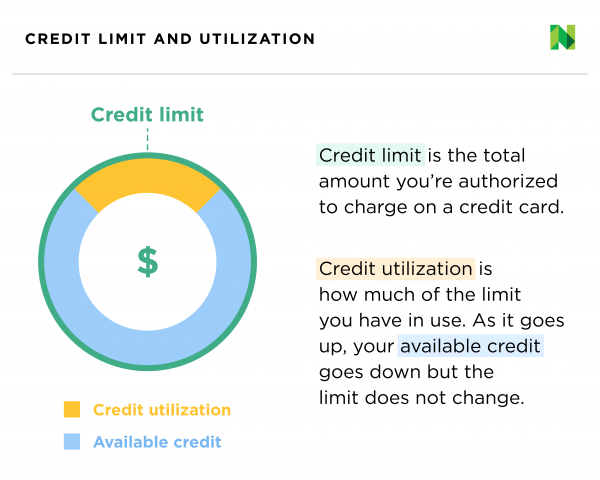

Your credit limit is the total amount of charges you’re authorized to make on a credit card. When you apply for a credit card, the lender will examine elements of your financial history and determine your credit limit, or the maximum amount you’re allowed to borrow.

If you're unsure where to find your credit limit on a new or existing credit card, you can try looking in a few places, including your online account or monthly statement.

What factors determine your credit limit?

When determining your credit limit, the lender considers a range of factors, including:

Your payment history, or the record showing whether you’ve paid your bills on time and if you’ve missed any payments.

Your credit score, a number from 300 to 850 that indicates your creditworthiness to potential lenders.

Your income, which is one way lenders assess your ability to pay back the money you’re lent.

Your credit utilization, or how much of your current credit limits you’re using.

What is available credit?

Your available credit is the amount that's left once you subtract your balance from your credit limit on any given card. For example, say your credit limit is $1,000 and you paid the balance in full last billing cycle. If you’ve spent $300 this billing cycle, you still have $700 in available credit before you hit your limit. But it’s important to note that “maxing out” your credit card is not recommended, because it will damage your score.

If you pay off your credit card in full, the available credit resets back to $1,000. But if you sometimes carry a balance on the card, keep your credit limit in mind so that you don’t suffer credit score damage or get into debt too difficult to recover from.

Credit limit and your credit score

Knowing your credit limit is important because credit utilization — how much of your credit limits you're using — is a major factor in your credit score.

There's no downside to keeping your credit utilization ratio low; in fact, the best credit scores tend to go to people using very little of their limits. But if you use too much of your credit, you could be viewed by potential lenders as a higher risk, which could complicate the process of applying for things like a car loan or home loan.

A good guideline is the 30% rule: Use no more than 30% of your credit limit to keep your debt-to-credit ratio strong. Staying under 10% is even better.

In a real-life budget, the 30% rule works like this: If you have a card with a $1,000 credit limit, it’s best not to have more than a $300 balance at any time. One way to keep the balance below this threshold is to make smaller payments throughout the month.

You can calculate your credit utilization per card or overall.

Pros and cons of increasing your credit limit

Credit limits don’t always stay the same across the life of your account since your finances will also change over time. It’s smart to assess whether it’s a good time to ask for a credit limit increase. You might be primed to ask for a credit increase if you’ve recently gotten a raise, have good credit or have a proven track record of making payments on time.

However, before you ask for the credit limit increase, there are some pros and cons to consider.

Pros of a higher credit limit:

It offers more flexibility in your budget.

It will shrink your overall credit utilization ratio if you don’t stack up a balance. And lower utilization will help your credit score. Calculating that ratio before you start the conversation is a good idea.

Cons of a higher credit limit:

It allows you to spend more and potentially rack up debt that is difficult to pay off.

The credit check often used to confirm eligibility could ding your credit score. Ask your card issuer if it will bump up your limit without a hard inquiry on your credit.

If you decide to move forward with the request after weighing the benefits and potential pitfalls, you can request a credit increase through a few avenues. The easiest way is to simply ask, usually through your online banking portal or by phone.

What if you spend more than your credit limit?

If you make a charge that puts you over your approved credit limit, your credit card may be declined. If you exceed your credit limit frequently, your lender may take actions including canceling the card, cutting rewards or lowering your limit.

And you'll likely be doing great harm to your credit score.

Why does your credit limit matter?

Your credit limits are a key piece of your financial portfolio. Keeping your spending at 30% of your credit limits or below is one strategy to improve your credit. Knowing your credit limits — and planning how much of them to use — is also a way you can avoid overspending and going into debt.

There are other ways to manage your credit to make sure it’s healthy. Paying your bills on time is essential to keeping your credit score strong, and setting up automatic payments is one strategy that can help. Mixing up the kinds of credit you have, paying attention to the average age of your accounts (a long record of responsible credit usage is a good thing), and spacing out your credit applications are good ways to keep your credit healthy.