View details

Monthly fees

$47 and up

Service fees

$75–$100

per claim

States available

49

states, and Washington, D.C.

View details

Some or all of the mortgage lenders featured on our site are advertising partners of NerdWallet, but this does not influence our evaluations, lender star ratings or the order in which lenders are listed on the page. Our opinions are our own. Here is a list of our partners.

A home warranty is a contract that covers the cost of select household repairs or replacements, up to certain caps. These plans cover damages due to "normal wear and tear," which is the expected deterioration that happens over time with everyday usage. Damages from other causes, such as natural disasters or lack of maintenance, are excluded.

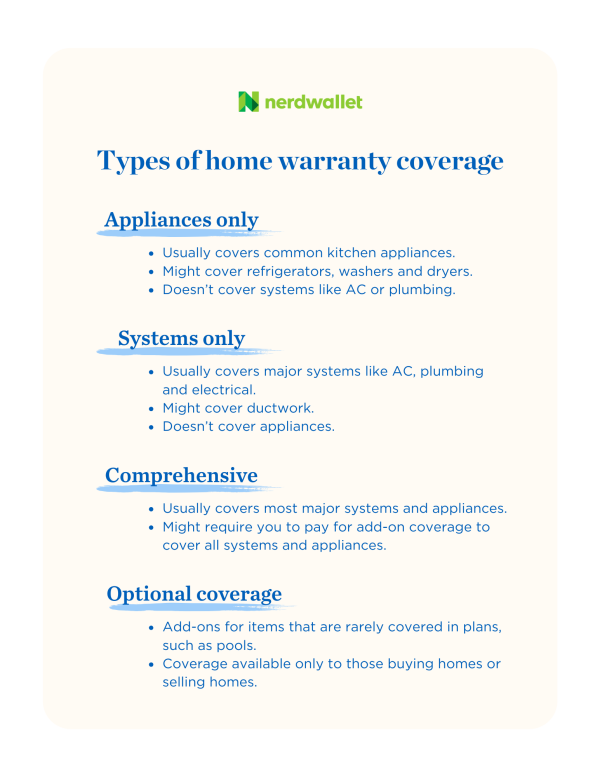

Comprehensive plans cover both systems (such as heating, electrical and plumbing) and appliances (such as refrigerators, ovens and dishwashers). Many providers also offer systems-only and appliance-only options.

Systems-only plans generally cover:

Heating.

Cooling.

Electrical.

Plumbing.

Water heaters.

Appliance-only plans generally cover:

Oven/range/stove/cooktop.

Dishwasher.

Washer and dryer.

Built-in microwave.

Garbage disposal.

Garage door opener.

Most home warranties allow you to pay more for additional coverage. A few examples of commonly available add-on items include:

Pool.

Septic pump.

Well pump.

Limited roof leak repairs.

on Choice Home Warranty's website

Check your service agreement, the contract associated with your home warranty, to find out what your policy covers. This contract outlines what the company will and won’t pay for and additional terms, such as when coverage begins.

Importantly, these documents list exclusions — appliances, systems and parts that aren’t covered by the warranty and in which situations an item might be denied coverage. Review exclusions carefully to understand what type of coverage you’re getting.

A sample service agreement for a home warranty from Select Home Warranty.

Service agreements list the service fee you need to pay for each claim filed — generally ranging from $75 to $100 — and coverage limits, which cap how much the company will pay to repair or replace a particular item. For example, if your oven fails and your policy has a $500 limit for repairs or replacement, you will pay out of pocket for any costs over that $500 limit.

Home warranty vs. homeowners insurance. Where a home warranty helps repair the appliances and systems in your house due to routine wear and tear, homeowners insurance covers your physical house when damages occur from events like fires or theft. Your home warranty may cover a malfunctioning dishwasher, but for coverage of secondary damages — like a buckled floor after your faulty dishwasher leaks — you'd need to rely on your homeowners insurance coverage.

While a home warranty plan may help pay to repair or replace a specific system or appliance, it doesn't cover everything that can go wrong with that item. Every provider's contract contains exceptions and exclusions to their coverage. For example, your plan's contract may cover plumbing stoppages, but those due to roots located outside of the home's structure may be excluded.

Home warranties also might not guarantee parts or equipment of the same brand, color or size for repairs or replacements. So while your appliances or systems might get fixed or replaced, you could end up having a mismatched kitchen or bathroom.

Here are some things home warranties typically don't cover:

Areas outside the main part of the house, such as underground pipes or sewer lines, unless you've specifically added them into your coverage, as with coverage for a pool or septic tank.

Homes larger than 5,000 square feet; you'll likely have to pay more for this coverage.

Pre-existing conditions or problems that began before you purchased the warranty. This can include any negative items found during a home inspection or indicated in the seller's disclosure as well as issues that you were unaware existed before a repair was started.

Sprinkler systems and outdoor plumbing, though you may be able to purchase coverage for an additional fee.

Repair of structural parts of a new construction or remodeled home, like walls, floors and plumbing (which would be covered by a builder warranty).

Systems and appliances that have been improperly maintained and installed.

Recalled items or any systems or appliances covered under another warranty.

Properties that are used as a commercial business, such as a bed-and-breakfast or day care.

Coverage for more than one of the same appliance or system; you'd need to pay extra to cover an additional refrigerator or dishwasher, for example.

Cosmetic damages, such as dents or scratches, and damages from pests like termites.

Coverage varies depending on the provider, and you should check your contract to learn what specific situations are excluded from coverage.

Still under manufacturer’s warranty? If most of your appliances and systems are still covered by the manufacturers’ warranties, you might want to wait to get a home warranty. Plans generally don’t cover items until after the manufacturer warranty expires.

» LEARN MORE: What does a new home warranty cover?

The good news is that, yes, a home warranty often will pay to replace an appliance or system if a repair won’t fix a problem that affects its functionality. But most home warranty contracts state that the amount paid for replacement can be less than what you’ll have to pay to purchase a new one.

For example, if a dishwasher needs to be replaced, you might spend $1,000 on a new one but only get reimbursed for $500. And even if you were able to buy a replacement for $500, the reimbursement amount might not include additional funds for taxes, shipping or installation. In this case, you could end up paying for a chunk of the replacement on your own.

There are several reasons a home warranty company might deny your claim, and most of them are likely outlined in your service agreement. These include things like:

The item not being included in your chosen plan.

A malfunction due to improper maintenance, installation, or modification of the item.

The item being located in a structure used for business purposes.

Damage or malfunction caused by weather-related events such as floods or fires.

Failure of an item because of damage caused by pests, such as termites, or pets.

Your previous claims reaching the limit on how much the company will pay toward repairs.

On a similar note...