How to Choose a Cash-Back Credit Card

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

Choosing a cash-back card sounds easy: Pick the one that gives you the most money back, right?

Sure. But to figure that out, you need to consider:

What’s the card’s cash-back rate, sign-up bonus and annual fee, if any?

How much hassle will you endure to get more cash back?

Answers to those questions will determine which card is best for you. If you want to skip directly to NerdWallet’s picks, see our best cash-back credit cards. Otherwise, let's get into it.

Be sure cash back is right for you

If you’re already sure, skip to the next section about deciding on the types of cash-back cards. Otherwise, here are benefits and drawbacks of cash-back cards:

Pros of cash-back cards

Cash back cards are so popular because they’re easy to understand, and the main benefit comes in the most useful rewards currency: dollars (as opposed to points or frequent-flyer miles.)

Using a cash-back card is like getting paid to spend money that you were going to spend anyway. Or put differently, it’s an automatic discount on whatever you buy with the card. Big spenders can easily earn hundreds of dollars per year in cash back.

Cash back comes in different forms, depending on your card. Typical options are:

A statement credit (making your next credit card bill lower).

A deposit into your bank account.

A mailed check.

Most cash-back cards don’t charge an annual fee.

» LEARN: How cash-back credit cards work

Cons of cash-back cards

The main downside of cash-back cards is you can't strategize to get outsized value, like plotting to use airline miles for a first-class ticket that would otherwise cost thousands of dollars. And they come with fewer perks than you’ll find on higher-end cards — no airport lounge access or free hotel nights.

Like all rewards cards, cash-back cards are best for those who pay off their monthly balances in full. Paying interest on balances will wipe out the value of your cash back.

Decide which type of cash-back card you want

Cheat sheet for choosing a cash-back card type

Flat-rate: Lowest hassle, lower cash-back rate (but on everything you buy).

Fixed bonus categories: Medium hassle, higher cash-back rate on some purchases.

Changing bonus categories: High hassle, highest cash-back rate on some purchases.

Flat-rate credit cards

Choose a flat-rate cash-back card if simplicity is paramount. You’ll get the same rewards no matter what you buy or where you buy it, even on your trash-pickup bill and doctor copayment.

A slew of cards offer 1.5% cash back on every purchase. Buy anything on your card for $100, and you get $1.50 back for free. Some even pay 2% or more. With many flat-rate cards, you can earn an unlimited amount of cash back.

A good example is the Citi Double Cash® Card. It earns an unlimited 2% cash back: 1% back on every dollar you spend, then another 1% cash back for every dollar you pay off.

Charge $15,000 to a 2%-back card in a year, and you’ll earn a total of $300 cash back.

Compared with bonus-category cards, detailed below, here are typical advantages and disadvantages of flat-rate cards.

Pros:

Simpler.

Unlimited cash back.

Higher than 1% back on everything.

Cons:

Lower cash-back rate on some spending.

Lower sign-up bonus, if any.

Bonus-category credit cards

Choose a bonus-category card if you’re willing to invest some effort to get a higher rate of cash back for purchases at some places — restaurants, grocery stores or gas stations, for example — and less, typically 1% back, everywhere else. (Issuers know where you bought something based on the transaction’s merchant category code. That’s how they know to apply a higher cash-back percentage to a purchase.)

Bonus-category cash-back cards come in two main flavors: Bonus categories that stay the same and those that change.

Fixed categories

These cards offer a higher rewards percentage for spending in certain categories, such as gas or groceries, and a lower rate — usually 1% — on all other purchases. The categories don’t change, although some cards limit the rewards you can earn in a given category.

An example of a fixed category card is the Blue Cash Preferred® Card from American Express. It earns 6% cash back at U.S. supermarkets on up to $6,000 a year in spending (then 1%); 6% cash back on select U.S. streaming subscriptions; 3% cash back at U.S. gas stations and on transit; and 1% cash back on all other purchases. Terms apply (see rates and fees).

Fixed-category cards are more complicated than flat-rate cards, but at least you know the bonus categories are always the same.

Changing categories

These cards are the most complicated because they not only have bonus categories to remember, but those categories also can change. Sometimes the issuer changes them — and you might even have to “activate” the categories every quarter to earn the bonus rate. Sometimes you can choose to change the categories, picking from a list.

The payoff for dealing with that hassle? The cash-back rate for bonus categories can be very high, like 3% to 5%.

For example, with the Discover it® Cash Back, you’ll earn 5% cash back in rotating quarterly bonus categories on up to $1,500 in combined spending per quarter (once you activate), and 1% cash back on all other purchases. Bonus categories in the past have included things like restaurants, grocery stores, gas stations, Amazon.com and more.

Compared with flat-rate cards, here are typical advantages and disadvantages of bonus-category cards.

Pros:

Higher rewards rates on some purchases.

More likely to have a sign-up bonus.

Cons:

Complicated.

Low 1% cash back on non-bonus categories.

Cash-back credit cards for small businesses come in the same types: flat-rate, fixed bonus categories and changing categories.

In choosing a type of card, know yourself. Are you a person who will use credit cards strategically? (And if others in the household use the same card, will they use it strategically?)

If you don't remember to use the right card for specific purchases, the higher rewards rate on a bonus-category card may not pay off. And you might do better overall with a flat-rate card.

Narrow your list

After you know which type of cash-back card is right for you, choose based on these criteria to get the most cash back:

Cash-value considerations

Reward rates and category spending

High rates for certain categories are great, but all categories aren't created equal. Consider how much you spend in the category regularly.

For example, you’re likely to earn more cash back if your card offers 3% back on supermarkets rather than a larger 5% on streaming video services. That’s because you spend more at the supermarket than on streaming. And you probably earn a lowly 1% back on everything else. That’s the allure of a good flat-rate card: you get more than 1% back on everything you buy with it and don’t have to think about bonus categories, just the rate of cash back.

Minimum goals:

Flat-rate cards: At least 1.5% back.

Bonus-category cards: At least 3% back in a high-spend category.

New-cardholder bonus

A one-time cash bonus is nice because it essentially boosts your rewards in the short term if you can meet the required spending to earn it. But the rewards rate is more important over the long term. A card without a bonus could still be the right one for you.

Annual fee

This is usually zero, because annual fees aren’t common on cash-back cards, unless they offer an especially lucrative cash-back rate. And some do. If a cash-back card has an annual fee, it has to be so good that it easily makes back that fee every year. Think of it as a reduction in your annual cash-back total.

One way to compare the monetary value of cards is to examine them over three years, using the factors above. Figure your annual cash back on a card for three years, add any sign-up bonus and subtract three years of annual fee. That’s how much richer you’ll be for using the card over that time.

Complexity

But hypothetical monetary value isn’t everything. Consider how complicated one card is versus another. That will mostly be decided by the type of card — flat-rate cards are easier to use than bonus-category cards.

But cards in the same category can offer different hassles. For example, some cards with excellent cash-back rates come from credit unions. In applying, are you willing to join a credit union? It could be worth it, but it’s an extra step. Or sometimes, the cash-back tiers of bonus categories are so convoluted that you won’t use the card optimally because it’s a hassle.

The main benefit of choosing a cash-back card is that it’s supposed to be simpler than, say, airline, hotel and luxury travel cards. Don’t discount the importance.

Other considerations

As a tie-breaker, maybe you consider other features of a card, like whether it charges foreign transaction fees, whether it comes with a 0% introductory APR or from an issuer you already like — Chase, American Express or Discover, for example.

Optional: Choose cash-back cards for a multi-card strategy

A multi-card strategy allows you to earn more cash back by using two or more cards together. Choose:

Bonus-category card(s) to earn accelerated cash back on certain purchases.

Flat-rate card for everything else.

In choosing cards, the advice is the same. Pick bonus-category cards based on where you spend a lot of money and cash-back rates. Then, choose a flat-rate card for all other spending. That way, you’re not stuck with a lowly 1% for the “everything else” spending.

Examples of excellent cash-back credit cards

See a full list of NerdWallet’s best cash-back credit cards.

Flat rate

With the Wells Fargo Active Cash® Card, you’ll earn 2% cash back on all purchases.

Annual fee: $0.

Sign-up bonus: Earn a $200 cash rewards bonus after spending $500 in purchases in the first 3 months.

With the Citi Double Cash® Card, you’ll earn 1% cash back every time you spend, then an additional 1% cash back when you pay your purchases off.

Annual fee: $0.

Sign-up bonus: Earn $200 cash back after you spend $1,500 on purchases in the first 6 months of account opening. This bonus offer will be fulfilled as 20,000 ThankYou® Points, which can be redeemed for $200 cash back.

Bonus categories

For best categories

The Blue Cash Preferred® Card from American Express earns 6% cash back at U.S. supermarkets on up to $6,000 a year in spending (then 1%); 6% cash back on select U.S. streaming subscriptions; 3% cash back at U.S. gas stations and on transit; and 1% cash back on all other purchases. Terms apply.

Annual fee: $0 intro annual fee for the first year, then $95.

Welcome bonus: Earn a $250 statement credit after you spend $3,000 in purchases on your new Card within the first 6 months. Terms Apply.

For best categories with no annual fee

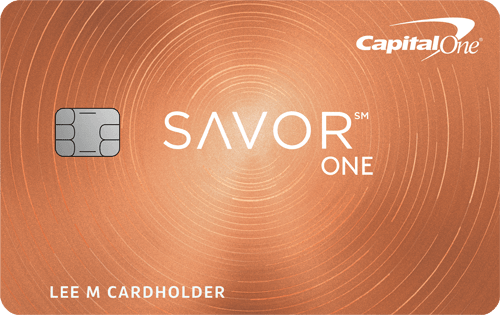

The Capital One SavorOne Cash Rewards Credit Card offers 3% cash back on dining, entertainment, popular streaming services and at grocery stores (excluding superstores like Walmart and Target), plus 1% on other purchases.

Annual fee: $0.

Sign-up bonus: Earn a one-time $200 cash bonus after you spend $500 on purchases within the first 3 months from account opening.

High-rate tandems

If you’re willing to juggle two cards:

With the Discover it® Cash Back, you’ll earn 5% cash back in rotating quarterly bonus categories, up to $1,500 spent per quarter (requires activation). You’ll also earn 1% cash back on all other purchases.

Annual fee: $0.

Sign-up bonus: INTRO OFFER: Unlimited Cashback Match for all new cardmembers – only from Discover. Discover will automatically match all the cash back you’ve earned at the end of your first year! There’s no minimum spending or maximum rewards. You could turn $150 cash back into $300.

With the Citi Double Cash® Card, you’ll earn 1% cash back every time you spend, then an additional 1% cash back when you pay your purchases off.

Annual fee: $0.

Sign-up bonus: Earn $200 cash back after you spend $1,500 on purchases in the first 6 months of account opening. This bonus offer will be fulfilled as 20,000 ThankYou® Points, which can be redeemed for $200 cash back.

If you want cards from the same issuer — so you can see your accounts on a single app or webpage:

The Chase Freedom Unlimited® earns at least 1.5% cash back on everything you buy.

The Chase Freedom Flex℠ earns 5% cash back on bonus spending categories that rotate quarterly, on up to $1,500 in combined spending each quarter (activation required); all non-bonus-category purchases earn 1% back.

Both cards earn 5% back on travel purchased through Chase and 3% on dining and at drugstores.

Some cards technically earn points that can be used as cash back. We generally consider them to be cash-back cards if you can redeem points for 1 cent each.

You found the best cash-back credit card. What’s next?

Choosing the best cash-back credit card for you is an accomplishment, but don’t stop there. Use your card the right way to get the most out of it. To rack up the most rewards, use the card for everyday purchases and pay your bill in full every month. If you’re using more than one cash-back card, maximize rewards by using the right card at the right merchant.

Find the right credit card for you.

Whether you want to pay less interest or earn more rewards, the right card's out there. Just answer a few questions and we'll narrow the search for you.