USAA Mortgage Review 2024

Some or all of the mortgage lenders featured on our site are advertising partners of NerdWallet, but this does not influence our evaluations, lender star ratings or the order in which lenders are listed on the page. Our opinions are our own. Here is a list of our partners.

- 50+ mortgage lenders reviewed and rated by our team of experts.

- 40+ years of combined experience covering mortgages and financial topics.

- Objective, comprehensive star rating system assessing 120+ categories and 5,000+ data points.

- Governed by NerdWallet's strict guidelines for editorial integrity.

Our Take

4.0

USAA specializes in VA loans, but other purchase and refinance options are available, too. USAA membership, which includes perks and a full suite of financial products, is open only to current and former military and eligible family members.

Pros

- VA loans are the bulk of USAA's business, so its loan officers know the ins and outs of eligibility and the application process.

- Offers HomeReady loans, a conventional mortgage with flexible down payment options for low- and moderate- income buyers.

- Has a highly rated mobile app.

Cons

- Offers a limited selection of loans apart from VA, including no FHA or USDA loans.

- Doesn’t offer home equity loans or lines of credit.

- Only sample mortgage rate information is on the USAA website. For customized rates, you have to make contact.

Lender | Min. credit score | Min. down payment | |

|---|---|---|---|

620 | 0% | Visit Lenderat Veterans United at Veterans United | |

620 | 0% | Visit Lenderat NBKC at NBKC | |

580 | 0% | Visit Lenderat Guaranteed Rate at Guaranteed Rate | |

580 | 0% | Visit Lenderat Rocket Mortgage, LLC at Rocket Mortgage, LLC | |

600 | 0% |

Full Review

What borrowers say about USAA mortgages

NerdWallet’s lender star ratings assess objective qualities, including rates, fees and loan offerings. To assess borrowers’ subjective experiences with lenders, NerdWallet has gathered customer satisfaction ratings from J.D. Power and Zillow.

USAA received a score of 797 out of 1,000 in J.D. Power’s 2022 U.S. Mortgage Origination Satisfaction Study. The industry average for origination was 716. (Mortgage origination covers the initial application through closing day.) USAA was not included in J.D. Power's 2023 Mortgage Origination Satisfaction Study.

USAA receives a customer rating of 3.55 out of 5 on Zillow, as of the date of publication. The rating reflects just 77 customer reviews.

USAA’s mortgage loan options

2 of 5 stars

If you’re actively shopping for a VA loan, USAA has likely made your list of mortgage lenders to compare. VA loans, backed by the U.S. Department of Veterans Affairs, don’t require a down payment and aim to make homeownership achievable for military members and families.

USAA is one of the country’s largest providers of VA loans. It offers standard and jumbo VA purchase loans. The lender also offers VA refinances for standard and jumbo amounts, including cash-out refinances and interest rate reduction refinance loans (known as a VA IRRRL). This range of VA loan options sets USAA apart from other lenders we’ve reviewed.

To get a mortgage with USAA, you have to enroll as a member. USAA membership is open to U.S. military members and honorably discharged veterans, as well as their spouses. Children of USAA members are also eligible to join.

Even though membership is exclusive to the military community, USAA’s offerings aren’t limited to VA loans. Conventional fixed-rate purchase loans and refinances are also available. USAA offers a low-down-payment purchase loan for first-time home buyers, defined as someone who hasn’t owned a home in the past three years, as well as HomeReady loans from Fannie Mae.

However, USAA falls short in that it doesn’t offer other common mortgage types. Government-backed FHA and USDA loans are not available, and neither are second mortgages such as home equity loans or lines of credit. USAA mortgages are available in all 50 states and D.C., but cash-out refinances are not available in Texas.

» MORE: Best VA mortgage lenders

What it’s like to apply for a USAA mortgage

4 of 5 stars

USAA is a members-only organization, so before you can apply for a mortgage, you’ll need to enroll as a member. If you aren’t already a USAA member, and you qualify, you can sign up online in a quick, do-it-yourself process.

Members can access a range of products from USAA, including banking and auto insurance. Additionally, USAA provides financial advising services designed for the unique needs of the military community. USAA membership is free and comes with additional perks such as discounts on shopping, travel and entertainment.

Once you’re a member, USAA offers a fully online mortgage application as well as other digital services, such as loan application tracking, document upload and e-signatures.

For a non-member, the options to research USAA’s mortgage offerings are somewhat limited. To measure the lender’s responsiveness to early-stage mortgage shopping questions, we called the USAA customer service line. Our call was answered immediately by a bot that provided menu options. After answering a series of mortgage eligibility questions, we were prompted to transfer to an agent who could assist with signing up as a USAA member.

USAA has a handful of branches for in-person service. Primarily, the lender assists customers remotely through the website or by phone during extended hours on weekdays. The website has an itemized list of international contacts for USAA, which would be especially helpful to those who are deployed. The lender also offers a highly rated mobile app.

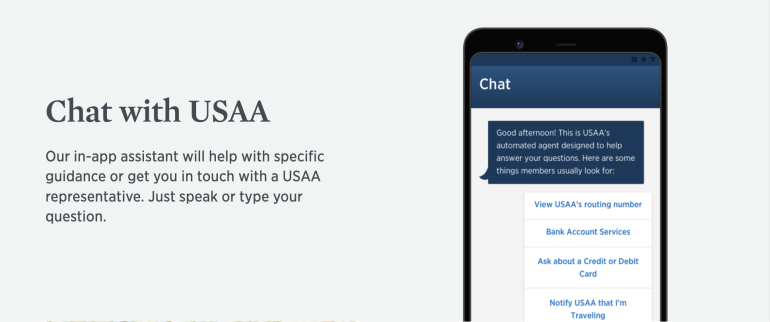

A virtual assistant chatbot is available through the website or mobile app.

This, too, is helpful mainly to members. When beginning a chat without being logged in, you’re required to select from a menu of common customer questions that apply to members or prospective members. NerdWallet issues the highest scores to lenders that make online chat available to anyone, including those in the early research stages who might not be ready to make an online account.

» MORE: How to apply for a mortgage

USAA’s mortgage rates and fees

3 of 5 stars

USAA mortgage earns 3 of 5 stars for average origination fee.

USAA mortgage earns 3 of 5 stars for average mortgage interest rates.

NerdWallet analyzes federal data to compare mortgage lenders’ origination fees and offered mortgage rates. We measure annual averages across all loan types, as reported by the lenders. USAA’s rates and fees are about average, compared to other lenders’.

Borrowers should consider the balance between lender fees and mortgage rates. While it's not always the case, paying upfront fees can lower your mortgage interest rate. Some lenders will charge higher upfront fees to lower their advertised interest rate and make it more attractive. Some lenders just charge higher upfront fees.

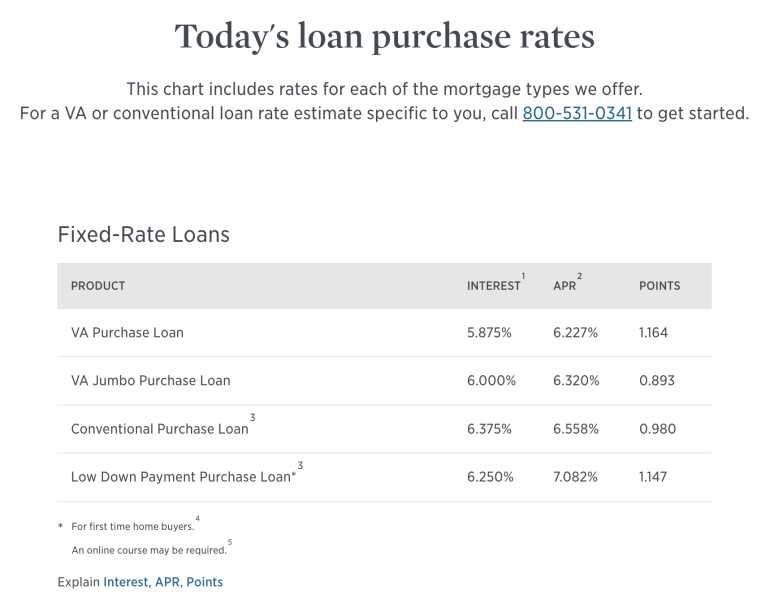

USAA’s mortgage rate transparency

4 of 5 stars

The USAA rates web page shows sample mortgage rates for purchase and refinance products. A few considerations are noted, such as APR and whether discount points have been applied to lower the displayed rate.

On the public-facing website, it’s not possible to customize a rate quote with your credit score, location, estimated down payment or other loan details. To get a customized rate quote, you'll need to contact a USAA loan officer or start an online application. An 800 number is clearly displayed to begin the process.

Alternatives to USAA mortgage

Here are some comparable lenders we review that borrowers can consider.

Navy Federal Credit Union also issues a large volume of VA loans, and servicemembers who have exhausted their VA benefit might consider their Military Choice Loan. Veterans United exclusively offers VA loans and has a highly rated mobile app.

» MORE: Best online mortgage lenders

Explore mortgages today and get started on your homeownership goals

Get personalized rates. Your lender matches are just a few questions away.

Bella Angelos contributed to this review.

More from NerdWallet

NerdWallet’s overall ratings for mortgage lenders are evaluated based on four major categories: variety of loan types (purchase, refinance, fixed and adjustable, for example), ease of application, rates and fees and rate transparency. Among the factors we consider when scoring these categories are options to apply for and track loans online, the level of detail about mortgage rates on lender websites and our analysis of the rates and fees lenders reported in the latest available Home Mortgage Disclosure Act data. These scores generate ratings from 1 star (poor) to 5 stars (excellent).