Your Credit History Opens Doors — Here’s How to Build It

Many, or all, of the products featured on this page are from our advertising partners who compensate us when you take certain actions on our website or click to take an action on their website. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

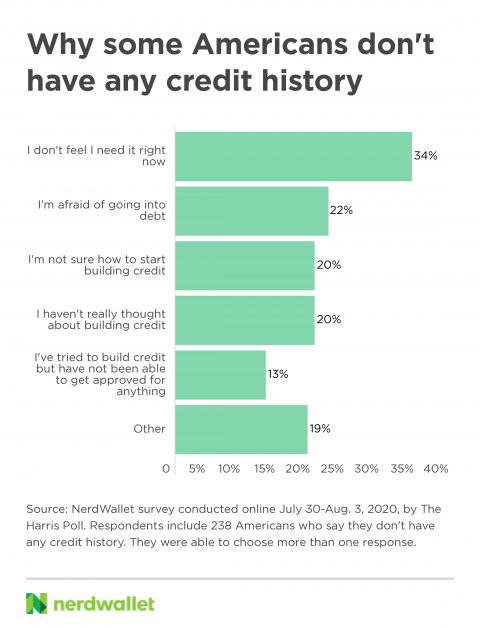

Around 1 in 8 Americans (13%) say they don’t have any credit history, according to a NerdWallet survey. They provided a variety of reasons: Some haven’t even thought about building credit, others want to do it but can’t gain traction and some are in the middle.

Building credit is wise for just about everyone, but it’s not something you can do overnight. It may take around six months for positive credit actions to have an impact on your credit score, so waiting until you’re ready to buy a house or finance a car is too late.

Even if such things aren’t in your plans, having good credit (or credit scores of 690 or higher) still expands your financial options. And while building credit isn’t always easy, it’s not as complicated as many people think.

Build credit before you need it

Among Americans without a credit history, about one-third (34%) say it’s because they don’t feel like they need it right now. And 1 in 5 (20%) say it’s because they haven’t really thought about building credit.

Building credit is about preparing for the future, and good credit means having more choices, like qualifying for loans and credit cards with better terms and lower interest rates. But the effects go well beyond your ability to borrow money — something many Americans may not know.

A good credit score can make it easier for you to rent an apartment. It can determine the kind of cell phone plan you’re eligible for, qualify you for lower auto insurance rates and allow you to get utility service without having to provide a security deposit. Many employers now check applicants’ credit, so your score can even affect your ability to earn a living.

Debt isn’t required to build credit

Close to a quarter of Americans who say they don’t have a credit history (22%) say it’s because they’re afraid of going into debt.

Being wary of debt is understandable. But you don’t have to go into debt to build credit; you just need to show a track record of making payments.

Credit card debt is notoriously expensive — but only if you carry a balance from one month to the next. And there's no need to carry a balance to build credit. By paying your bill in full by the due date each month, and you’ll never be charged interest.

If you’re concerned about overspending, use the card only for specific recurring expenses, then set up an automatic payment from your bank account each month. For example, instead of using a credit card for daily expenses and possibly running up debt, put your monthly power bill or streaming subscription on the card. That way you aren’t spending more than you would otherwise, but you’re still building credit and avoiding interest.

How to get started

According to the survey, 20% of Americans without credit history say it’s because they aren’t sure how to start building credit. And 13% say they’ve tried to build credit but haven’t been able to get approved for anything.

A well-known catch-22 of credit-building is that good credit allows you to borrow money, but you need to be able to borrow money to establish good credit. You can start building credit by becoming an authorized user on someone else’s credit card or by getting your own secured card.

Become an authorized user

An authorized user is added to another person’s credit card account and benefits from that primary cardholder’s good credit habits. So if you have a parent, partner or someone else with good credit who's willing to add you to one of their credit card accounts, you can start building credit without getting approved on your own. Before you go this route, have the primary cardholder confirm with the credit card issuer that it reports credit activity for authorized users to the three major credit bureaus, Equifax, Experian and TransUnion.

Get a 'starter' credit card

Another option is a secured credit card, which you can get on your own if you have a few hundred dollars for a deposit. Here’s how it works: You put down a cash deposit, then you get a card with a credit limit that's usually equal to your deposit. You use the card like any other credit card, making purchases and paying your bill on time every month. Unlike with a prepaid card, your account activity is reported to the credit bureaus. Once you’ve built up your credit, you can close the account, get a regular card (or upgrade to one, if the issuer offers it) and get your original deposit back.

For more, read NerdWallet’s guide on how to build credit, which covers getting started with credit-building, practicing good credit habits and tracking your progress by monitoring your credit report.

Find the right credit card for you.

Whether you want to pay less interest or earn more rewards, the right card's out there. Just answer a few questions and we'll narrow the search for you.