What to Consider Before Closing Your Travel Credit Card During the COVID-19 Crisis

Many, or all, of the products featured on this page are from our advertising partners who compensate us when you take certain actions on our website or click to take an action on their website. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

» This page is no longer being updated.

COVID-19 presents both a health and a financial crisis, and during such a difficult time, you may be looking to cut expenses you see as discretionary. Since you probably won't be traveling soon (or as much), that might include a travel credit card with an annual fee.

Closing a credit card you don’t need is fine in some circumstances, especially if it carries an annual fee and the anniversary date is looming. However, it’s not completely without risks. Closing a card may adversely affect your credit in a time when you might need it more than ever. And in some cases, your credit card company can even claw back the points you’ve earned.

If you’re on the fence about whether you should keep or cancel your travel rewards credit card, here are a few things to consider.

The downsides to closing a credit card

Credit experts often suggest you shouldn’t apply for more credit than you need, but that’s not the same as cutting down on the credit you already have. The latter can harm your credit scores because of a metric called your utilization rate (or utilization ratio).

The utilization rate is the ratio of your card’s balance to your total credit line. This figure is used by both FICO and VantageScore, two major credit scoring companies, to determine your creditworthiness. If you have several credit cards, you can use a calculator to find your credit utilization ratio.

Experts usually advise keeping the utilization rate (both per card and of your overall credit) under 30%. But this is a general guideline; the lower your rate, the better. VantageScore bluntly states that the "optimal ratio always will be as close to zero percent as possible," although it leaves a possibility of having "elite credit scores with higher ratios."

So if you thought your only job was to pay your bills on time, that’s not quite true. To FICO, the utilization rate is second in importance only to payment history, while to VantageScore it’s the most influential factor.

This is why it’s crucial to know where you stand before closing your account. Let’s say you have three cards with credit limits of $2,000 each. If you cancel one of them, you’re slicing one-third of your total credit, which has now shrunk to $4,000. That can be unsettling even in normal times — but especially now, when emergency spending is more likely and can contribute to a utilization rate increase.

On the other hand, if you carry several cards for a total balance of $20,000 and keep a utilization rate of 10% or 15%, then closing one low-limit card should be OK.

The point is, having a good credit score affords easier access to new credit should the need arrive, which is especially important at a time of crisis when lenders are likely to tighten approval standards.

» Learn more: Does closing a credit card hurt my credit score?

Ask about annual fee credits or retention offers

Sometimes a solution to your problem is one phone call away. Just tell the agent that you’re thinking of canceling the card because times are rough and you don’t have an immediate need for the card.

If your account is in good standing, they might offer to reduce the annual fee or waive it rather than see you go. Or they might try to entice you with a retention offer including a points or miles bonus. You’ll never know unless you try.

However, if you carry a balance on your card, you might want to ask them to lower your annual percentage rate instead. That approach could work out even better than getting the fee waived.

» Learn more: How to get a lower APR on your credit card

But be careful — some issuers are quick to close your card immediately upon such a request. To avoid that, tell them you would like to speak to the retention department. And be patient, because wait times on the phone may be longer than usual right now. Also, though it may go without saying, try to be unfailingly polite even if they say no.

» Learn more: How and when to ask for a retention offer

See if promotional offers could offset the annual fee

Many travel rewards credit cards come with an annual fee, ranging from a reasonable $49 up to a hefty $550 or even more. For frequent travelers, or even those who take only a few trips a year, the benefits that come with the cards generally make the annual fee worth it.

Even if you’re not traveling right now, you may be able to find value from the card in other ways. Many cards offer coupons and exclusive offers that could save you enough money to justify keeping the card.

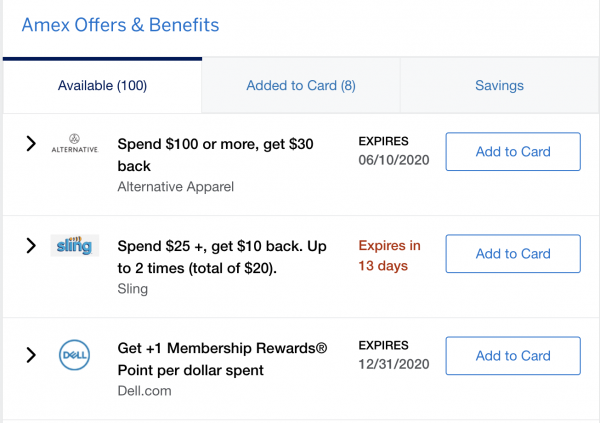

American Express Offers

If you have an American Express card, you have the opportunity to add AmEx Offers to it. Log into your AmEx account and scroll down the page until you see the "AmEx Offers and Benefits" section.

You’ll see a list of merchants with various offers that you can add to your card. Some will save you cash — just click to add the offer to your card, then use that card to pay for your transaction at that merchant. If you meet the requirements of the offer, you’ll get cash in the form of a statement credit back on your account.

Other offers will earn additional Membership Rewards points above what you’d earn normally for using the card.

The offers available to you may be different from offers your family or friends receive. Add as many offers as you like; there’s no obligation to use them. If you have multiple AmEx cards, even though you may see an offer available on several of them, you’ll only be able to use each offer on one card.

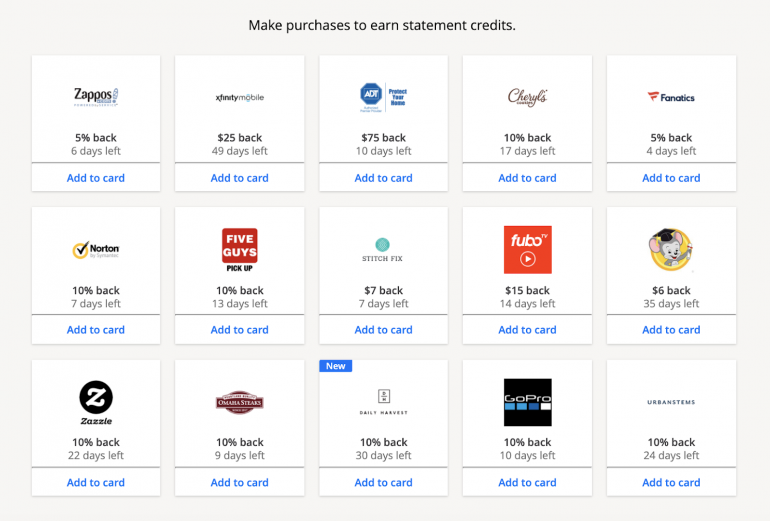

Chase Offers

Chase also has an array of rotating offers you can add to your card. Sign in to your Chase account, and you’ll see offers you can activate on your cards.

Chase Offers are newer on the scene and not quite as robust as the offerings you’ll find on AmEx. These offers typically earn cash back on your statement instead of extra points.

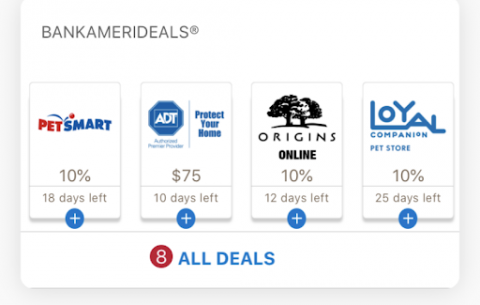

BankAmeriDeals

You can find special offers and deals on your Bank of America credit cards, too. Just scroll down the page when you’re logged in and you’ll see a list of BankAmeriDeals that are available to add to your card.

Like Chase Offers, these deals are cash-back offers that will be credited to your statement after you pay. Make sure you’re spending enough at that merchant to meet the requirement for the offer, and don’t forget to use the card you added the offer to when you check out.

Special bonus rewards and statement credits

In the coronavirus pandemic, a number of travel credit cards feature special extras for a limited time. Many cards have increased bonuses for the money you spend on groceries, while others are giving statement credits for streaming services, cell phones and electronics purchases.

Here are a few of the special bonuses offered by various cards: (You can find our detailed lists here and here.)

Up to $320 in statement credits on the The Platinum Card® from American Express for streaming services like Netflix and Spotify and for wireless phone services through Dec. 2020.

3x-12x per dollar spent on groceries, depending on the credit card.

The ability to use annual hotel and resort credits toward any U.S. restaurant purchase.

Check out the offers for the cards you carry and factor those savings into the bigger picture when you’re deciding to keep or cancel the card. Watch out for other special, limited-time offers that may crop up on your specific card.

Ask for a product change to a no-annual-fee card

If you don’t care about keeping the same card, you can ask for a product change. In most cases, your credit card company will be happy to offer you a downgrade to a no-annual-fee card with the same credit line. Problem solved.

Before you do this, make sure your credit card company won’t claw back your points if you cancel or downgrade. Read your cardmember agreement or call the issuer to ask what happens if you cancel or change the card.

In most cases, a credit card company won’t take back your airline miles or hotel points, but with credit cards’ own rewards programs (like Citi ThankYou, Chase Ultimate Rewards® or AmEx Membership Rewards) things can get a little more complicated.

Some credit card programs may have different product-changing stipulations, so make sure you understand the implications and can protect your points. They may take you far when planes lift into the skies again.

Consider if you will be able to get the card back

If you’re thinking about canceling the travel rewards credit card you have now, but then want to reopen it later when you’re ready to travel, your plans might be foiled.

Chase, which has arguably one of the best portfolios of travel credit cards around, has an (unofficial) policy that could make it hard for you to get a "new" card when you’re ready, even if you had it before. It’s called the 5/24 rule, and it means that in order to be approved for a Chase credit card, you must have fewer than five approvals for credit cards in the last 24 months.

For example, let’s say you closed your Chase Sapphire Preferred® Card now and opened several cards that earn cash back instead. If you wanted to reopen a Chase Sapphire Preferred® Card again next year but you were over five cards in 24 months (from any issuer), you’d likely be denied.

Even if you’re not affected by the 5/24 rule, there’s always a chance that your favorite travel card won’t be available for new applicants, you wouldn’t qualify for a welcome offer or the bank may enforce a longer waiting period before you can get it again.

Make sure you are aware of your 5/24 count, review the issuer policies on timing rules related to welcome bonuses and gather information about reapplying for your specific card before you make a decision to cancel.

» Learn more: Chase 5/24 rule explained

Will closing the card leave you with "orphan" miles?

Thanks to flexible points programs, it’s easy to transfer points to many different airline and hotel reward accounts. You can transfer your flexible points into your airline or hotel account if you need more points to reach the award you want to redeem them for. If your airline or hotel points were close to expiring, in many cases, you could transfer flexible points to generate account activity and keep them from expiring. Or, if you found an irresistible deal and wanted to transfer your points, you could do so in a few clicks.

Keep in mind that not all airline and hotel rewards programs have transfer partners. Take American Airlines, for example. While it does have a variety of co-branded credit cards to choose from, it doesn’t partner with any flexible programs like Chase, American Express or Citi.

Let’s say you close your American Airlines credit card. Once it’s safe to travel again, you find an amazing Web Special award but you don’t have enough American AAdvantage miles to book the trip for your whole family. You won’t be able to generate more AAdvantage miles by spending on your credit card (because you closed it), and you won’t be able to transfer any flexible bank points into your account. Sure, there are other ways to earn more miles, but it may not be as easy if you no longer have the credit card.

The bottom line

Closing your travel rewards credit card in the coronavirus pandemic may be the right decision for you. Before you close it, consider the fact that you may not be able to reopen it down the line or that you may be able to get more value to cover the annual fee than you realize.

If there’s an option to downgrade your card to a different version, that could end up being a better plan. You may also qualify for a retention offer when you call to chat about your options with the issuer.

The information related to the Citi Prestige® Card has been collected by NerdWallet and has not been reviewed or provided by the issuer or provider of this product or service.

How to maximize your rewards

You want a travel credit card that prioritizes what’s important to you. Here are some of the best travel credit cards of 2024:

Flexibility, point transfers and a large bonus: Chase Sapphire Preferred® Card

No annual fee: Bank of America® Travel Rewards credit card

Flat-rate travel rewards: Capital One Venture Rewards Credit Card

Bonus travel rewards and high-end perks: Chase Sapphire Reserve®

Luxury perks: The Platinum Card® from American Express

Business travelers: Ink Business Preferred® Credit Card

on Chase's website

1x-5x

Points60,000

Points

on Chase's website

1.5%-5%

CashbackUp to $300

2x-5x

Miles75,000

Miles