What Is a FICO Score? Here’s What You Need to Know

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

Your FICO score is a number typically on a 300 to 850 range used by lenders to determine your ability to pay back borrowed debt.

FICO defines a good credit score as 670 to 739.

Payment history and amounts owed are the two biggest factors that impact your FICO score.

You have multiple FICO scores because scoring models are updated every few years, and there are industry-specific FICO scores for auto lenders and credit card products.

Paying your bills on time, utilizing less than 30% of your available credit and having a variety of credit types will help build your FICO score.

What is a FICO score?

A FICO score is a three-digit number, typically on a 300 to 850 range, that tells lenders how likely a consumer is to repay borrowed money based on their credit history. FICO also offers industry-specific scores for credit cards and car loans, which range from 250 to 900.

The name derives from the Fair Isaac Corp., which introduced the FICO score in 1989.

The terms “credit score” and “FICO score” are often used interchangeably, but there are other brands of scores, including VantageScore, which is FICO's biggest competitor.

Why is a FICO score important?

Your FICO credit score is important because it determines the kinds of rates and terms you can get on financial products such as a car loan or a mortgage. For example, a score that is in the good or excellent range can give you more choices and access to lower interest rates. Your credit score may also be used by utility companies and landlords to determine your deposit or whether you'll be accepted as a tenant.

What is a good FICO score?

FICO defines a good score as 670 to 739. Generally, scores from 690 to 719 are considered good credit. But each lender or credit card issuer can decide what score is needed to qualify for a particular line of credit.

How is a FICO score calculated?

The company applies a proprietary formula to the data in your credit reports to produce a score.

What factors affect your FICO score?

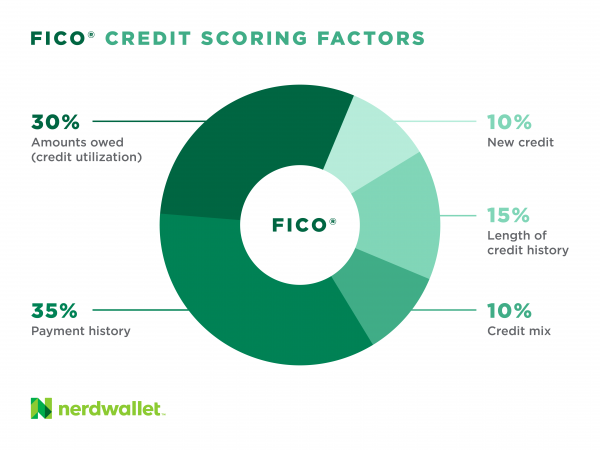

While FICO doesn’t reveal its exact scoring formula, it gives useful guidelines about the factors that matter for scores. Paying on time and keeping balances low account for about two-thirds of your score:

Payment history (35% of your score): Paying your bills on time is key for earning an excellent score. Late payments can really hurt your score, as can accounts in collections or a bankruptcy.

Amounts owed (30%): Also known as credit utilization, this is how much of your available credit you are using. Ideally, try to use 30% or less of your available credit.

Length of credit history (15%): This refers to how long you’ve had credit and the average age of your credit accounts.

New credit (10%): A so-called hard inquiry when you apply for new credit can nick your score for up to six months. That's why it's important to research credit card offerings and eligibility requirements before applying for one.

Credit mix (10%): Having both installment loans (those with level payments, like a car loan or mortgage) and revolving credit (like a credit card) can help your score.

Why do my FICO scores vary?

The three main credit bureaus that create your credit reports — Equifax, Experian and TransUnion — have slightly different data from one another. So your score may vary depending on which bureau's data was used.

What is a FICO score used for?

Creditors often use FICO scores to decide whether to approve an application for a loan or a credit card. It gives them a picture of how you've handled credit in the past. They also check other information, such as your income and existing debt obligations, to see whether you have the means to repay them.

FICO 8 is the most widely used among lenders

FICO scores are one type of credit score (VantageScore being another), but you can also have multiple versions of a FICO score. FICO 8, introduced in 2009, is the most widely used, while FICO 9 as well as FICO 10 and FICO 10T are newer versions.

UltraFICO, launched in 2018, is a scoring model meant for people new to credit or looking to rebuild credit. UltraFICO links with your checking and savings accounts to provide a bigger picture of your financial habits.

FICO is the go-to for mortgage lenders

FICO says it is used by 90% of “top lenders,” and it's favored by the law in one crucial spot: home mortgages. Right now, it’s the only tool to evaluate credit risk that is approved for use by government-sponsored enterprises such as Fannie Mae and Freddie Mac.

Although mortgage lenders typically use much older FICO score versions, they will begin adopting FICO 10T over the course of the next few years. This comes after a 2022 decision by the Federal Housing Finance Agency to approve the use of FICO 10T and VantageScore 4.0 for loans sold to Fannie and Freddie.

Although implementation of these two scoring models will take "a multiyear effort" to coordinate, the benefits are expected to be significant, especially for minority home buyers.

FICO vs. VantageScore

VantageScore was developed jointly by the three major credit bureaus and introduced in 2006. It is gaining traction with both consumers and lenders.

How do I get a FICO score?

You may already have access to a free FICO score on your credit card statement or banking app. Some credit card issuers such as Bank of America and Discover give customers free FICO scores monthly.

You can also pay to get a FICO score via the company’s own website. It costs $29.95 per month to get your FICO scores from all three credit bureaus, along with other kinds of information like your FICO automotive score. If you're preparing for a big purchase, like a car or home, it might be worth it to subscribe for one month, check your reports and then cancel. That way, you'll be walking into the lender's office without any surprises.

Many personal finance websites, including NerdWallet, offer a free credit score from VantageScore, FICO's main competitor. That gives you another option for watching your score. VantageScores tend to track similarly to FICO scores, because both weigh many of the same factors and use the same data from the credit bureaus.