720 Credit Score: Is It Good or Bad?

Many, or all, of the products featured on this page are from our advertising partners who compensate us when you take certain actions on our website or click to take an action on their website. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

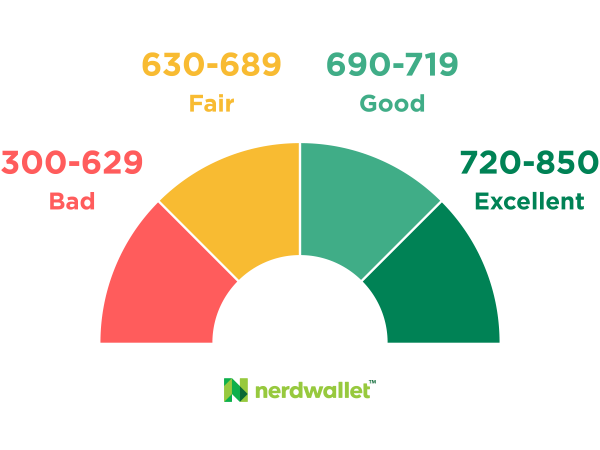

A 720 credit score on the common credit scoring range of 300-850 is right at the border of “good” and “excellent.” In fact, when your score hits 720, you’ve just crossed over into the excellent score band. That’s great news, unless your score was higher and you’re worried about what a loss of points might mean.

If your 720 credit score is cause for celebration, keep in mind that scores fluctuate as new data flows into your credit reports. If your score has plunged to 720 because of, say, a late payment, you may no longer be eligible for the very best terms on financial products. Because your score is at the dividing line between excellent credit and good credit, you probably want to wait until you're more firmly in the excellent category before you apply for credit. With your 720 score, here’s how you compare:

A 720 FICO score is slightly better than the average FICO 8 score, which was 717 as of October 2023, up one point from a year earlier, according to FICO. A 720 score is significantly better than the average of 700 on the VantageScore 3.0 model, as of October 2023, up six points from a year before. You are in the excellent credit range, which is 720-850. But any drop in your score could move you back to the good credit range of 690-719.

What a 720 credit score can get you

Good or excellent credit can help you get better terms (like a lower interest rate) on loans, and may also be a requirement for apartment rental or for lower or no deposits when you have utilities connected.

Score is not the only factor, though. Creditors are also interested in how much credit experience you have. For example, a 720 credit score that comes primarily from someone else's credit cards that you were added to as an authorized user in the last year is not going to be quite as reassuring as a 720 credit score that comes from several years of solid payment history, where you were responsible for paying. Creditors may also consider such things as how much disposable income you have to cover a new payment, or your overall debt-to-income ratio.

Adding points to your score can give you more options. A score above 750 could help you qualify for 0% financing on cars and 0% introductory interest rates on credit cards.

That said, here are some things you might be able to get with a 720 credit score:

Car loans

A 720 credit score is in an area that credit bureau Experian describes as “prime,” but it’s well short of “superprime,” which begins at 781. You will pay more in interest on a car loan than someone with a higher score. Recently the difference was more than a full percentage point higher for new and used car loans. That’s a significant difference, and the rates are worse for lower scores. Your 720 credit score is lower than the average new-car buyer’s score of 735, but higher than the typical used-car buyer’s score of 675.

Home loans

Assuming you have enough income, a 720 credit score is likely high enough to help you get a government-backed mortgage such as an FHA for VA loan. However, it’s probably not high enough to get the lowest interest rates available.

Credit cards

A 720 credit score is going to look pretty good to most credit card issuers. The top-of-the line rewards cards may be out of reach, but you’ll likely be able to qualify for decent cards with rewards or cash back.

Personal loans

A 720 credit score will likely give you a choice of personal loans. It’s not a guarantee, though, because lenders look at many factors to arrive at a decision on approval.

Strategies to keep building your 720 credit score

If your score moved up to 720, you’ll probably see continued improvement from the momentum you’ve established by paying on time and keeping balances low. But if your score seems stuck at 720, or if its general direction is down, there are ways to address this.

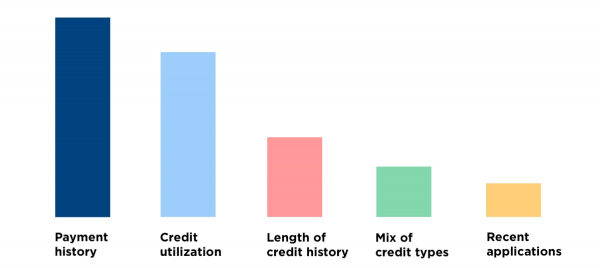

Understanding what information in your credit reports has the biggest impact on your credit is a good place to start.

The tried-and-true ways actually do work. Here’s how to build your score.

Pay on time

A late payment can do some serious damage, and most credit scoring formulas are designed to hold a grudge. A late payment can damage your score, and the later it is, the worse the damage. Neglecting this will negate just about anything else you do to try to improve your credit.

Use credit lightly

If the amount you owe on your credit cards is anywhere close to your credit limits, your credit score will take a dim view of it. The best thing you can do is keep balances under 30% and pay them off in full. If you can’t do both, keep balances of all cards under 30%. This factor is called credit utilization, and it is a major contributor to your credit score.

Apply for credit sparingly

Avoid applying for a lot of credit in a relatively short period. Typically, a credit application results in a credit bureau checking your credit, and each hard inquiry can ding your credit score. Lots of credit applications in a short time can do more damage. Fortunately, the effect fades after about a year. Spacing applications out by about six months is the safest idea.

Keep credit cards open

We don’t mean you can never close a card, but think about it carefully if the card you're considering closing is one of your oldest cards or if it’s got a high credit limit. The age of credit and the percentage of your overall credit limit you use have a powerful effect on your credit score.

Check your credit reports

You want your credits report to be boring. Interesting things, like an address where you’ve never lived or an account that doesn’t belong to you, could signal identity theft. You’ll want to get to the bottom of that right away. Being mistaken for a same-name or same-address family member who has a sordid credit past could impact your score. You can access your credit reports from all three credit bureaus for free at annualcreditreport.com. Get errors corrected, and your score should reflect it.

Pay strategically

Once you have the big things covered, consider learning the strategies to add every point you can. Things like zapping small, lingering balances or making small, frequent payments can help.

Compare the same score

Credit scores are snapshots of a moment in time, and they're calculated on demand. That means they fluctuate, since they're based on the information in your credit reports at that given moment. The two major scoring companies, FICO and VantageScore, have several different scoring models as well, so your score can vary among them.

Do what you’d do if you were trying to figure out your “true” weight: Use the same scale every time you weigh yourself. Even then, it’s not going to be the same every time you step on. You should be within a few pounds, though, and trends will be evident no matter which scale you're using, right? Credit scores are similar. That means pick one source of a free credit score and use it to track your progress over time.

Smaller-impact things to know

Credit scores reward you for having a mix of credit cards (revolving accounts, in credit-speak) and loans such as mortgages and auto loans (installment accounts).

Be aware that if you co-sign for someone else, it’s not a character reference — it’s an agreement to pay if they do not. You are responsible for the full loan amount. Having that loan obligation could reduce your own borrowing power if you need to borrow money. And if the primary borrower pays late, your credit score is likely to suffer.

What happens to a 720 score with a late payment?

If it’s just a day or two late, pay up as quickly as you can, but don’t worry about score damage. Nothing gets reported to the credit bureaus unless you are at least 30 days late. The creditor could charge you a late fee, though. You could call the creditor and ask it to rescind the late fee. It’s best to do this when it has gotten your payment already and when you’ve rarely been late before.

If you do have a payment 30 or more days past due and it’s reported to the credit bureaus, it can do serious harm — and late payments stay on your credit reports longer than most other credit missteps. The higher your score is, the bigger the fall is likely to be. That is to say, it could fall about 100 points. But that’s not the worst thing that can happen. As a payment gets later — at 60 days past due, 90 days and so on — things can get uglier. The late payment can turn into a collection action, judgment, foreclosure or bankruptcy. Those can make the initial 100-point drop seem like it wasn’t all that bad.