We believe everyone should be able to make financial decisions with confidence. And while our site doesn’t feature every company or financial product available on the market, we’re proud that the guidance we offer, the information we provide and the tools we create are objective, independent, straightforward — and free.

So how do we make money? Our partners compensate us. This may influence which products we review and write about (and where those products appear on the site), but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services. Here is a list of our partners.

How to Get the Best Mortgage Rate

You can get the best mortgage rate by knowing what lenders are looking for, shopping around and paying aggressively upfront.

Taylor Getler Writer | Home equity, first-time home buying, home warranties

Taylor Getler is a home and mortgages writer for NerdWallet. Her work has been featured in outlets such as MarketWatch, Yahoo Finance, MSN and Nasdaq. Taylor is enthusiastic about financial literacy and helping consumers make smart, informed choices with their money.

Michelle Blackford spent 30 years working in the mortgage and banking industries, starting her career as a part-time bank teller and working her way up to becoming a mortgage loan processor and underwriter. She has worked with conventional and government-backed mortgages. Michelle currently works in quality assurance for Innovation Refunds, a company that provides tax assistance to small businesses.

At NerdWallet, our content goes through a rigorous editorial review process. We have such confidence in our accurate and useful content that we let outside experts inspect our work.

Alice Holbrook Assigning Editor | Homebuying, savings and banking products

Alice Holbrook edits homebuying content at NerdWallet. She has covered personal finance topics for almost a decade and previously worked on NerdWallet's banking and insurance teams, as well as doing a stint on the copy desk. She is based in Ann Arbor, Michigan.

Some or all of the mortgage lenders featured on our site are advertising partners of NerdWallet, but this does not influence our evaluations, lender star ratings or the order in which lenders are listed on the page. Our opinions are our own. Here is a list of our partners.

You’re following Taylor Getler Visit your My NerdWallet Settings page to see all the writers you're following.

After the sticker price of the home, your interest rate is the biggest influence on your monthly mortgage payments. With a higher rate, interest takes up a larger share of your monthly housing budget, and it might also affect the price range that you can comfortably shop.

Though it can feel like you’re at the mercy of lenders and the market, there are steps you can take to improve the rates you’re offered, potentially saving thousands of dollars and growing your homebuying budget.

1. Strengthen your financial profile

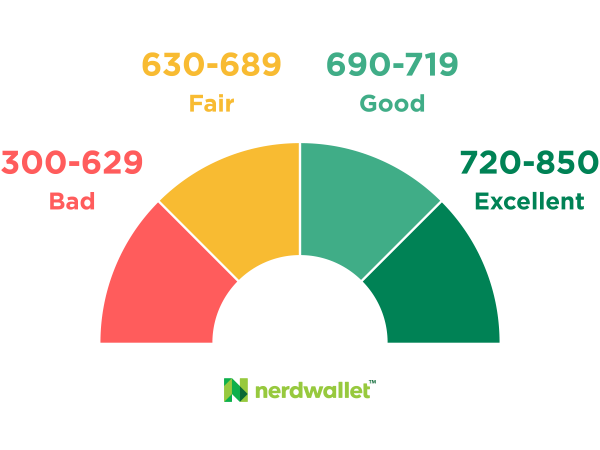

The best mortgage rates are typically reserved for borrowers with the best credit scores, so you’ll want to know where your credit score will stand with lenders. Scores in the highest range (720-850) are considered “excellent,” while scores in the 690-719 range are “good,” scores in the 630-689 range are “fair,” and scores in the 300-629 range are “bad.”

You can grow your credit score by paying your bills on time, as well as by paying down debt to reduce the amount of credit you’re using and maintaining low credit balances. Keep your cards open to prevent your utilization from going up. You’ll also want to pay off any debts that have gone to collections.

NerdWallet recommends that you request free credit reports from the three major credit reporting bureaus (Experian, Equifax and TransUnion) and dispute any errors that might be suppressing your credit score. You can access these reports at AnnualCreditReport.com.

In addition to your credit score, lenders will also consider your debt-to-income ratio (DTI). This is the percentage of your gross monthly income that goes toward paying your debts. This number does not include nondebt expenses, such as groceries or utilities.

Lenders typically want this number to be no higher than 36%; the lower, the better. Paying down credit card debt will also improve your debt-to-income ratio. You can find this number using NerdWallet’s DTI calculator.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

0%On VA loans, NBKC offers down payments as low as 0%.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

3.5%First-time home buyers may qualify for 3% down mortgages at Rocket.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%Better offers 3% down payments on conventional loans.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%Guaranteed Rate offers conventional loans with as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

0%On VA loans, NBKC offers down payments as low as 0%.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

3.5%First-time home buyers may qualify for 3% down mortgages at Rocket.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

4.0

NerdWallet rating

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%Better offers 3% down payments on conventional loans.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

0%Veterans United offers VA loans for as little as 0% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%Rocket Mortgage offers conventional mortgages with as little as 1% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

3%New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%Guaranteed Rate offers conventional loans with as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

N/ANew American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

5.0

NerdWallet rating

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

N/ANew American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

0%On VA loans, NBKC offers down payments as low as 0%.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

3.5%First-time home buyers may qualify for 3% down mortgages at Rocket.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%Better offers 3% down payments on conventional loans.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

0%On VA loans, NBKC offers down payments as low as 0%.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

3.5%First-time home buyers may qualify for 3% down mortgages at Rocket.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

4.0

NerdWallet rating

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%Rocket Mortgage offers conventional mortgages with as little as 1% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

620620

Min. down payment

3%NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

3%New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

N/ANew American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score

580580

Min. down payment

N/ANew American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Being able to put a larger amount down on a house will lower your loan-to-value ratio (LTV) and generally also your mortgage rate. For example, if you make a 20% down payment, your LTV is 80%.

Conventional mortgage borrowers who put down less than 20% are also required to pay private mortgage insurance (PMI), an additional monthly expense. When looking at lender rates online, be aware that the advertised rate often assumes that the borrower is putting down 20% or more.

Discount points are fees borrowers pay to reduce the interest rate on their mortgages. One point costs 1% of the loan amount, which typically reduces the mortgage rate by 0.25%, although the reduction can vary.

When you pay discount points, you typically shell out thousands of dollars upfront to save a few dollars every month. The more points you buy, the larger your monthly savings will be. You’ll likely have to pay at least three or four discount points to save more than $100 each month. It takes several years for your total savings to exceed the initial amount paid. This break-even period varies depending on the loan amount, the cost of the points and the interest rate.

You can calculate the potential savings of paying points and find the break-even period using NerdWallet’s mortgage points calculator. If the break-even period exceeds the amount of time you plan to be in the home, then buying points probably isn’t worth it.

For example, if you pay $3,000 for one discount point on a $300,000 mortgage, you could bring your mortgage rate down from 6.75% to 6.5%. This would result in monthly savings of $50, with a break-even period of five years to recoup the cost of the point.

4. Take advantage of first-time home buyer programs

Before you settle on a mortgage, find out whether you’re eligible for any special programs that make homebuying less costly. Many states offer help to first-time home buyers as well as repeat buyers.

Each state offers its own mix of programs, often including down payment assistance, combined with favorable interest rates and tax breaks. Some programs are targeted geographically, and others offer help to home buyers in certain professions, such as teachers, first responders and veterans.

You probably wouldn’t commit to buying the first home you tour, right? You’d shop around until you found one that fits your needs and is affordable. The same philosophy can be applied to finding a lender. If you have an existing relationship with a lender, they can be a great place to start, especially if they offer discounts to current customers. However, applying for preapproval with a few lenders gives you an opportunity to compare offers and see who is offering the lowest rate.

Though 30-year fixed-rate mortgages are popular among homebuyers, other types of mortgages can come with lower rates.

For example, adjustable-rate mortgages (ARMs) can have introductory rates below market. These mortgages have a fixed rate for a certain number of years before changing on a regular cadence, usually every six months. For example, a 5/6 ARM will have a fixed interest rate for five years before adjusting every six months. This can be risky because you’ll have to pay more if rates rise. However, these mortgages can be a strategic choice if you plan to sell before the fixed period ends.

You can also choose a shorter loan term; 15-year mortgages often have lower interest rates than 30-year mortgages. Because you’ll have less time to pay it off, your monthly payments will be higher. However, you’ll save on the overall loan because you’ll be making fewer interest payments.

Loans backed by the Federal Housing Administration (FHA) can also have lower rates than conventional mortgages as well as more flexible qualification requirements.

However, you'll have to pay a monthly insurance premium. If you’re able to make a down payment of 10% or more, you can cancel this insurance payment after 11 years. Otherwise, you’ll be required to keep paying it for the life of the loan or until you refinance.

You could also consider a shared appreciation mortgage (SAM), which involves giving a lender a percentage of the future appreciation of the home in exchange for a below-market interest rate or another kind of perk. In addition to making monthly loan payments, you’d pay any remaining principal balance at the end of the term plus a percentage of its appreciated value. Beware that if your home grows in value, you’ll be obligated to pay more to the lender. Under the terms of a traditional mortgage, you would retain any accumulated equity.

The average rate for a 30-year conventional mortgage has been above 6.5% since early 2023, meaning that a rate offer anywhere near 4% would be significantly below market. However, if you’re willing to lower your budget to make more aggressive monthly payments, you could opt for a shorter loan term, which comes with a lower rate.

For instance, say you purchased a $350,000 house with $35,000 down at a rate of 6.5% for 30 years, and your monthly payment is $2,592. You could purchase a $280,000 home and take out a 15-year mortgage at a rate of 5.5% for a monthly payment of $2,585. For nearly the same monthly payment, the combined lower rate and smaller total mortgage would enable you to pay off your home in half the time.

Will mortgage rates go down in 2024? Will they go down in 2025?

Maybe. This depends on market conditions and other factors that are nearly impossible to predict more than a few weeks out. Rather than trying to time the market, you’re better off focusing on elements within your control that affect your rate offers — namely, lowering your existing debts and bolstering your credit score and down payment savings.

How do I ask my lender for a better rate?

Applying to multiple lenders will allow you to find the lowest rate offer, and it can give you negotiating power if you have a preferred lender. Additionally, you can ask your lender whether you qualify for any rate discounts.

Is it possible to get a 4% mortgage rate?

The average rate for a 30-year conventional mortgage has been above 6.5% since early 2023, meaning that a rate offer anywhere near 4% would be significantly below market. However, if you’re willing to lower your budget to make more aggressive monthly payments, you could opt for a shorter loan term, which comes with a lower rate.

For instance, say you purchased a $350,000 house with $35,000 down at a rate of 6.5% for 30 years, and your monthly payment is $2,592. You could purchase a $280,000 home and take out a 15-year mortgage at a rate of 5.5% for a monthly payment of $2,585. For nearly the same monthly payment, the combined lower rate and smaller total mortgage would enable you to pay off your home in half the time.

Will mortgage rates go down in 2024? Will they go down in 2025?

Maybe. This depends on market conditions and other factors that are nearly impossible to predict more than a few weeks out. Rather than trying to time the market, you’re better off focusing on elements within your control that affect your rate offers — namely, lowering your existing debts and bolstering your credit score and down payment savings.

How do I ask my lender for a better rate?

Applying to multiple lenders will allow you to find the lowest rate offer, and it can give you negotiating power if you have a preferred lender. Additionally, you can ask your lender whether you qualify for any rate discounts.

Understanding how much you can afford is a great first step to buying a home. NerdWallet helps you easily determine your home buying budget with our home affordability calculator.