New deductions for tips and overtime made headlines last year after the “One Big, Beautiful Bill Act” (OBBBA) was signed into law. But don’t overlook another tax break the bill ushered in: the senior tax deduction.

What is the new ‘senior bonus deduction’?

The tax code already gives seniors who are 65 and older a break in the form of a larger standard deduction, allowing eligible people to deduct up to an extra $2,000 on top of their regular amount.

New this filing season is the "senior bonus deduction." This is an separate benefit for qualified seniors that will be available through 2028 unless extended by Congress. It’s worth up to $6,000 per qualifying individual, meaning joint filers who are both 65 or older can get up to $12,000.

If you qualify, you can claim both the extra standard deduction and the new senior bonus deduction.

Who qualifies for the deduction?

Being 65 or older by the end of 2025 is the first box you have to check to qualify, but there are a few other rules to know about.

Income limits: Individual filers must have a modified adjusted gross income (MAGI) of $75,000 or less to claim the full credit. For joint filers, the MAGI limit is $150,000. The deduction amount is reduced by 6 cents for every dollar of income that exceeds these limits until it phases out completely. This means you won’t get any credit if you made $175,000 or more last year as an individual or $250,000 or more as a joint filer.

Single filer income | Joint filer income | |

|---|---|---|

Full credit | $75,000 or less. | $150,000 or less. |

Partial credit | Between $75,000 and $175,000. | Between $150,000 and $250,000. |

No credit | $175,000 or more. | $250,000 or more. |

Social Security number: Taxpayers must have a valid Social Security number to claim the senior tax deduction. This requirement has become more common to claim popular tax credits and deductions since the OBBBA was passed.

File jointly: Filers who are married must file a joint return with their spouse to claim the deduction. This is true regardless of if your spouse qualifies for the deduction.

This tool was created by our editorial team with the assistance of AI. It has been reviewed by our team for accuracy and quality.

» How does this deduction affect your whole tax picture? Use our free tax calculator to find out

How to claim the deduction

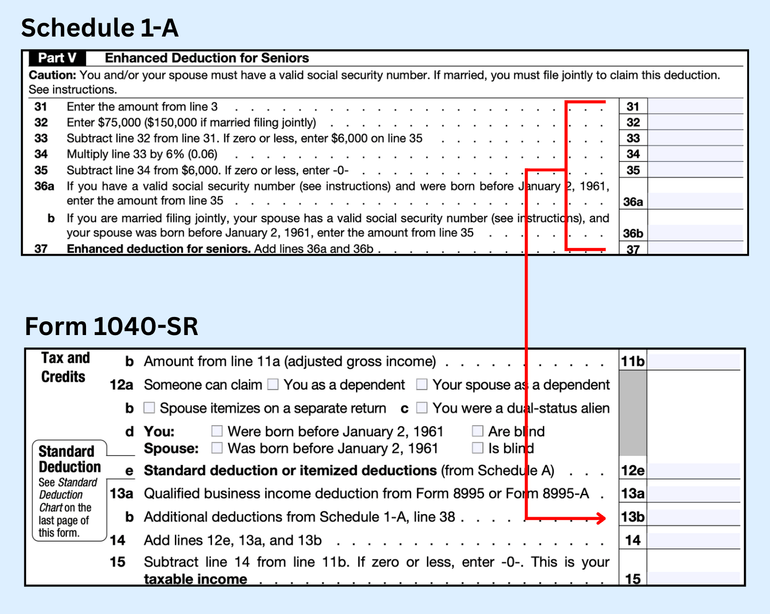

Unlike some other tax breaks, you don’t have to itemize deductions on your tax return to claim the senior bonus deduction. You’ll need to fill out the “Enhanced Deduction for Seniors” section of Schedule 1-A and include your deduction amount on line 13b of Form 1040 or 1040-SR.

Unless you’re filing your return with paper forms and mailing it in — which the IRS doesn’t recommend — you won’t need to get too cozy with these forms. Tax software will do this work for you.

You may, however, want to explore whether you qualify for the IRS’ volunteer-run Tax Counseling for the Elderly (TCE) program, which offers free tax preparation services for qualified filers who are 60 and older. The IRS says TCE volunteers specialize in “questions about pensions and retirement-related issues unique to seniors.” You can find the TCE location closest to you by using the IRS’ locator tool.

AD

Owe $10,000+ or More? This Tax Season Could Be Your Chance to QualifyEach year the IRS writes off millions in tax debt, yet few have applied.

on Anthem Tax Services' website

AD

Owing the IRS Over $10K Is More Common Than You ThinkDiscover tax resolution options customized to your case, backed by a 100% Resolution Money Back Guarantee.

on TaxRise's website

AD

Owe $10,000+ or More? This Tax Season Could Be Your Chance to QualifyEach year the IRS writes off millions in tax debt, yet few have applied.

on Anthem Tax Services' website

AD

Owe $10,000+ in IRS Back Taxes? Get Trusted Tax Help TodayBBB Accredited, $500M+ tax debt resolved, free consultation.

on Alleviate Tax's website

Explore more on