First National Financial Mortgage Review 2026

First National Financial: Our quick take

First National Financial is unique among Canadian lenders in that it provides mortgages for traditional borrowers as well as those who can't qualify for conventional mortgages.

Who is a First National mortgage best for?

First National Financial may be a good choice if you're looking for a competitive non-bank lender or are having difficulty qualifying for a traditional mortgage.

First National loans are only available through brokers, so a willingness to work a mortgage broker is a must.

Who's eligible for a First National mortgage?

To qualify for a prime mortgage with First National, as with any lender or brokerage, you’ll need to meet certain eligibility requirements.

These include:

Minimum credit score: To get First National's best rates, you'll generally need a credit score of at least 680, as you would with Big 6 lenders. But First National also lists rates for borrowers with credit scores below 680. There is no minimum score listed for its Excalibur mortgage product.

Down payment amount: At least 5% for a home under $500,000. For homes between $500,000 and $1,499,999, you need 5% of the first $500,000 and 10% of the amount above $500,000. For a home that costs $1.5 million or more, you’ll need 20% of the purchase price.

Debt service ratios: First National may offer borrowers more flexible standards compared to traditional lenders.

First National's Excalibur mortgage, which is designed for those with low credit, is available in Ontario, Atlantic Canada, British Columbia and the Prairies.

What types of mortgages does First National offer?

First National advertises the following mortgage types publicly:

Fixed-rate mortgages.

Variable-rate mortgages.

Closed and open mortgages.

Mortgage renewals.

Mortgage refinances

Mortgages for self-employed individuals.

Bad credit mortgages

How do First National's mortgage rates compare?

You can see how First National's mortgage offers stack up against bank and non-bank lenders on the following pages.

Review of First National mortgage features

NerdWallet Canada's editorial team sifted through dozens of lender websites looking for features borrowers are interested in. Then, we summarized how each lender compares to its competitors using the labels "limited," "standard" or "excellent."

To see the details that led to each summary, expand the box below each entry.

Special offers available

LIMITED

First National doesn't list any special offers on its website. It also doesn't list APRs along with the rates it posts, which makes them harder to compare to rates you find elsewhere.

The mortgage broker you work with will be able to get that information for you.

First National helpfully shares different mortgage rates for different down payment amounts. It also has various mortgage rates for specific credit score ranges below 680.

Why this might matter for you: Special rates can be a window into the types of rates you'll actually get from a lender. It's frustrating when one lender clearly displays them online and another doesn't.

Why this might not matter: If you work with a mortgage broker, they're the ones who will gather rate information. Also, because every mortgage offer is unique to the applicant, a special rate you see may not reflect the rate a lender will offer you.

Term length options

STANDARD

First National advertises nine term lengths online.

Why this might matter for you: Some borrowers need financing for an unusual amount of time (six months, six years or 25 years, for example).

Why this might not matter: If you intend to get a standard three- or five-year term, having access to less common terms doesn't matter as much.

Expand for details

First National offers the following mortgage terms:

6 months (open)

1-year fixed

2-year fixed

3-year fixed

4-year fixed

5-year fixed

5-year variable

7-year fixed

10-year fixed

Prepayment limit

STANDARD

First National's prepayment privileges are standard. You can pay up to 15% of your original mortgage amount each year without penalty.

That’s better than the 10% limit found at the least flexible lenders, but not as generous as those that allow you to prepay 20 or 25%.

You can also increase your mortgage payment as a form of prepaying. First National allows you to increase your monthly payment on fixed-rate mortgages by up to 15% without triggering any prepayment charges. That's

Why this might matter for you: Paying off a mortgage early is a goal many homeowners have. The bigger your lender's lump-sum prepayment limit, the more flexibility you'll have.

Why this might not matter: If you don't expect to have funds available for prepayments, this limit is irrelevant.

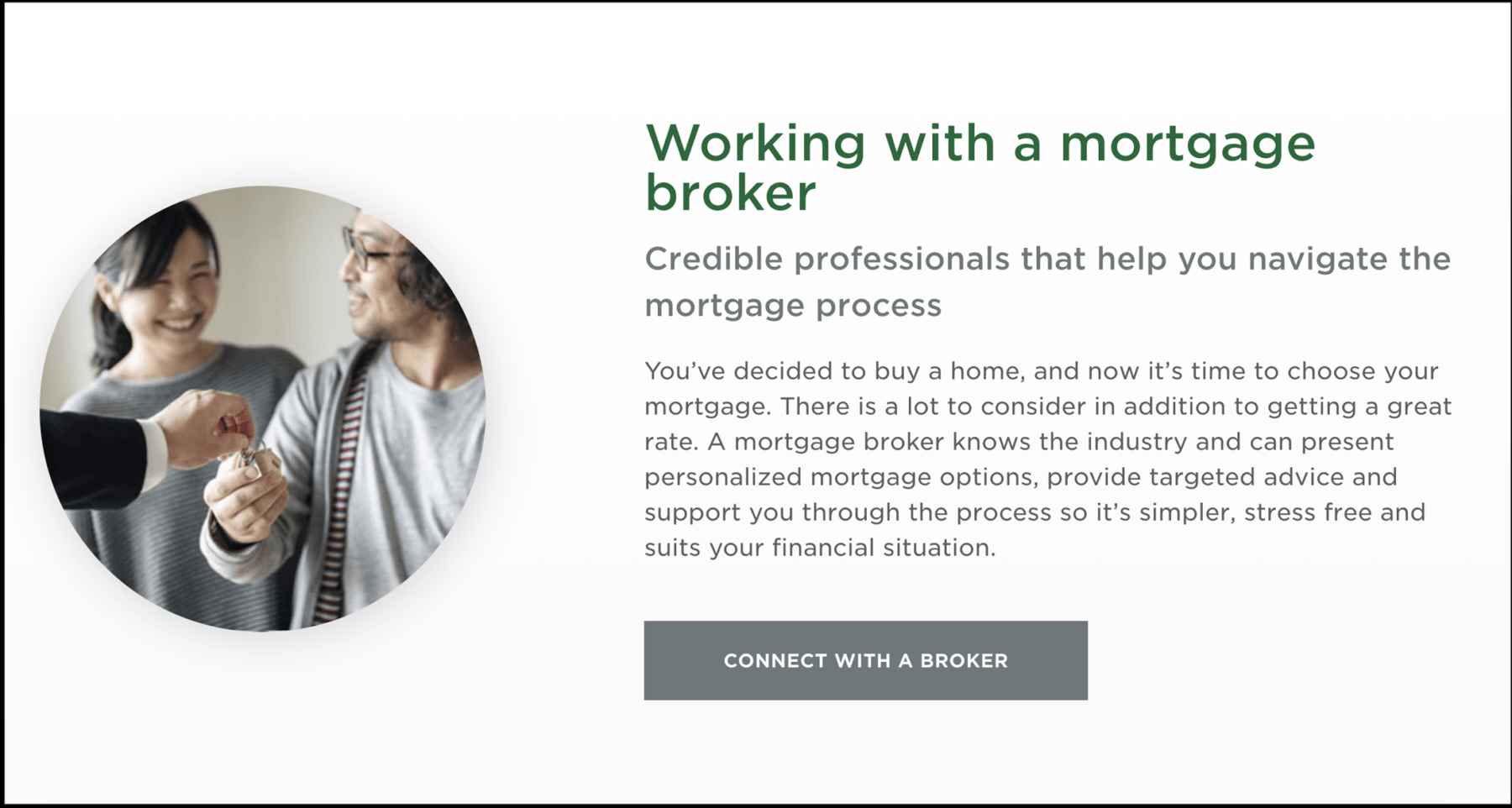

What it’s like to apply at First National

First National deals exclusively with mortgage brokers, so the only way you can apply for a mortgage with the company is by first contacting a broker. First National can help you do that.

Learn more about finding a mortgage broker

After navigating to the First National homepage, hover over “Residential Mortgages” and then click on “Working with a mortgage broker.”

Click on “Connect with a Broker,” enter your contact information and you should hear from a broker within two business days. We were contacted within hours of submitting our information.

You don’t necessarily have to use the form on the First National site. You can reach out to mortgage brokers in your area and ask them if they work with the company.

About NerdWallet mortgage reviews

When the NerdWallet Canada editorial team reviews a mortgage lender, we look for the options it offers customers, transparency in advertising, ease of application and flexibility it offers mortgage-holders.

Of course, a mortgage is a highly personalized product. The offer you receive depends on the details of your financial situation. A lender may have a less-than-transparent website but offer you a great rate.

Use this review to familiarize yourself with this mortgage lender. To get the best mortgage rate, work with a mortgage broker or negotiate directly with multiple lenders.

DIVE EVEN DEEPER

Clay Jarvis

Clay Jarvis Clay Jarvis

Clay Jarvis Kurt Woock

Kurt Woock

Beth Buczynski

Beth Buczynski