TransUnion Credit Score in Canada: Ranges and How to Access

Evaluating your three-digit credit score is one way that lenders, like banks and credit card issuers, decide whether or not to approve you for a loan or line of credit.

There are multiple credit reporting agencies, sometimes called credit bureaus, in Canada. TransUnion is one such agency, and is a common source of credit history and score information for both consumers and creditors.

What is a TransUnion Credit Score?

A TransUnion credit score is a three-digit number, from 300 to 900, that represents your general creditworthiness.

TransUnion is one of the major credit bureaus in Canada. The company was established in 1989 and now has offices across the country.

Based on the data provided by financial institutions, TransUnion uses scoring models provided by companies like the Fair Isaac Corporation or VantageScore, along with its own algorithms, to generate credit scores.

Your TransUnion credit score may fluctuate over time, depending on how you access and use credit. Your credit score may change immediately, such as after applying for new credit. Or, your credit score may increase or decrease gradually based on day-to-day credit use.

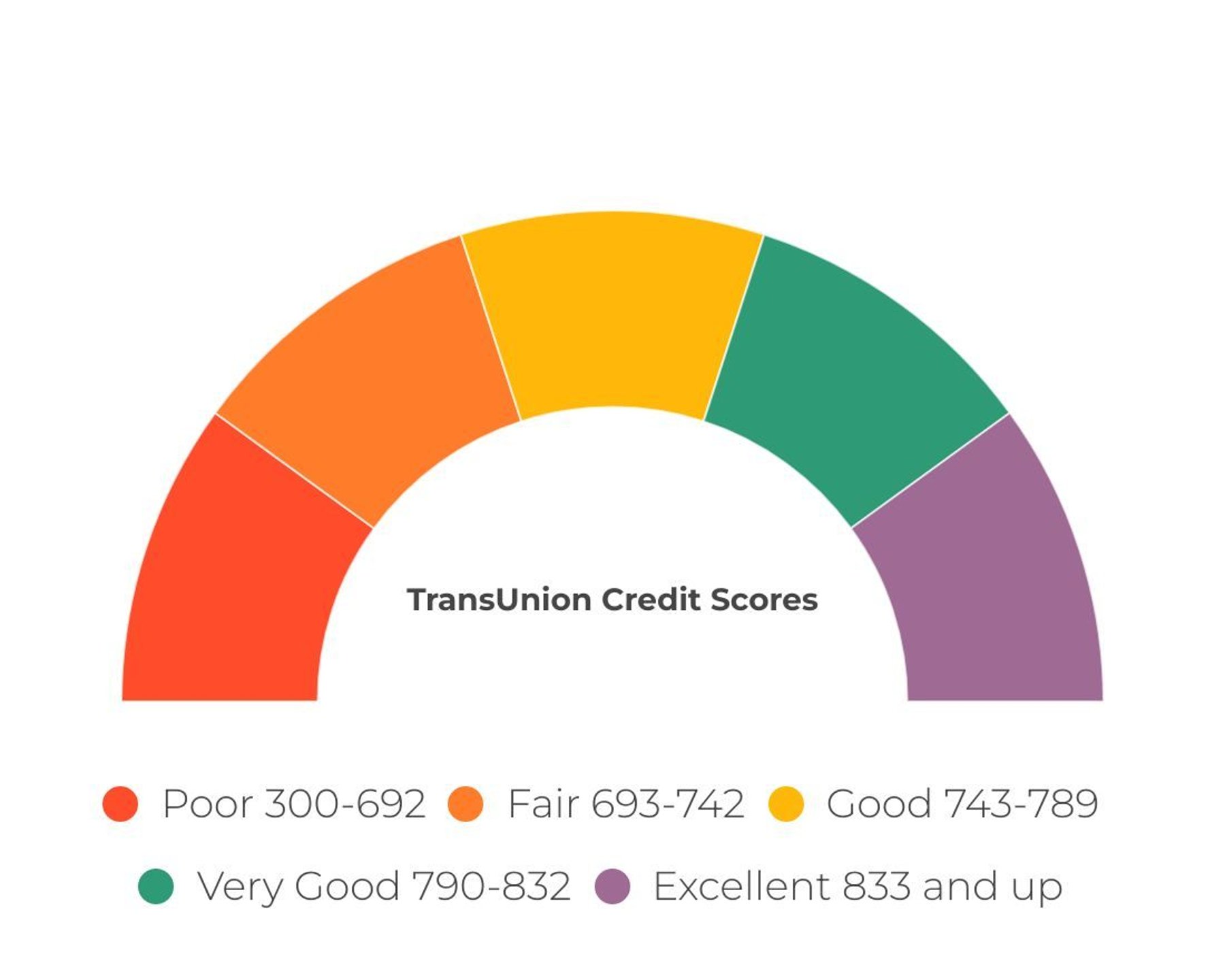

TransUnion credit score ranges

Source: RBC

Source: RBCTransUnion credit score ranges and what they mean

Poor (300-692): You’ve likely had credit-damaging incidents in the past. It will be tough to get approved for credit. If a lender is willing to extend credit to you, they’ll likely charge a higher interest rate.

Fair (693-742): You’re likely establishing or rebuilding your credit. You might be approved for entry-level credit cards with a low limit. If you’re applying for other types of credit, the interest rates may still be a touch higher.

Good (743-789): You’re keeping a good handle on your existing debts. You’re likely to qualify for many loans and lines of credit at competitive interest rates.

Very good (790-832): You’ve had very few credit-impacting incidents on your report. You’ll likely get access to most financial products with favourable rates.

Excellent (833 and up): There are no credit-damaging incidents on your report, and you don’t carry much debt. You’ll likely be eligible for top-tier credit products, like premium credit cards, and could potentially negotiate competitive rates on loans and lines of credit.

While your TransUnion score is an important factor when determining your creditworthiness, it’s not the only thing lenders look at when determining if they’ll approve you for a loan or more credit. Some other factors include your income, monthly expenses and how much debt you currently have. And creditors will likely look at scores from more than one bureau at a time.

How to get your TransUnion credit score in Canada

There are multiple ways to access your TransUnion score in Canada. That said, each method varies in convenience, level of information provided and cost. Knowing your options is essential.

TransUnion Canada

Credit scores can be obtained directly from TransUnion Canada, however it will require you to sign up for a paid, monthly subscription. The cost of a subscription is $24.95 a month, plus applicable tax, as of this writing.

While TransUnion is required by law to provide all Canadians with free access to their credit report, only residents of Quebec are eligible to receive their credit score for free, according to the TransUnion website.

Third-Party Services

TransUnion credit scores can also be obtained via certain banks and financial companies, if you’re a customer or member. These include:

RBC: Existing customers can get free access to a TransUnion CreditView Dashboard, by logging into their RBC Online Banking account and selecting the “View Your Credit Score” link.

Credit Karma: Account holders can access their TransUnion credit score and report for free, as often as they like.

ClearScore: ClearScore is another company that has partnered with TransUnion to provide credit scores and reports to its members. According to the ClearScore website, there is no cost to sign up.

Credit Scores from Other Providers

TransUnion is not the only credit reporting agency in Canada. This is relevant because not all financial institutions provide the same information to the credit bureaus. That means your credit score will likely differ from one agency to the next. The other reporting agencies are:

Equifax: The other major reporting agency in Canada is Equifax. Their main Canadian office is located in Toronto, and beyond credit scores and reports, they also provide general information to enhance Canadians’ financial literacy.

FICO: The Fair Isaac Corporation, or FICO, is more widely known in the U.S., but is used in Canada as well. Both TransUnion and Equifax provide credit report data to FICO. That data is then used with FICO’s own scoring models to generate credit scores, sometimes known as a FICO or beacon score.

Improving Your TransUnion Score

If you’d like your TransUnion score to be higher, here are a few credit-building behaviors you can keep in mind:

Keep your credit utilization ratio low: The amount of credit you use relative to how much credit you can access is known as your credit utilization ratio. For example, if you regularly charge $2,000 to your credit card and you have access to $10,000 total credit, your utilization ratio is 20%. Generally, you want to keep your utilization ratio below 30%.

Pay your bills on time: By paying your credit card bills and loans on time, it shows credit bureaus that you’re responsible with your money. Try your best to pay off the entire amount each month, as you’ll lower your utilization ratio and avoid interest charges.

Limit your credit applications: Whenever you formally apply for credit, a hard inquiry is performed on your credit profile. This typically results in a drop in your credit score by a few points. While your credit score may naturally improve over time, you still want to avoid any unnecessary inquiries on your credit score.

Start using credit: If you’re looking to establish or rebuild your credit score, you’ll need to start somewhere. See if your financial institution will approve you for an entry-level credit card. If you find you’re still being declined, you could apply for a guaranteed secured credit card.

DIVE EVEN DEEPER

Janine DeVault

Janine DeVault

Barry Choi

Barry Choi

Siddhi Bagwe

Siddhi Bagwe