The 3 Credit Bureaus, and Why They Matter to You

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

There are three major credit bureaus, and your credit score will vary depending on which one provided the data to create that score.

Key takeaways:

A credit bureau — sometimes called a credit reporting agency — is a business that collects data about you and how you've used credit. The three major credit bureaus are Equifax, Experian and TransUnion.

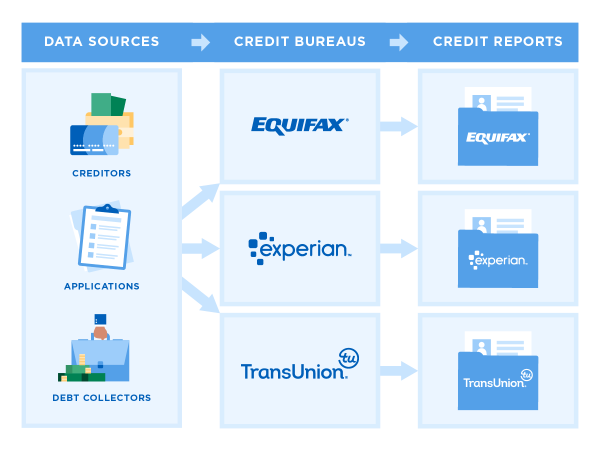

Credit bureaus use that data about you, provided by creditors, to create your credit reports — and your credit scores are based on those reports.

These credit bureaus also sell that data to lenders and others who want to check your credit before doing business with you.

You can dispute errors on your credit report with each bureau and also put a security freeze on your credit.

What are the three credit bureaus?

The three major credit bureaus are Equifax, Experian and TransUnion. Credit bureaus gather and maintain data on consumers' credit use, which means that if you have a credit card or a loan, you probably have a credit file with one, two or all three major credit bureaus.

Sometimes called credit reporting agencies, these credit bureaus can collect and sell information on your consumer credit behavior without your consent. However, businesses that check your credit, such as credit card issuers and lenders, must have a legitimate reason to look at your credit file, such as screening credit applications. In most cases they must have your permission.

The information credit bureaus collect is typically used:

To calculate credit scores.

To make lending decisions, such as whether to offer you a credit card or loan and at what interest rate.

In some pre-employment background checks.

To evaluate lease applications.

In setting some insurance rates.

To decide whether you must pay a utility deposit.

You have a right to see your credit reports and to dispute information that is inaccurate or should no longer be reported because of its age.

What data do the credit bureaus maintain?

Your credit reports will include identifying information, such as your name, birthdate, Social Security number and addresses (past and present).

They also can contain:

A list of current and past credit accounts.

Payment history, such as whether you paid on time.

Negative information, such as missed payments, collections, bankruptcies, repossessions and foreclosures. Each type of negative mark must come off your report after a set time, usually seven years.

A record of who has accessed your credit report, for instance when you apply for credit or when a marketer wants to preapprove you for an offer.

If data privacy is a concern, you should know that credit bureaus are highly regulated by the Fair Credit Reporting Act, or FCRA, which puts limitations on how they collect and share your personal data.

Where do the credit reporting bureaus get their data?

Creditors report how you handle accounts, including payment history. They're not required to report to the credit bureaus, but most do because data on how borrowers have handled credit cards and loans in the past helps them make lending decisions.

Creditors may report to one, two or all three bureaus — so your credit report at each bureau can vary a bit from the others.

Some types of accounts don't routinely show up on your report, such as utilities and rent. But those accounts can still end up on your report if there's a payment problem that leads to a debt collection.

Data also comes from public records, such as:

Repossessions.

Bankruptcy filings.

Foreclosures.

Can other types of data help my credit reports?

If you are new to credit, you might benefit from getting other types of account information added to your reports. Options include:

If you're a renter, you can look into rent reporting.

You can use one of the newer products that gather some data from bank accounts you link, such as Experian Boost and UltraFICO.

Why doesn’t my report show a credit score?

While the law requires the credit bureaus to let you see the information in your credit reports, there is no such requirement for credit scores.

There are many types of credit scores, but the two main ones are FICO and its competitor VantageScore, which was developed jointly by the three main credit bureaus.

Scores are created by running the information in your credit reports through a mathematical formula designed to predict how likely you are to repay debt. Because the bureaus may have slightly different datasets, your scores may vary depending on which scoring model was used and whose data was used.

You can get a free credit score from many personal finance websites, such as NerdWallet, banks and credit card issuers.

Are credit scores from all major bureaus the same?

You may notice some variation in your credit score depending on which credit bureau’s data was used.

These differences exist because creditors report your payment history and other financial behaviors to the credit bureaus, but they don’t have to report to every bureau. So, one credit bureau might have more information than the other two, thus making your credit score different.

The main thing to take away is this: Your credit score will likely vary depending on whether it is based on data from Experian, Equifax or TransUnion. But that’s not a cause for alarm. The only cause for worry is if one bureau reports a score that is drastically different from the other two. Then, it’s time to check your credit reports for score-lowering errors and dispute them.

How can I check my credit reports?

You can use AnnualCreditReport.com to get the free reports you're entitled to from the three major credit bureaus. Because credit bureaus operate independently, each may receive information from a different set of sources. It’s important to check all three reports.

It’s smart to read your reports to make sure your identifying information and account information are correct, because mistakes can lower your credit scores.

You can also check on some personal finance websites that offer a free credit report, like NerdWallet. NerdWallet’s credit report displays TransUnion data.

You can request your credit report in Spanish directly from each of the three major credit bureaus: · TransUnion: Call 800-916-8800. · Equifax: Visit the link or call 888-378-4329. · Experian: Click on the link or call 888-397-3742.

🤓 Consejo Nerdy Usted puede solicitar una copia de su informe crediticio (gratis y en español) de cada una de las tres principales agencias de crédito: · TransUnion: Llame al 800-916-8800. · Equifax: Visite el enlace o llame al 888-378-4329. · Experian: Haga clic en el enlace o llame al 888-397-3742.

What if I see a mistake on my report?

If you see an error, you can dispute it. That means you file a formal complaint online, by phone or by mail, and the bureau must respond. Each credit bureau has a slightly different procedure for disputing.

It’s important to fix a mistake with all three major bureaus, because credit reporting agencies do not share information.

What else do credit bureaus do?

You can protect your credit by asking each bureau to freeze your credit. It's free to freeze your credit (and to unfreeze it when you want to apply for something), and it won't hurt your score.

NerdWallet recommends freezing to protect yourself from scammers opening accounts in your name and ruining your credit.