Travel Insurance and Pregnancy: What to Know

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

There’s a lot to think about when you’re pregnant — especially if you plan to travel. You’ll want to make sure your health care and your trip costs are covered if something goes wrong.

And while travel insurance for pregnancy may sound like a must-have, remember that not all plans will cover your specific needs. At the moment, there isn't a specific insurance option for those who are pregnant. Rather, pregnant people will need to consider travel insurance that includes coverage for trip cancellation and interruption, as well as emergency medical and evacuation costs.

Your decision to buy travel insurance while pregnant will depend on how much of your trip is nonrefundable, where you’re going and what coverages you already have. These coverages may include trip interruption insurance from your credit card issuer or emergency medical coverage from your current health insurer.

Here’s what you need to know to choose the best travel insurance for pregnancy.

Trip cancellation or interruption due to pregnancy

Most travel insurance policies will reimburse you for all or a portion of your nonrefundable travel costs if you have to cancel your trip for a covered reason. But for pregnant people, covered reasons are a little more complicated.

For most policies, normal pregnancy is not a valid reason to cancel your trip if you already knew you were pregnant when you purchased the insurance. But pregnancy may be a valid reason to cancel if you learn you're pregnant after you’ve booked your trip and paid for an insurance policy.

For example, if you prepay for a trip a year in advance, purchase Allianz travel insurance, and a few months later find out you’re pregnant and need to cancel your trip, the company will likely reimburse you for all or a portion of your lost travel costs. But you’ll have to prove that you learned about your pregnancy after you purchased the policy.

On the other hand, if you knew you were pregnant when you purchased the policy, you will likely not get reimbursed if you canceled your flight due to morning sickness, for example.

» Learn more: Can you fly while pregnant? It depends.

Trip cancellation or interruption due to complications of pregnancy

If you have complications during your pregnancy, travel insurance may cover your trip costs regardless of when you learned you were pregnant.

Keep in mind that only specific complications — like gestational diabetes, preeclampsia, hyperemesis gravidarum or miscarriage — are eligible, and a doctor must advise you not to travel due to your diagnosed condition.

Medical coverage for pregnant travelers

If you’re traveling domestically, your regular health insurance may be all the coverage you need. Check with your provider. If you’re going abroad, there’s a good chance your health insurance will not reimburse you for medical expenses while traveling. So for pregnant people traveling internationally, travel medical insurance is probably a good idea.

Secondary travel health insurance can be surprisingly affordable. Secondary plans kick in after you’ve used any applicable primary insurance coverage from your current health insurer.

Searching InsureMyTrip.com, we found secondary international medical insurance plans starting at $14 for a 30-year-old California resident traveling to France for 12 days in September. For this price, you receive coverage up to $50,000.

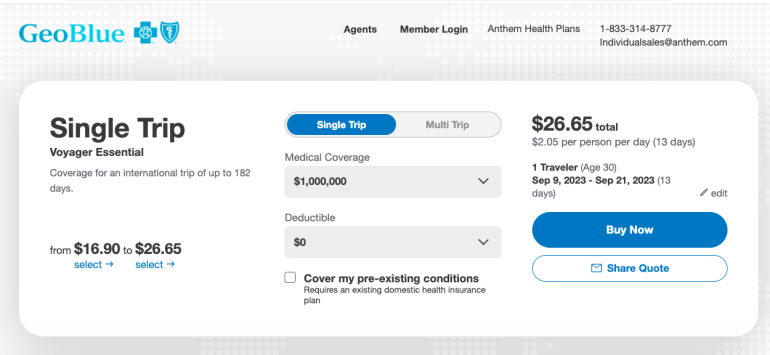

Want higher coverage limits? They’re available. For the same 30-year-old California-based traveler headed to France, GeoBlue's Voyager Essential plan offers $1 million in travel medical coverage with a $0 deductible for $27 — again, that’s for the whole trip, not per day. This plan is not secondary coverage, meaning you can buy it even if you don’t have a primary health insurer.

Emergency medical evacuation due to pregnancy

If you’re traveling to large city, a health care facility is likely a short drive away. But if you’re traveling someplace remote, emergency transportation coverage, like a helicopter, can be a literal lifesaver. Covering this service with an insurance plan can save you a bundle.

Some credit cards give you automatic emergency medical evacuation when you use the card to book your trip, like the Chase Sapphire Reserve®. But if you didn’t use a credit card with emergency evacuation coverage or need higher limits, you may want to buy travel insurance. Most comprehensive plans include emergency medical evacuation insurance, but make sure it’s covered before you purchase your plan.

» Learn more: The best credit cards for travel insurance benefits

Where to buy insurance for traveling while pregnant

Different travel insurance companies have a variety of plans with varying coverage.

A policy from Travel Guard that was perfect for your nonpregnant friend when she traveled to Machu Picchu may not be as good as a policy from Travelex or Nationwide if you’re pregnant and cruising through Europe. Comparison shop and carefully note what’s covered and the deductible limits before you buy.

» Learn more: The best travel insurance companies

Travel insurance while pregnant recapped

You may not need travel insurance for pregnancy, especially if you’re traveling domestically and your trip is fully refundable — but don’t assume that’s always the case.

Read up on your existing coverage from your health plan and any insurance offered by your credit card. Then you can explore a little more of the world before baby arrives, knowing you’re covered for any scenario.

How to maximize your rewards

You want a travel credit card that prioritizes what’s important to you. Here are our picks for the best travel credit cards of 2024, including those best for:

Flexibility, point transfers and a large bonus: Chase Sapphire Preferred® Card

No annual fee: Bank of America® Travel Rewards credit card

Flat-rate travel rewards: Capital One Venture Rewards Credit Card

Bonus travel rewards and high-end perks: Chase Sapphire Reserve®

Luxury perks: The Platinum Card® from American Express

Business travelers: Ink Business Preferred® Credit Card

on Chase's website

1x-10x

Points60,000

Points

on Chase's website

1x-5x

Points60,000

Points

on Chase's website

1x-2x

Points50,000

Points