National Bank Mortgage Rates

Current National Bank discounted mortgage rates

Term | Rate | APR |

|---|---|---|

1-year (fixed, uninsured) | 5.49% | 5.61% |

2-year (fixed, uninsured) | 4.84% | 4.91% |

3-year (fixed, uninsured) | 4.69% | 4.74% |

4-year (fixed, uninsured) | 4.79% | 4.83% |

5-year (fixed, uninsured) | 4.84% | 4.88% |

5-year (fixed, insured) | 4.69% | 4.73% |

5-year (variable, uninsured) | 4.10% | 4.14% |

7-year (fixed, uninsured) | 5.26% | 5.29% |

This table is updated daily on weekdays using data available on the National Bank of Canada website.

Current National Bank posted mortgage rates

Term | Rate | APR |

|---|---|---|

1-year (fixed, uninsured) | 5.49% | 5.61% |

2-year (fixed, uninsured) | 5.24% | 5.31% |

3-year (fixed, uninsured) | 6.05% | 6.10% |

4-year (fixed, uninsured) | 5.99% | 6.03% |

5-year (fixed, uninsured) | 6.09% | 6.13% |

5-year (variable, uninsured) | 4.45% | 4.74% |

6-year (fixed, uninsured) | 6.40% | 6.44% |

7-year (fixed, uninsured) | 6.40% | 6.43% |

10-year (fixed, uninsured) | 6.80% | 6.83% |

This table is updated daily on weekdays using data available on the National Bank of Canada website.

National Bank prime rate

As of Oct. 30, 2025, National Bank’s prime rate is 4.45%.

National Bank’s prime rate is the basis for its variable-rate lending products, like mortgages, credit cards and lines of credit. When the Bank of Canada adjusts its overnight rate, National Bank’s prime rate will increase or decrease by the same amount, affecting the cost of borrowing for these products.

National Bank at a glance

The National Bank of Canada was founded in Quebec City in 1859. Despite being the smallest of Canada’s Big Six banks, National Bank remains the largest bank in Quebec. It employs almost 30,000 employees across 120 countries.

Although it’s dwarfed by other major banks like RBC and TD, National Bank’s mortgage business is considerable. In the second quarter of 2023, National Bank’s Canadian residential mortgage portfolio, including home equity lines of credit, was $113 billion.

National Bank mortgages: things to consider

National Bank mortgage products

In addition to providing traditional mortgage products, including fixed- and variable-rate loans that may be structured as either open or closed, National Bank also offers:

Posted rates vs. special rates

Large lenders like National Bank often provide two sets of current mortgage rates: posted rates and special, or discounted, rates.

National Bank posted mortgage rates

National Bank’s posted rates are the pre-discounted mortgage rates the bank makes publicly available. Posted rates can be much higher than discounted rates, with the expectation that borrowers will negotiate them down.

There are various theories around why this is the case at major lenders. Some lending experts believe it’s to make borrowers feel a sense of satisfaction at getting a better deal, others wonder if a higher posted rate allows banks to charge stiffer penalties if a person breaks their mortgage contract.

If you’re offered a posted rate when you first walk into a National Bank branch, consider it the beginning of a negotiation — and a great reason to compare offers from other lenders.

National Bank special rates

Special rates are National Bank’s posted rates that have already been discounted, including limited time offers. Under most circumstances, a special rate will be more in line with the rate you’re actually offered.

Even if you’re offered a special mortgage rate at National Bank, don’t be afraid to try and negotiate a lower one.

Fixed vs. variable mortgage rates

When you get a mortgage from a lender like National Bank, you’ll have to make an important choice between a fixed or variable mortgage rate.

Fixed mortgage rates

With a fixed-rate mortgage, your interest rate will remain the same for the duration of your mortgage term. If National Bank offers you a 4.25% five-year fixed mortgage rate in 2025, for example, your rate won’t change until it’s time to renew your mortgage in 2030.

A fixed mortgage interest rate allows you to budget around a predictable monthly mortgage payment for years at a time. But if fixed rates fall during your mortgage term, the only way to take advantage is by breaking your mortgage contract and refinancing at a lower rate. Doing so can trigger steep mortgage prepayment penalties.

Variable mortgage rates

If you opt for a variable rate on your National Bank mortgage, the rate could rise or fall many times during your term. When it rises, more of your monthly mortgage payment will go toward interest; when it falls, more will go toward the principal.

Variable mortgage rates have generally been lower than fixed rates. But in times of high inflation, when variable rates are driven upward by increases to lenders’ prime rates, variable rates can put unexpected pressure on your finances.

From March 2022 to July 2023, for example, homeowners with variable-rate mortgages saw their rates increase 475 basis points. Since one basis point is equal to 0.01%, that means a borrower who secured a variable rate of 2.25% in January of 2022 would be paying 7% in July 2023. That’s not a common occurrence, but it highlights the risk of taking out a variable-rate mortgage during times of economic uncertainty.

Open vs. closed mortgages

Another consideration when getting a mortgage at National Bank is whether to choose an open or closed mortgage.

With an open mortgage, you can increase your mortgage payments or even pay your mortgage in full at any time without penalty. A closed mortgage will impose annual limits on how much you can prepay your mortgage.

Choosing between open and closed mortgages is often a matter of cost. Open mortgages tend to come with much higher interest rates.

Rate vs. APR

When investigating National Bank’s mortgage rates or comparing them to rates from other lenders, it’s best to use the annual percentage rate (APR) provided rather than the interest rate itself.

APR includes any other fees that might be added to the cost of your mortgage, and gives you a more accurate figure with which to calculate your potential mortgage costs.

How to get the best mortgage rate at National Bank

As one of Canada’s federally regulated A lenders, National Bank follows the country’s strict lending guidelines. Convincing the bank to offer you the best mortgage rates might require a little effort on your part, including:

Raising your credit score. A high credit score tells National Bank that you pay your debts on time, which signals less risk. The lower the risk, the lower the mortgage rate.

Making a larger down payment. If you can make a significant down payment, it shows CIBC that you prioritize home ownership and that they can loan you less money. Both interpretations mean less risk for the bank.

Lowering your debt service ratios. If your debt service ratios are high, CIBC may believe that too much of your income is already going toward paying down debt. That’s a potentially risky situation, which the bank may balance out by increasing the rate they offer you.

Shopping around. National Bank may not offer you the best mortgage rate. Take a look at the rates other lenders are charging to find out which one is the best fit.

Negotiating: Ask your National Bank mortgage expert if they can improve on the rate they’ve offered you. Let them know that you’ll consult other lenders before making a final decision.

Getting a mortgage at National Bank

In addition to offering in-person mortgage service, National Bank offers online mortgage prequalifying and pre-approval. Find out how each process works below.

When you hover your mouse over the Mortgages tab on the CIBC site, it looks like the only mortgage processes you can begin online are for pre-approvals, refinances and renewals.

But if you click on “Mortgage Pre-approval,” you’ll have the option to get prequalified or pre-approved.

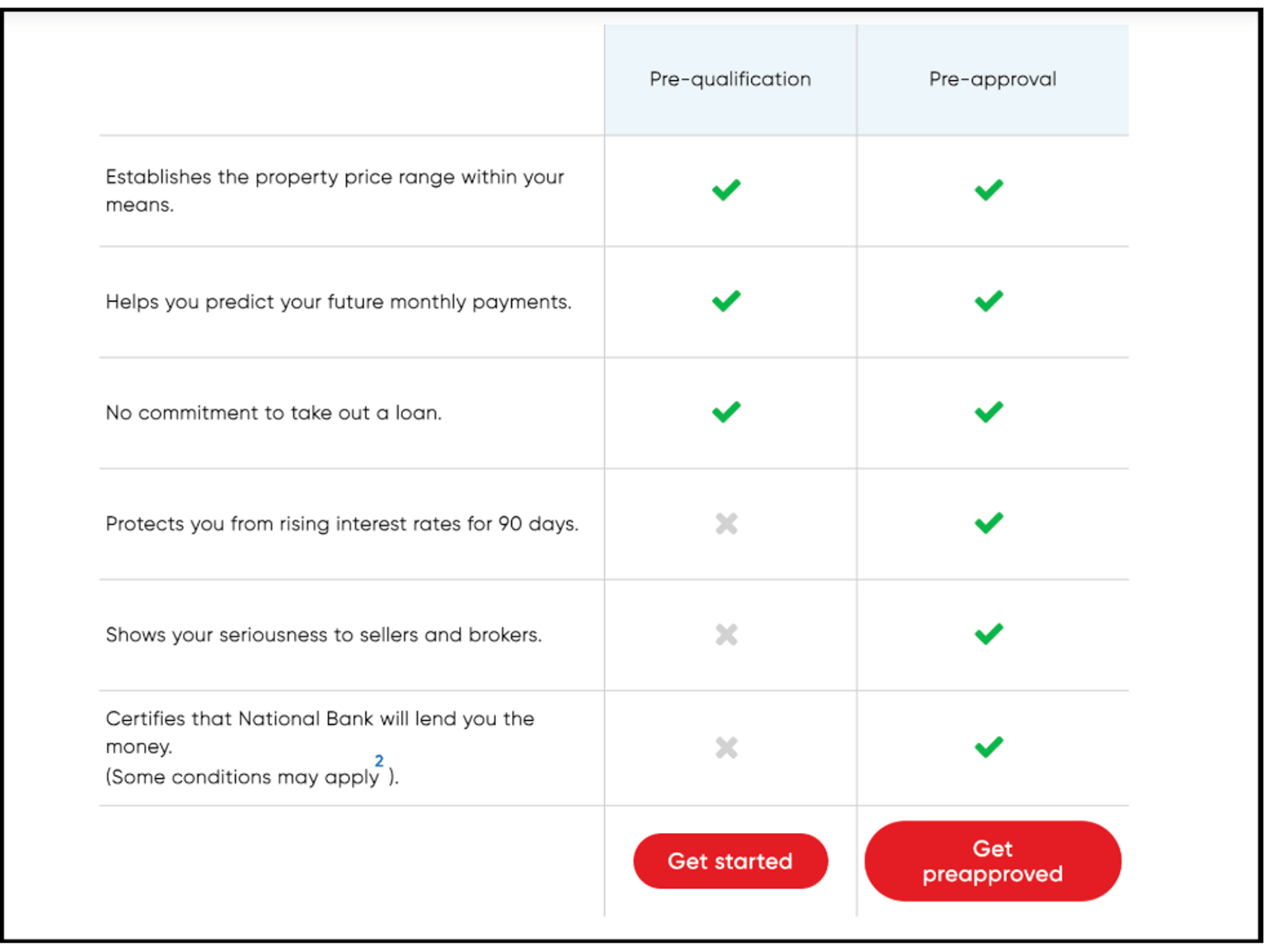

Step 1: From the pre-approval page, scroll down until you see the following graphic and choose “Get started.”

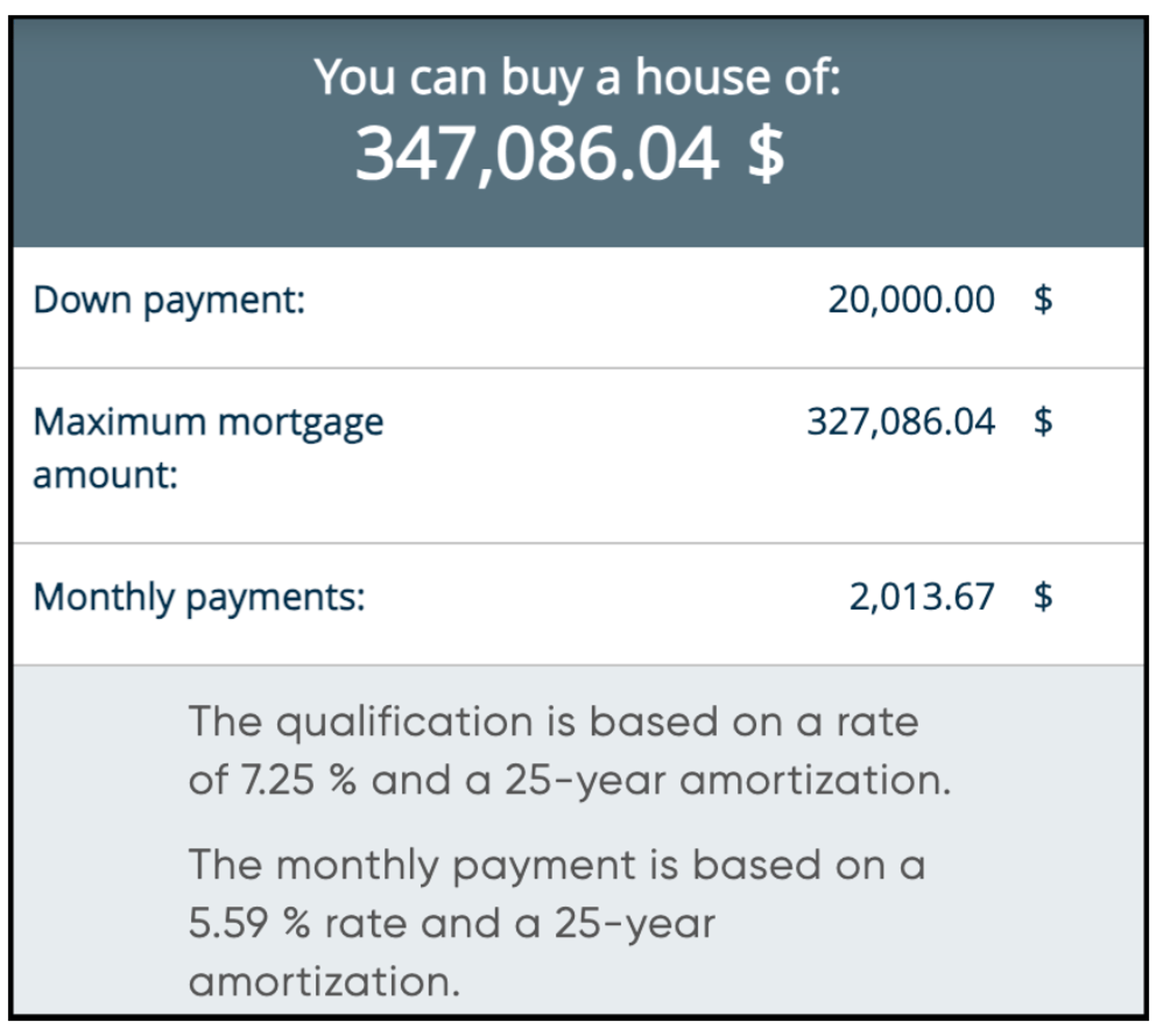

Step 2: Enter your income, down payment amount, monthly debt obligations and home expenses such as taxes and heating costs. You should receive a prequalification estimate as soon as you hit the “Calculate” button.

Step 1: From the pre-approval page, scroll down until you see the following graphic and choose “Get preapproved.”

Once you answer a series of yes/no questions and agree to the terms and conditions, you can start the pre-approval process.

Step 3: Enter some general details about the home you hope to buy, including:

The province it’s located in.

The target purchase price.

How much money you intend to use as a down payment.

Step 2: Enter your personal information, including:

Your name, date of birth and contact information.

Social Insurance Number (optional).

Your address and whether you own or rent your current residence.

When this is complete, you’ll create a profile and move on to the next step.

Step 4: Provide details regarding your income, including:

Your employment status.

Your employer’s name.

Your position.

Your gross annual salary.

How long you’ve held your position.

Step 5: Confirm the information you’ve entered, agree to the bank’s terms and conditions and consent to a credit check. You’re all done.

Frequently asked questions

What is National Bank’s prime rate today?

National Bank’s prime rate is currently 4.45%.

Can you negotiate mortgage rates at National Bank?

You can — and should — negotiate your mortgage rate at National Bank. When you first apply for a mortgage, National Bank may not offer you the lowest rate possible, so it’s always advisable to ask for a lower one. Even if you’re only able to reduce the cost of your mortgage by a little, the money you save can be put toward a better use.

DIVE EVEN DEEPER

Kurt Woock

Kurt Woock

Clay Jarvis

Clay Jarvis Clay Jarvis

Clay Jarvis