PrimeLending Mortgage Review 2024

Many, or all, of the products featured on this page are from our advertising partners who compensate us when you take certain actions on our website or click to take an action on their website. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

- 50+ mortgage lenders reviewed and rated by our team of experts.

- 40+ years of combined experience covering mortgages and financial topics.

- Objective, comprehensive star rating system assessing 120+ categories and 5,000+ data points.

- Governed by NerdWallet's strict guidelines for editorial integrity.

Our Take

3.0

PrimeLending stands out for its wide variety of renovation loans, and it also offers construction-to-permanent loans for new builds. Approval letters can be issued in as little as 24 hours to some borrowers. However, the lender doesn’t post mortgage rates on its website, and it doesn’t offer home equity products.

Pros

- Offers a broad selection of renovation loans to finance cosmetic upgrades or structural repairs.

- Issues loan approval letters within 24 hours to borrowers who qualify.

- Offers resources to connect eligible borrowers with closing cost and down payment assistance programs.

- Receives high marks for customer satisfaction, according to J.D. Power and Zillow.

Cons

- No online mortgage rates — you have to contact the lender for information.

- Rates and fees are on the high side, according to the latest federal data.

- Doesn't offer home equity loans or lines of credit.

Lender | Min. credit score | Min. down payment | |

|---|---|---|---|

620 | 3.5% | Visit Lenderat NBKC at NBKC | |

620 | 3% | Visit Lenderat Guaranteed Rate at Guaranteed Rate | |

620 | 1% | Visit Lenderat Rocket Mortgage, LLC at Rocket Mortgage, LLC | |

620 | 5% | ||

620 | 3% |

Full Review

What borrowers say about PrimeLending mortgages

NerdWallet’s lender star ratings assess objective qualities, including rates, fees and loan offerings. To assess borrowers’ subjective experiences with lenders, NerdWallet has gathered customer satisfaction ratings from Zillow.

PrimeLending receives a score of 735 out of 1,000 in J.D. Power’s 2023 U.S. Mortgage Origination Satisfaction Study. The industry average for origination is 730. (Mortgage origination covers the initial application through closing day.)

PrimeLending receives a customer rating of 4.99 out of 5 on Zillow, as of the date of publication. The rating reflects more than 22,130 customer reviews.

PrimeLending and consumer trust

On March 27, 2024, the U.S. Department of Labor announced that PrimeLending violated federal whistleblower provisions. Investigators from the Occupational Safety and Health Administration found that the company illegally fired two employees who raised concerns about a branch manager pressing them to charge fees to loan applicants when the fees were caused by internal delays.

The department ordered a former senior vice president and two managers to pay $35,000 in emotional damages and legal fees of the employees found to be fired illegally, as well as lost wages and interest.

The lender emailed the following statement: “PrimeLending disagrees with OSHA’s findings and intends to appeal. ... Because the litigation process is ongoing, PrimeLending will not comment on the allegations or their respective claims.”

The Department of Labor’s action against PrimeLending didn’t meet our criteria to deduct points from a lender’s score, so PrimeLending’s NerdWallet star rating was not affected. When shopping for a mortgage lender, do an online search to see if the company is in the news, and why.

PrimeLending’s mortgage loan options

4 of 5 stars

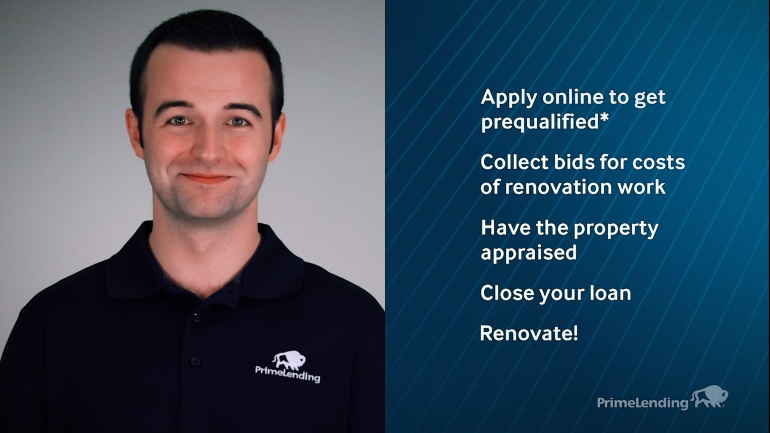

If you’re looking to buy a fixer-upper or finance home renovations, PrimeLending has plenty of experience (and variety) in renovation mortgages. The lender offers a broad selection of loans to help finance cosmetic home upgrades or structural repairs. On the PrimeLending website, a two-minute video explains how renovation loans work and what steps to expect in the process.

Government-backed renovation mortgage options include FHA 203(k) loans through the Federal Housing Administration and VA renovation loans from the Department of Veterans Affairs. On the conventional side, PrimeLending offers Fannie Mae HomeStyle and Freddie Mac CHOICERenovation loans. It also offers some unique loans, including two escrow options to designate funds for home repairs or swimming pool construction.

Other unique offerings from PrimeLending include construction-to-permanent loans, which help finance the build of a new home, and reverse mortgages, which allow seniors to tap home equity to pay everyday expenses. The lender also offers conventional mortgages to purchase manufactured homes, which cost less to build than traditional site-built construction and provide an affordable path to homeownership, especially in rural areas.

Beyond its renovation products, PrimeLending provides conventional and government-backed mortgages to purchase or refinance a home, including VA, FHA and USDA loans. Fixed- and adjustable-rate mortgages are also available for purchase and refinance, as are jumbo loans for higher-priced homes and cash-out refinance options. However, PrimeLending lost some points in our rubric for not offering home equity loans or lines of credit.

» MORE: Best FHA 203(k) mortgage lenders

What it’s like to apply for a PrimeLending mortgage

3.5 of 5 stars

PrimeLending offers mortgages in all 50 states. Applicants can complete the loan process entirely online, uploading documents directly into a secure system, e-signing and receiving reminders and updates along the way. That’s convenient when you’re ready to apply for a mortgage on your own time, without waiting for a loan officer to call you back.

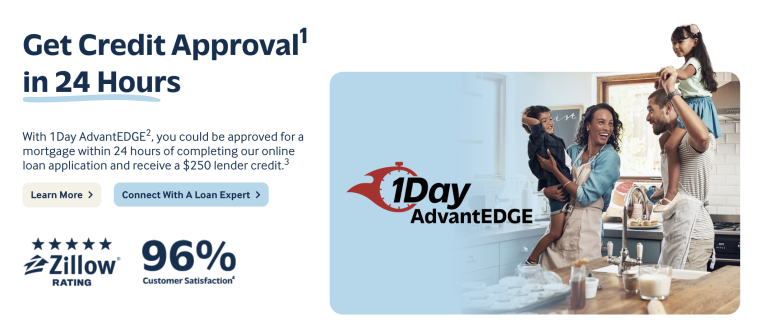

If you have documents ready and want to move quickly, you’re in luck: PrimeLending can issue an approval letter in 24 hours to some borrowers. The program, called 1Day AdvantEDGE, speeds up the process for people who meet certain requirements. For example, you need a predictable source of income (such as a W2) as well as the appropriate credit score and debt-to-income ratio to qualify for a conforming loan.

PrimeLending’s contact information is easy to find on its website. However, the lender lost some points for not offering online chat or a chatbot as a customer service option.

We called the customer service line as part of our research and found it to be mostly helpful, with a short hold time. The customer service agent answered a simple question about VA loans. When we asked a more complex question about mortgage pros and cons, the agent placed us on hold to connect with a loan officer. After a 10-minute wait, we were prompted to leave a message.

PrimeLending does offer a mobile app, but it’s only available to real estate agents and builders, not the general public. Other lenders reviewed by NerdWallet offer Apple and Android mobile apps for borrowers to apply for a mortgage online, view documents and make payments.

» MORE: How to apply for a mortgage

PrimeLending’s mortgage rates and fees

2 of 5 stars

PrimeLending earns 2 of 5 stars for average origination fee.

PrimeLending earns 2 of 5 stars for average mortgage rates.

NerdWallet analyzes federal data to compare mortgage lenders’ origination fees and offered mortgage rates. We measure annual averages across all loan types, as reported by the lenders. Compared to other lenders, PrimeLending’s rates and fees are both on the high side.

Borrowers should consider the balance between lender fees and mortgage rates. While it's not always the case, paying upfront fees can lower your mortgage interest rate. Some lenders will charge higher upfront fees to lower their advertised interest rate and make it more attractive. Some lenders just charge higher upfront fees.

PrimeLending’s mortgage rate transparency

1 of 5 stars

PrimeLending doesn’t offer the option to rate-shop online. The lender prefers to provide personalized rate quotes to applicants through a loan officer rather than posting interest rates on its website.

NerdWallet’s transparency ratings are higher for lenders that post sample rates on their sites, making it easier for home buyers to comparison shop, and highest for sites with self-serve tools that allow shoppers to see what rates might be like for their particular loan.

Alternatives to a home loan from PrimeLending

Here are some comparable lenders we review that borrowers can consider.

New American Funding offers FHA 203(k) loans and provides rates online. Flagstar offers construction loans to help finance new builds.

» MORE: Best mortgage lenders

Explore mortgages today and get started on your homeownership goals

Get personalized rates. Your lender matches are just a few questions away.

Bella Angelos contributed to this review.

More from NerdWallet

NerdWallet’s overall ratings for mortgage lenders are evaluated based on four major categories: variety of loan types (purchase, refinance, fixed and adjustable, for example), ease of application, rates and fees and rate transparency. Among the factors we consider when scoring these categories are options to apply for and track loans online, the level of detail about mortgage rates on lender websites and our analysis of the rates and fees lenders reported in the latest available Home Mortgage Disclosure Act data. These scores generate ratings from 1 star (poor) to 5 stars (excellent).