We believe everyone should be able to make financial decisions with confidence. While we don't cover every company or financial product on the market, we work hard to share a wide range of offers and objective editorial perspectives.

So how do we make money? Our partners compensate us for advertisements that appear on our site. This compensation helps us provide tools and services - like free credit score access and monitoring. With the exception of mortgage, home equity and other home-lending products or services, partner compensation is one of several factors that may affect which products we highlight and where they appear on our site. Other factors include your credit profile, product availability and proprietary website methodologies.

However, these factors do not influence our editors' opinions or ratings, which are based on independent research and analysis. Our partners cannot pay us to guarantee favorable reviews. Here is a list of our partners.

How to Apply for a Mortgage

Our step-by-step guide details the mortgage application process, explaining what you do and what the lender does.

Taylor Getler is a home and mortgages writer for NerdWallet. Her work has been featured in outlets such as MarketWatch, Yahoo Finance, MSN and Nasdaq. Taylor is enthusiastic about financial literacy and helping consumers make smart, informed choices with their money.

Chris Jennings is a NerdWallet editor specializing in home lending topics. He has been writing and editing about mortgages and personal finance since 2016. He enjoys simplifying complex mortgage topics for first-time homebuyers and homeowners alike. Before joining NerdWallet, he wrote and edited content for a number of respected finance brands, including Bankrate, Forbes Advisor, and GOBankingRates.

Born and raised in the Chicago suburbs, Chris earned a bachelor's degree in English from Illinois State University. Chris now calls Los Angeles home, where he lives with his wife, daughter, and their dog.

Updated

How is this page expert verified?

NerdWallet's content is fact-checked for accuracy, timeliness and relevance. It undergoes a thorough review process involving writers and editors to ensure the information is as clear and complete as possible.

You’ve decided to buy a home. Hooray! Now you need a mortgage. Take a breath — it’s not every day you apply for a loan with that many zeros.

Preparation is key, because after your purchase offer is accepted, the clock is ticking. Closing a mortgage transaction takes about 43 days on average, according to Freddie Mac, though certain loan types may take a little longer.

By familiarizing yourself with the mortgage application process, you can be prepared to hit the ground running.

What to do before applying for a mortgage

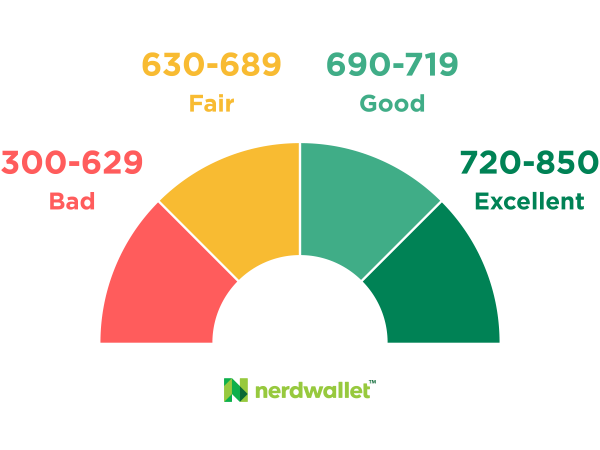

Review your credit report. Checking your own credit is a "soft pull," meaning it does not affect your credit score. You can access free reports from the top three credit reporting bureaus — Experian, Equifax and TransUnion — at AnnualCreditReport.com. Check the report for errors and dispute anything that appears wrong, as this could be holding your score back and cost you thousands in interest down the line.

You’ll also want to know where your credit score will likely stand with lenders. The higher your score, the more likely it is that you’ll be approved for a mortgage — and receive more favorable rate offers.

Explore different types of mortgages. This decision will largely come down to the rate, terms and requirements that best fits your needs.

For example, if you need a mortgage with flexible credit score requirements and a low minimum down payment, you might consider a loan backed by the Federal Housing Administration (FHA). If you know that you’re only planning on being in the home for a few years, you may be interested in taking advantage of the lower introductory rate that comes with an adjustable-rate mortgage.

Research and compare lenders. Shopping around and applying with multiple lenders will allow you to compare offers and find the lowest rate. NerdWallet’s roundup of the best mortgage lenders can be a great place to start your search.

Assemble your loan paperwork. This includes:

Personal information, like your Social Security number and ID

Income verification, such as W-2s and pay stubs (or tax returns, if you’re self-employed)

Federal tax returns

Bank statements

Proof of other debts and assets

Get preapproved to borrow at a given loan amount. This is a sort of preliminary application that you’ll fill out before you start looking at homes. Lenders will review your personal information, such as your credit report, income documentation and assets, to evaluate how much you may be eligible to borrow.

The lender will provide you with a letter detailing these results. When you’re ready to make an offer on a home, this letter can boost the chances of your offering being accepted, since it shows the seller that you can secure financing.

Work with a real estate agent and find your home. Referrals and online searches can be great ways to find real estate agents in the area where you’re planning to move. You’ll want to interview a few until you find an agent that you feel comfortable with — especially if you’ll have unique needs.

For example, if you’re getting an FHA loan or a loan backed by the Department of Veterans Affairs (VA), the home has to meet certain requirements at the appraisal. An experienced agent can steer you toward homes that will meet these standards.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

3%

NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

580

580

Min. down payment

3.5%

First-time home buyers may qualify for 3% down mortgages at Rocket.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

0%

Veterans United offers VA loans for as little as 0% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

580

580

Min. down payment

3%

Rate offers conventional loans with as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

3%

Rocket Mortgage offers conventional mortgages with as little as 1% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

3%

NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

580

580

Min. down payment

3%

AmeriSave offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

600

Min. down payment

N/A

New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

600

Min. down payment

N/A

New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

3%

NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

N/A

No score credit options are available.

Min. down payment

0%

Provides DPA assistance for no down payment options.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

580

580

Min. down payment

3.5%

First-time home buyers may qualify for 3% down mortgages at Rocket.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

0%

Veterans United offers VA loans for as little as 0% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

0%

On VA loans, NBKC offers down payments as low as 0%.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

N/A

No score credit options are available.

Min. down payment

0%

Provides DPA assistance for no down payment options.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

580

580

Min. down payment

3%

Rate offers conventional loans with as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

3%

Rocket Mortgage offers conventional mortgages with as little as 1% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

3%

NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

580

580

Min. down payment

3%

New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

580

580

Min. down payment

3%

AmeriSave offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

600

Min. down payment

N/A

New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

600

Min. down payment

N/A

New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

720

720

Min. down payment

N/A

NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Now that you’ve researched lenders, applied for preapproval and found a home that you’d like to buy, it’s time to actually apply for the mortgage. All in all, the entire process from application to closing could take anywhere from two weeks to two months.

1. Fill out a mortgage application

Use the same documents from your preapproval to apply with one or more lenders. Applying with multiple lenders helps you compare rates and terms, and if you submit all applications within 45 days, it only counts as one credit check. Most lenders nowadays let you apply online or by phone. You may be able to apply in person at a branch location, depending on the lender.

By law, a lender has three business days after receiving your application to give you a Loan Estimate form, a detailed disclosure showing the offered loan amount, type, interest rate and all estimated costs of the mortgage, including hazard insurance, mortgage insurance, closing costs and property taxes.

2. Review your Loan Estimates

Compare terms and costs across your Loan Estimates. Check the interest rate expiration date (top right corner of the first page) and confirm if the rate is “locked” or if it’s subject to change. Ask the lender to explain anything you don’t understand.

🤓Nerdy Tip

Consider locking your rate before closing to avoid surprises. This ensures that you’ll know exactly what you’re paying from your first bill.

The third page of the Loan Estimate includes a helpful “Comparisons” section, which has key information that you can use to compare offers, such as:

Total cost in five years: This is all charges — including interest, principal and mortgage insurance — that you'll incur within the mortgage's first five years.

Principal paid in five years: This is the amount of principal you’ll have paid off in the first five years.

APR: Also known as annual percentage rate. This figure accounts for your interest rate plus any fees or points. Usually, the APR is higher than your interest rate.

Percent paid in interest: This represents how much interest contributed to the final balance of the loan. It's not the same as the interest rate.

After comparing your loan estimates, choose the best fit and contact the lender to tell them you’re ready to move forward. They may ask for additional documentation. You’ll also want to purchase homeowners insurance, as you’ll need it before you can receive final approval.

3. Loan processing takes over

This stage involves a detailed review of your mortgage application, where the lender verifies your financial information and statements. Your lender will order an appraisal of the property to ensure that its value matches the purchase price. Prepare to answer questions and provide additional documents quickly to keep everything moving forward.

You’ll want to avoid any moves that could disrupt your credit. This includes opening any new lines of credit, making any major purchases (like a car), and paying all of your bills on time, as any changes could jeopardize your mortgage approval.

4. The underwriter makes a decision based on your documentation

Now that the lender has verified the information in your application, the underwriter will use it to judge the risk of lending money to you.

What’s your loan-to-value ratio (the mortgage amount relative to the value of the home)?

Do you have the cash flow to make the monthly payments?

What’s your history of making payments on time?

Is the home valued correctly, the condition good and title clear?

Do you have a spotty employment history?

If the underwriter does not have enough information to make a decision on the loan, you may have to provide further documentation.

5. Your loan is cleared to close

In this final step, the lender must act before you can move forward.

With time to spare (hopefully) before your closing date, you hear from the lender with happy news: “You're cleared to close!”

🤓Nerdy Tip

It's a good idea to order a home inspection to assess the property’s condition immediately, even though lenders don't require it. You can get a fuller understanding of the condition of the home, and if something is found to be severely wrong, you may even decide to withdraw your offer. This will cost around $300 to $500.

The lender must send you another federally required form, the Closing Disclosure, three business days before your scheduled closing date. It shows the detailed and final costs of your mortgage.

Compare the Closing Disclosure with your Loan Estimate to check for any changes, and ask your lender to explain anything you don’t understand. If you haven’t locked in your rate yet, you’ll want to do it now.

At this stage, you’ll also arrange how to pay your closing costs, either upfront with a wire transfer or cashier’s check or by rolling them into your loan. Closing costs are typically between 2% and 6% of your loan amount. You can estimate this amount using NerdWallet’s closing cost calculator.