The ideal mix of credit cards looks different for everyone, so it can be tough to know how many cards are too many.

Some people are ready to downsize their credit card lineup right now: One in three Americans with credit cards (33%) say they have too many, according to a recent NerdWallet survey conducted by The Harris Poll.

Strategy matters when cutting back on credit cards. Cards should make it easier to reach your financial goals. Stay focused on those goals — not rewards or annual fees — to know which ones to keep and which ones to cut.

When one card is plenty

At its core, a credit card can be thought of as an instantly approved loan. If someone is short on cash but wants to buy lunch, there’s no need to call a banker to draw up a $14.27 loan. Just present the plastic to the cashier.

But many card users may not need the monetary component of the loan. In other words, they’re likely not using it because they’re short $14.27. Instead, they just need the immediacy of it. No need to run to a bank to get cash. These users likely pay off their balance each month. Indeed, more Americans are not currently carrying revolving debt (50%) compared to those who are (38%), according to the NerdWallet survey. If that convenience is all someone is after, one card might be enough.

When multiple credit cards make sense

For some, one card isn’t enough. Americans were using 792.9 million credit cards at the end of 2024, or about 3.3 cards for every adult 25 and older, according to the Consumer Financial Protection Bureau. But having two credit cards instead of one doesn’t necessarily double the convenience factor.

One incentive for multiple accounts is credit card rewards. From the card company’s perspective, these benefits drive card sign-ups and can persuade owners to keep and use their card over others. From a user’s perspective, these perks can be worth hundreds of dollars in value.

Power users often take optimizing their card lineup to the next level, tracking dozens of cards and chasing sign-up bonuses to juice their point balances. But that’s not the only way to approach credit card perks.

Rewards on groceries can make shopping for essentials a little bit cheaper. An airline card offering free checked bags can save frequent travelers a lot with just a little effort. Cash-back cards are great for those who want to keep things simple.

What the Nerds do

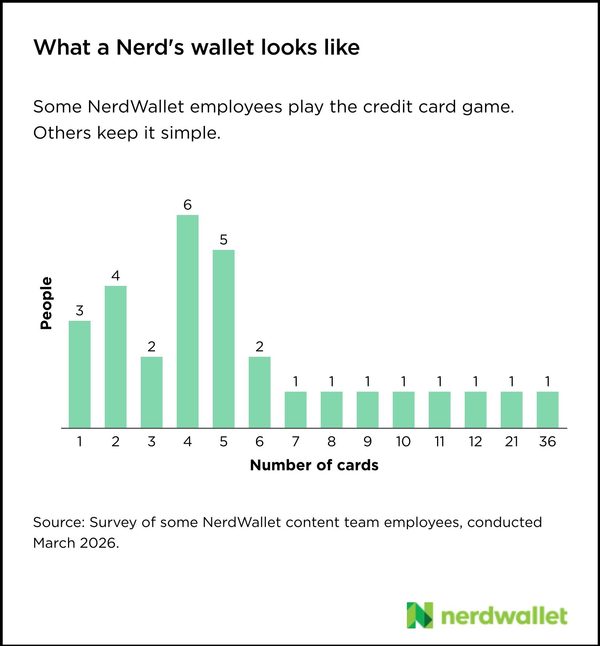

To illustrate how the “right” number of cards can vary a lot in practice, even among people who study personal finance for a living, 30 members of NerdWallet’s content team responded to a poll about the credit cards they carry.

The average number of credit cards per “Nerd” was 6.4. But that average was heavily influenced by just a few points and miles enthusiasts. The number of Nerds with three or fewer cards was almost double the number of Nerds who had 10 or more.

Craig Joseph is a travel writer at NerdWallet and an exemplar of a maximalist approach: His stack of three dozen cards is over 1.5 inches tall. “Optimizing card rewards has been an industrial-scale hobby and part of my personal finance plan for almost 15 years,” he says. “Since the rewards I earn are used exclusively for travel, I don’t need line items in my budget for flights and hotels. It takes a lot of tracking, but it works well for me.”

Laura McMullen, an editor at NerdWallet, has a different mindset: She keeps just two cards. “I know myself, and I don’t want to think much about my credit cards,” she says. “Maximizing isn’t fun for me, so I stick with two highly rated cards that earn strong rewards without much decision-making on my end.”

When enough is enough

One rationale for limiting the number of cards is that using credit can result in higher spending. The majority of Americans (84%) say it’s easy to overspend when using a credit card, according to the NerdWallet survey. A history of overspending may be a good reason for someone to focus on managing credit card debt instead of finding the next card, even if that means passing up an appealing sign-up bonus. If credit card usage is already under control, finding the right number to own may come down to weighing trade-offs, specifically money and time.

Maximizing credit card rewards can require diligence, discipline and time. And with annual fees for high-end cards approaching $1,000, the juice might not be worth the squeeze. Card owners can easily recoup that fee if their spending habits align with the card’s benefits. But if those perks go unused, or if they persuade people to spend money they otherwise wouldn’t, that same fee may be expensive.

Downsize with a plan

If a card no longer contributes to your financial goals or wellbeing, it may make sense to get rid of it, even for a person who doesn’t mind managing a thick stack of cards.

When pruning your wallet, be smart about it:

- Start by naming your financial goals. Obtaining miles, points and perks isn’t the end goal. The goal is whatever those benefits are used for. That could mean upgrading an upcoming trip to more luxurious accommodations. It could mean the ability to string together more cheap travel. It could mean saving money on gas. A pile of points is useless if it doesn’t get a person closer to what they’re after in the first place.

- Prepare for the possible credit hit. Closing a credit card can temporarily hurt your credit, as it plays into three important components: the length of your credit history, your total available credit and your credit mix. Keep this in mind when you’re choosing which card to close — a newer card with a lower credit limit may do less damage.

- Take stock of major upcoming purchases. A person planning to apply for a mortgage or any other loan in the near future shouldn’t make any credit-altering changes until after the purchase.

- Consider all options. If canceling primarily because of a high annual fee, see if the card company can transfer the account to a no-fee card. Keeping the account, and its spending limit, results in a higher overall amount of total available credit, which is generally good for credit scores.

Article sources

NerdWallet writers are subject matter authorities who use primary, trustworthy sources to inform their work, including peer-reviewed studies, government websites, academic research and interviews with industry experts. All content is fact-checked for accuracy, timeliness and relevance. You can learn more about NerdWallet's high standards for journalism by reading our editorial guidelines.

- 1.Consumer Financial Protection Bureau. Market Snapshot: Consumer use of State payday loan extended payment plans. Accessed Mar 4, 2026.