Each month, NerdWallet suggests one wallet win to help you feel more confident about your money. This month’s topic is budgeting, and we’re going to turn our finances around together in an hour or two.

I’m a NerdWallet writer and I have a confession to make. I don’t have a budget.

Well, I did. There was a spreadsheet at one point. I loosely followed it, but lost my diligence. My current financial habits make me think I need to find it again (the spreadsheet and my diligence).

Here’s what my wife and I recently realized:

- Our monthly credit card balances are out of control. We pay them in full each month, but gasp at the total spend every time. Sometimes, we take from savings to cover it all.

- We just sent the final payment (of three) for our upcoming weeklong rental at the beach. We never budgeted for it, and, again, had to take money from savings.

- We have three kids, and our two bigger kids are attending various day camps all summer long. Neither of us knows the total cost.

I asked Valerie A. Rivera, a certified financial planner in Chicago and founder of FirstGen Wealth, what she thought of situations like mine. She posed this question:

“What does it cost to run your life in a normal month?”

I was like, “Dang, I guess I really don’t know anymore.”

I mean, I’m in an expensive season of life with a mortgage, one kid still in day care, and astronomical utility bills. I know I can do better, though.

Maybe you’re in the same boat. Let’s get back on track this month. It’ll only take an hour or so and a pitcher of iced tea.

Meet MoneyNerd, your weekly news decoder

So much news. So little time. NerdWallet's new weekly newsletter makes sense of the headlines that affect your wallet.

Action: Review your monthly spending

“When I ask people what they spend, they never know,” Rivera says.

I hate that I can relate. Time to look at the numbers.

Grab your beverage, sit down with your significant other (or yourself) and jot down the major monthly expenses.

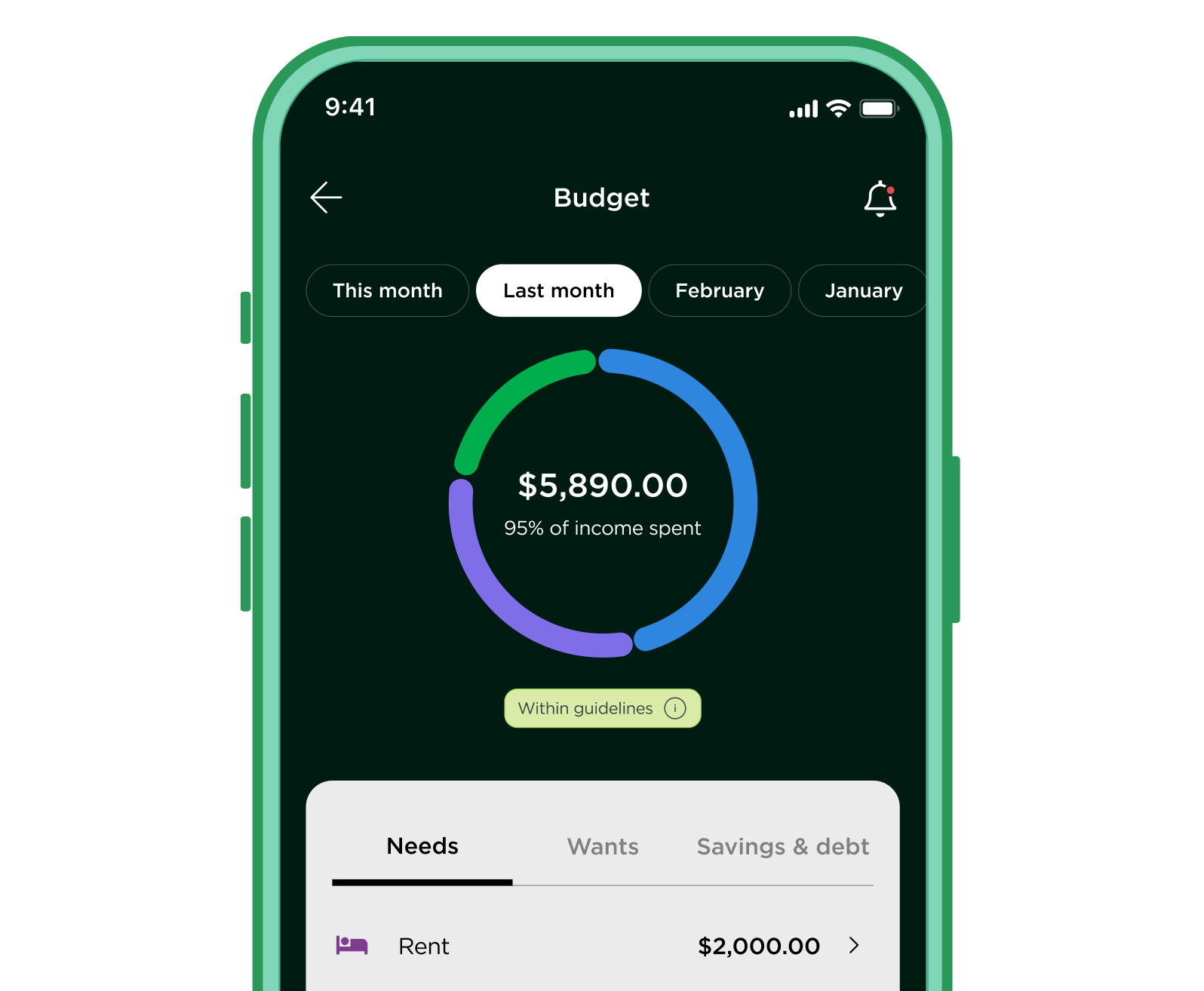

NerdWallet’s app has a 50/30/20 feature that lets you see how much of your money is going into needs, wants and savings.

The budgeting framework suggests using 50% of pay for needs, 30% for wants, and 20% for savings and paying off debt.

As an example, if you bring home $5,000 per month, you have $2,500 for necessities, $1,500 for wants and $1,000 for savings and extra debt payments.

Keep those suggested percentages in mind as you note the big stuff — like rent or mortgage, day care costs, car payment(s), utility bills and any other loans.

Next, go over recent credit and debit spending with a fine-tooth comb. Look at statements online or link your accounts in the NerdWallet app for an automatic needs vs. wants analysis.

Now that you know what you spend in a typical month, how does the total compare with your income?

If it turns out you’re spending, say 60% on needs, that’s OK. The 50/30/20 budget is a guideline to get you started. If you live in a high cost of living area, or are paying a child care bill that feels like a second mortgage, you can adjust your percentages.

The main thing is to take time to look, Rivera says. “That’s the step that moves you forward.”

Action: Bring bigger expenses into the broader budget

Refill your glass and start talking about “lumpy spending,” as Rivera calls it.

My wife and I neglected to plan for our summer vacation and camp costs ahead of time, and now we’re feeling it.

Lumpy spending examples are the hefty expenses — like a big trip later in the year — that you can get in front of.

Break those expenses into a monthly amount you can spread out, Rivera says. Once you do, you can automate a monthly transfer from your bank account into a special bucket or sinking fund.

This creates consistency in your monthly cash flow and provides permission to enjoy, Rivera says.

Your budget builds itself, instantly

Action: Create new habits to keep yourself honest

With the numbers coming more into focus, I need to get a handle on our “fun mon” spending. This is a great use case for 50/30/20.

We have a healthy emergency fund and minimal debt beyond our house and car payments, so I’m looking closely at “wants.”

I used the budget calculator and realized we were spending more like 40% on wants every month. My goal is to get it down to the recommended 30%, which I think is possible.

We do most of our damage with credit cards, and I love Rivera’s idea for being more intentional about this kind of spending.

Don’t wait for the due date to pay your bill because that puts you a month behind, she says.

“What I advocate for people is to pay it off as paychecks come in, or on a weekly basis.”

I’m going to do this with all three of our credit cards. And I’ll do so with my specific “wants” limit fresh in my mind. I bet I’ll spot “spend creep” sooner.

There was a time I had a better handle on this stuff. Heck, I’ve even found and written about real ways to cut back on needs. I’m ready to be a little more intentional again.

Your mission this month

Take these tasks to heart today and I know you’ll feel better:

- Take a look at baseline spending: Tally up your major bills and non-negotiable expenses to find out exactly what it costs to run your life in a normal month.

- Apply the 50/30/20 rule: Plug your income into a calculator or download the NerdWallet app to set clear limits for your needs (50%), wants (30%), and savings or debt payments (20%).

- Manage "lumpy" expenses for the long-term: Estimate the annual cost for large, irregular bills or trips, divide that number by 12, and automate a monthly transfer into a dedicated savings bucket.

- Pay credit cards weekly or biweekly: Maintain real-time awareness of your cash flow and wants limit by paying off your credit card as paychecks come in, rather than waiting for the monthly due date.

Go forth and budget. Oh, and make my iced tea an IPA, please.

If you’re following along with us on this monthly financial challenge, start by testing out the tips we shared today over the next few weeks. We’ll be back again next month to learn how to break the pricing algorithm. And if you missed last month’s edition, take a look back at how to review your insurance coverage.