This article originally appeared in NerdWallet's investing newsletter, the Nerdy Investor. You can subscribe for free here.

On April 30, President Trump signed an executive order to set up TrumpIRA.gov, an online marketplace "designed to connect American workers who do not have access to employer‑sponsored retirement plans with high-quality, low-cost IRAs offered by private-sector financial institutions.”

The order provides some information on how the new program might work and teases a $1,000 annual government match for qualifying retirement savers, but the key details won't be set in stone until the website officially launches by January 2027.

Here's what we know so far — and what two certified financial planners say you should keep in mind as the program takes shape.

What is the Trump IRA program?

In contrast to the recently launched Trump Accounts, the new “Trump IRA” program doesn't appear to be a government-run investment account. Instead, the executive order describes the forthcoming TrumpIRA.gov website as more of a web portal or shopping tool for IRAs.

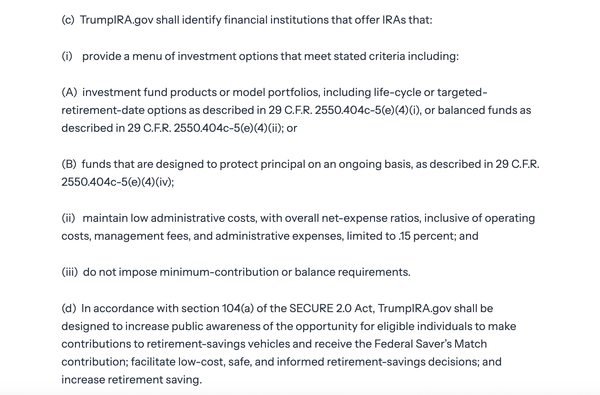

The excerpt below contains the meat of the order:

The site will help people filter for IRAs that have no minimum contribution or balance requirements, have minimal expense ratios (below 0.15%) and offer a variety of fund choices such as target-date funds, balanced funds (typically a fund that holds a fixed ratio of stocks and bonds) and principal protection funds (conservative funds made up mostly of bonds).

What's the deal with the $1,000 match?

One feature of the TrumpIRA.gov executive order that has caught some media attention is the mention of an “easy and transparent way for eligible workers to obtain up to a $1,000 match for their savings.”

A little more digging reveals that this $1,000 match isn’t a new program — it refers to the Saver’s Match program, an initiative ushered in by the Secure 2.0 Act that will replace the older, nonrefundable saver’s credit in 2027. And it has some pretty tight income limits to boot.

Under the Saver’s Match program, taxpayers whose modified adjusted gross income (MAGI) is below $20,500 (single) or $41,000 (married filing jointly) can get a 50% match from the federal government on their first $2,000 of retirement plan contributions. Above that income, taxpayers will get a reduced match, and the match phases out entirely for single taxpayers with MAGIs above $35,500 or married taxpayers with MAGIs above $71,000.

Even if you don’t qualify, there are other ways to get some “free money” in your IRA. Many IRA providers offer account-opening bonuses for investors who meet certain minimum deposit requirements. On top of that, several have started offering small contribution matches, usually as retention programs (i.e., you can keep the matching dollars only if you keep your funds in the IRA for a certain number of years). NerdWallet has a roundup of the best brokers for IRA matching to help you compare these options.

What do financial advisors think of TrumpIRA.gov?

Christopher Giambrone, a certified financial planner based in New York, said in an email interview that for many people, the hardest part of retirement planning is simply starting to save. TrumpIRA.gov could help with that, if it's designed well.

"A lot of individuals know they should be saving, but they get overwhelmed by the choices, or assume they need a large amount of money to get started. If this can cut through some of that noise and present a handful of reputable options in a way that is easy to compare, that would be a meaningful benefit. Sometimes the difference between someone saving and not saving comes down to whether the first step feels manageable," Giambrone said.

Joon Um, a California-based certified financial planner, praised the low-cost and no-minimum requirements proposed for accounts on TrumpIRA.gov in an email interview, but added that other criteria also matter to investors just starting to save for retirement. "Education and ease of use are equally important. Even good IRA options don’t help much if people don’t understand how to contribute or stay invested long term," Um said.

TrumpIRA.gov may very well be the first government website to let investors shop for IRAs, but there are already several similar tools available now.

NerdWallet’s roundups of the best IRAs and best Roth IRAs make it easy to compare IRAs based on fees, account minimums, educational resources, and promotions such as opening bonuses and contribution matches. They also feature reviews and analysis from our writers, who have thoroughly researched these IRA providers and tested their investment platforms.

Will this program last, or will it meet the same fate as MyRA?

Trump is not the first president to try to incentivize IRA use. His predecessor, Barack Obama, established the “MyRA” in 2015 to promote Roth IRA use among lower-income Americans; however, the program never quite caught on and was quietly shuttered by the first Trump.

MyRAs closely resembled Roth IRAs in that they shared the same income and contribution limits. However, they could only be funded up to a maximum balance of $15,000. They could also be invested only in Treasury securities in order to provide a sort of risk-free starter account that participants could later roll into a standard Roth IRA with more investment choices.

Fewer than 40,000 MyRA accounts were ever opened during the program’s lifetime, and about 10,000 were never funded. Among those that did have money in them, the median balance was just $500.

The first Trump administration cited the program’s high costs — $70 million in its first two years, with a projected $10 million per year thereafter — in its decision to shut it down in 2017. The MyRA phaseout process was completed in 2018, whereupon all remaining funded accounts were automatically rolled into private-sector Roth IRAs.

TrumpIRA.gov is slated to be very different from the MyRA program and might fare better as a result. It is designed to connect investors to regular IRAs offered by private-sector financial institutions, which won't have the same investment and balance restrictions as MyRAs did. And the Saver's Match of up to $1,000 per year could make them more popular among lower-income Americans than MyRAs were.

"The $1,000 Saver’s Match is interesting because people usually respond better to a direct match than just a tax deduction. The biggest challenge will probably be awareness and simplicity. Programs like MyRA never really gained traction because many people either never heard about them or didn’t fully understand them," Um said.

More decisions and more complexity

It’s too early to speculate about how popular the proposed Trump IRA program will be or how much it will cost the government, as its details could change before implementation. But in general, investment initiatives like this can mean new decisions to make and greater complexity in financial planning for some people.

If you’re feeling overwhelmed by all the choices and don't know where to start, NerdWallet's five-step guide to retirement planning may be worth a look.

Explore more on

Article sources

NerdWallet writers are subject matter authorities who use primary, trustworthy sources to inform their work, including peer-reviewed studies, government websites, academic research and interviews with industry experts. All content is fact-checked for accuracy, timeliness and relevance. You can learn more about NerdWallet's high standards for journalism by reading our editorial guidelines.

- 1.The White House. Promoting Retirement-Savings Access for American Workers by EstablishingTrumpIRA.gov. Accessed May 14, 2026.

- 2.Congress.gov. The Retirement Savings Contribution Credit and the Saver’s Match. Accessed May 12, 2026.

- 3.U.S. Department of the Treasury (Archived). U.S. Treasury Launches myRA (my Retirement Account) to Help Bridge America’s Retirement Savings Gap. Accessed May 12, 2026.

- 4.New York Times. Treasury Ends Obama-Era Retirement Savings Plan. Accessed May 13, 2026.

- 5.Treasury Direct. The myRA Program Has Been Phased Out.. Accessed May 12, 2026.