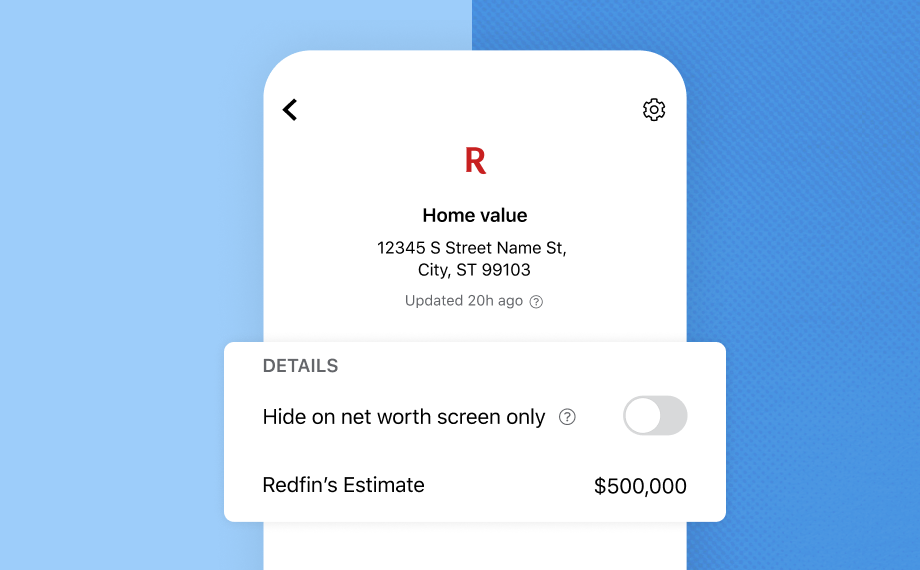

We regularly update your home's current value to reflect the latest market conditions, which you can check anytime.

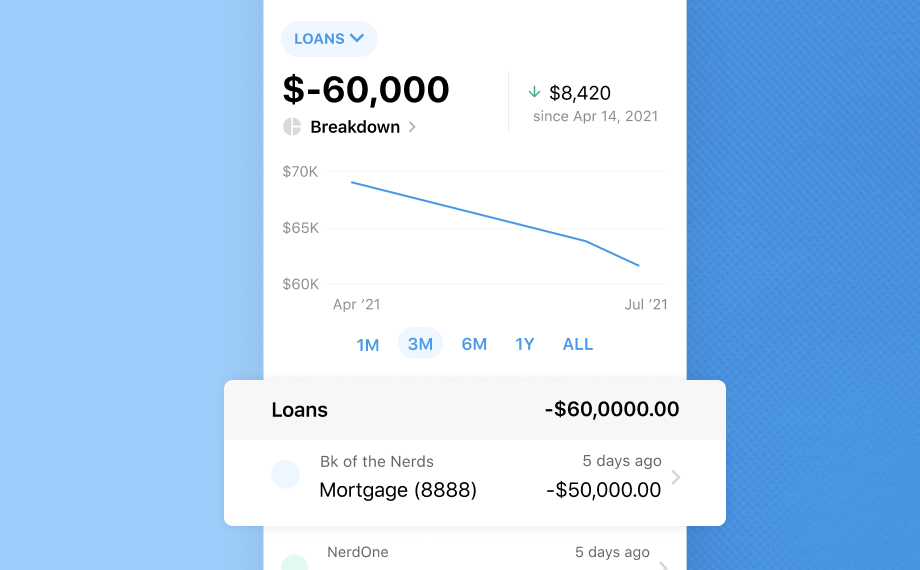

Quickly see the total remaining balance on your mortgage alongside your other loans to see how much you owe.

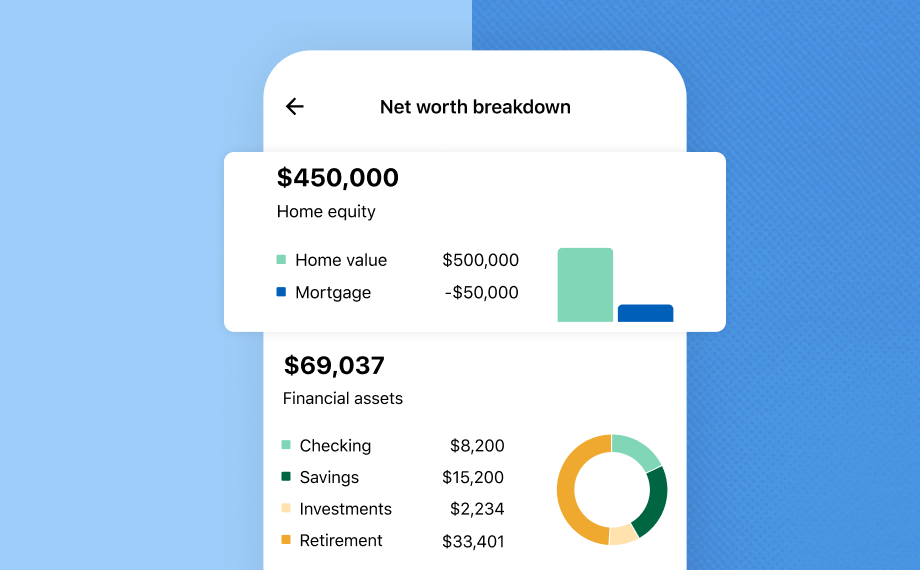

Get a holistic view of your home equity including its current market value, how much you owe – and more nerdy insights like historical value.

Home value has a slightly different meaning if you ask a homeowner, appraiser or tax assessor. But in most cases, home value means the amount for which a house would likely sell, otherwise known as the current market value. Mortgage lenders — as well as buyers and sellers — typically rely on professional property appraisers to calculate market value, but there are ways to determine home value on your own.

A home appraisal is an objective estimate by a professional appraiser of how much your home is worth. To find the value, an appraiser visits your home, takes a detailed inventory of the property and researches the local real estate market. The estimate is based on many factors, including recent sales of comparable homes; neighborhood characteristics; and age, size and condition of the home.

The home value calculation uses data gathered by Redfin. To calculate the Redfin Estimate, Redfin considers hundreds of data points about the market, the neighborhood, and the home itself, like whether it has a water view or is located on a busy street. Keep in mind, these estimates of how much your home is worth are only a starting point. Hire a professional appraiser or get a comparative market analysis from a qualified real estate agent before buying or selling.

Home equity is the value of your home minus the balance of your mortgage. To put it another way, home equity represents the portion of the house you’ve “paid off” and therefore own. Equity increases slowly with each mortgage payment, but may grow faster if you make value-boosting home improvements or if home values rise in your area. As a homeowner, equity is a valuable asset that directly affects your financial freedom. More equity means more ways to achieve financial goals. You can make home improvements, consolidate debt, cover emergency expenses or even pay college tuition by tapping home equity. Don’t cash out or borrow against home equity just because you have it, though. Tapping equity can add years to your mortgage payoff and means less cushion if the home loses value. And if you have trouble paying the loan for any reason, such as losing your job, the lender could foreclose on your house. You can tap your home equity with the following loans: • Cash-out refinance: Mortgages your house for more than you owe. You can generally turn 80% to 90% of your home’s equity into cash, and in some cases, get a lower interest rate than your previous mortgage. • Home equity loan: Allows you to borrow up to 85% of your equity at a fixed interest rate. Home equity loans are disbursed in a lump sum and repaid through monthly payments. • Home equity line of credit (HELOC): Allows you to borrow up to 85% of your equity at a variable interest rate, which means your payments could change every month. Instead of a lump sum of cash, HELOCs provide a limited line of credit you can borrow when needed, much like a credit card. Interest is paid only on the amount you take out.

Unlike other assets, such as your car, a home often appreciates over time. In general, real estate appreciates because there’s only so much space for new development. As time goes on, there’s generally more demand for less land, driving up value. If demand drops, however, prices could go down. Other factors that can influence changes in home value are: • How much the house sold for in the past • Quality of the neighborhood • Market conditions, such as the number of homes available and strength of the economy • Tax assessment • Nearby amenities • Square footage • Age and condition of the house and property

Home value can be affected by factors beyond your control, but you can still manage the ongoing costs of homeownership. These include: • Mortgage payments: Choosing a longer mortgage repayment period (30 years instead of 15 years, for example) yields smaller monthly payments. So does a bigger down payment. After you purchase a home, you may be able to reduce payments by refinancing or negotiating a lower tax assessment. • Insurance: Compare homeowners insurance rates from different insurers to find the best price and coverage. Choose a policy that’s tailored to your needs rather than simply picking standard coverage. Buying homeowners insurance from your current auto insurance company may earn you a discount. Some home improvements, like a new roof or security system, may also yield lower insurance premiums. • Utilities: Stop energy waste by boosting home efficiency. Make your energy bills more affordable by switching to LED lights, properly insulating or replacing old appliances with energy-efficient ones, for example. If you're not sure where to start, ask your utility provider about a home energy audit. • Mortgage insurance: Private mortgage insurance, or PMI, is typically required for conventional loans when the down payment is less than 20%. You can ask your lender to remove PMI as soon as you reach an 80% loan-to-value ratio, and making additional loan payments will get you to the sweet spot sooner. Also, if you think your home’s value has increased substantially since you bought it, you can pay for an appraisal to see if you’ve achieved 20% equity. If so, you may be able to refinance and cancel PMI. If you have an FHA loan with mortgage insurance, cancellation is still possible but may have different requirements. Talk with your lender to explore your options. • Home improvements: Repairs and upgrades can increase your home’s value, and choosing DIY home improvements can help reduce costs. Smaller projects, such as a minor kitchen remodel or a new front door, often have the best return on investment.

Refinancing replaces your existing mortgage with a new loan. Some reasons for refinancing are directly related to home value, while others aren’t. Refinancing might be a good idea if you want to: • Lower your interest rate: If mortgage interest rates drop after purchasing your home, refinancing could allow you to lock in a lower rate, reducing your monthly payment. • Change your loan term: Refinancing into a shorter-term loan, for example 15 years instead of 30, may increase your monthly payment, but it will also reduce payback time so you pay less in interest and own your house sooner. • Drop mortgage insurance: Refinancing can remove mortgage insurance in two ways. First, you can refinance from an FHA loan (these loans always carry mortgage insurance) to a conventional loan without paying PMI if you have built up over 20% equity on your existing loan. Second, you can refinance from a conventional loan with PMI to another without it if your current home value and mortgage balance puts you over the 20% equity mark. • Pull cash out of your home: As you pay down the loan and your home gains value, equity increases. When your equity stake is large enough, you may be able to turn some of it into cash through a cash-out refinance. Use our mortgage refinance calculator to see how much a refinance could save you and get customized lender recommendations.

Unfortunately, it’s not yet possible to self-report or edit your mortgage information, but we are working on adding this functionality soon!

If you have any feedback, please email us at [email protected]. We appreciate any feedback you have and will use it to inform how we invest in this experience.