After you apply for a mortgage, be sure to keep your eye out for the Loan Estimate, an official document from the lender.

Reading and comparing Loan Estimates from different lenders will help you understand the terms and costs of getting a home loan — and potentially help you save money.

What is a Loan Estimate?

A Loan Estimate is a three-page government-mandated document that spells out the terms of a mortgage offer.

To get a Loan Estimate you must provide a lender with:

- Your name

- Income amount

- Social Security number

- Address of the property you want to buy

- Estimated value of the property

- Requested loan amount

Once you've applied with this information, the lender has three business days to provide a Loan Estimate.

Although you don't have to give more information about your finances at this stage, the Loan Estimate will be more accurate the more details you provide, such as the amount of debt you carry and the type of mortgage you're interested in.

Reading a Loan Estimate

A Loan Estimate details the terms of your loan, including:

- Expenses, with clear “yes” or “no” answers to important questions, such as whether each amount can increase after closing, whether your loan includes a prepayment penalty or a balloon payment and which expenses are included in your escrow account.

- The projected monthly mortgage payment, including taxes, insurance and other assessments.

- Estimated closing costs and the amount of cash you’ll need to have on hand at the time of settlement.

- Information on services you can, and cannot, shop for — such as pest inspections, survey fees and the home appraisal.

Did you know...

The lender must give a new Loan Estimate if key information changes. For example, if the property appraisal comes in lower than expected, the loan offer may change and require a new Loan Estimate. Or a new Loan Estimate might be necessary if your credit standing changes and you no longer qualify for the terms of the original loan offer.Comparing Loan Estimates

The Loan Estimate also offers data that can help you compare loan offers from multiple lenders. The information to compare includes the total costs of third-party services, the annual percentage rate (APR) — your interest rate including fees — and the amount of interest you’ll pay over the loan term, expressed as a percentage of your total loan amount.

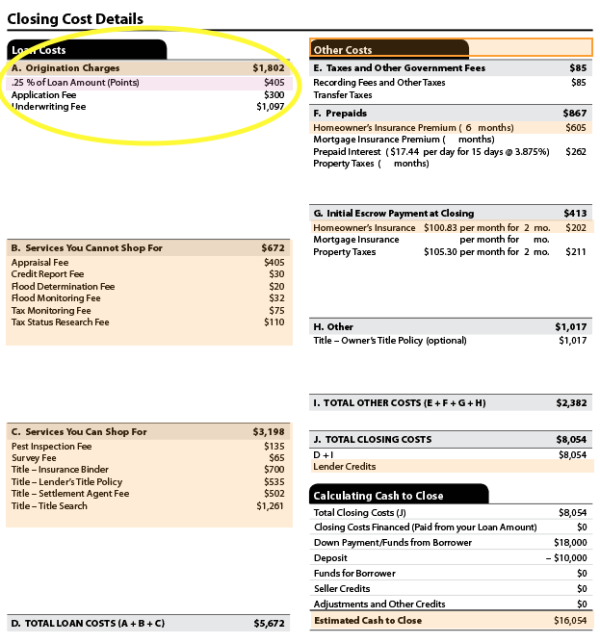

One important section to look for is at the top of Page 2, on the left-hand side of the page. That's where you'll see "Loan Costs" and "A. Origination Charges." You'll find two types of charges here:

- Lender fees can have several different names, including "application fee" or "underwriting fee," as shown. You'll want to compare these origination fees among the lenders you're shopping.

- Discount points are prepaid interest that you have the option of paying to reduce your interest rate. In the example below, an annotated screenshot from the Consumer Financial Protection Bureau's website, it's shown as ".25% of Loan Amount (Points)." For more detail, go to the CFPB website and click through all three pages of the sample Loan Estimate.

It's a good idea to apply with a few lenders and compare Loan Estimates line by line to see which is the best deal.

» MORE: Calculate your closing costs

Are Loan Estimates negotiable?

A Loan Estimate isn’t just a disclosure — it’s a valuable tool home shoppers can use to leverage competing lender offers and negotiate better terms.

Did you know...

Getting quotes from just two lenders could save you an average of $1,500 over your loan term, according to Freddie Mac data. Compare five lenders and you could save an average of $3,000 over the life of your loan.While not everything in the document is negotiable, reviewing Loan Estimates from at least three lenders can put you in a strong position to:

- Ask a lender to match or beat a competitor’s rate

- Negotiate certain lender fees

- Reduce your rate further by purchasing mortgage discount points (if it makes sense for your situation)

- Compare the cost of third-party services, like pest inspections and title searches

- Qualify for promotional discounts or rebates

- Explore options like a no-closing-cost mortgage if you’re short on upfront cash

As you gather Loan Estimates, aim to compare a mix of lender types, such as traditional banks, credit unions, non-bank lenders and mortgage brokers, to get a broader view of your options.

What you can (and can’t) negotiate on a Loan Estimate

A Loan Estimate includes a mix of fees, many of which are required to close your loan.

While you can’t avoid certain required costs, you may have the option to shop around. Homeowners insurance is an example of a cost that lenders require, but you get to select your preferred provider.

However, you’ll notice on the Loan Estimate that some costs are both required and non-negotiable, meaning you don’t get to shop around. Your lender selects these providers.

Here’s what you can and can’t negotiate prior to signing on the dotted line.

✅ Negotiable costs | ❌ Non-negotiable costs |

|---|---|

Mortgage rates | Appraisal fee |

Lender fees | Flood determination fee |

Home and pest inspector fees | Flood monitoring fee |

Homeowners insurance | Mortgage insurance |

Survey fees | Recording fees |

Title fees | Prepaid interest and escrow items |

Lender rebates/credits | Credit report fees |

Mortgage points | Property taxes |

See the final terms in the Closing Disclosure

Once you carefully review each of your Loan Estimates and choose a lender, you'll go through the entire mortgage underwriting process. Your lender will order an appraisal of the property and may request more documentation of your finances.

After final loan approval, you'll get the Closing Disclosure. This document gives the final terms and costs of your loan, including the specific amount you’ll need to pay at closing.

You’ll receive the Closing Disclosure at least three business days before your scheduled loan closing. Use this time to review the document for any changes, comparing your Closing Disclosure with the previously received Loan Estimate side by side. Call the lender if you have any questions.

Explore more on