People who ask whether it's possible to use one credit card to pay off another are usually seeking to do one of two things: manage their debt load by shifting credit card balances around, or collect more rewards by earning points or cash back on debt payments. The first is possible, but it will cost you in fees. The second is ... not going to happen.

First things first: You can't directly pay your credit card bill with another card. In other words, when your credit card statement arrives and shows that you owe $100, you can't simply put that $100 on a different credit card the same way you might use a card to make a purchase.

And while it's possible to pay a credit card indirectly with a cash advance — for example, by using a different credit card to get cash at an ATM — doing so would be extremely expensive and inefficient, making it a poor choice.

But there is a way to use one card to pay off another and potentially come out ahead: by performing a balance transfer, in which you move debt from one card to another. Rules and restrictions apply, though.

When transferring a balance: Yes

A balance transfer can save you money on interest by moving debt from a high-interest credit card to one with an introductory 0% APR offer. You can then pay down that debt more quickly because your entire payment can go toward reducing the principal balance.

Credit cards generally charge balance transfer fees of 3% to 5% of the amount transferred, so this option isn't free. Even so, if it would otherwise take you more than a few months to pay off your debt, you may well save money even with the fee. Balance transfers aren't instant, either; they can take weeks to go through. Also, they generally don't earn rewards.

For cards with long 0% intro APR periods for balance transfers and low transfer fees, see our best balance transfer credit cards.

How balance transfers work

While the exact process for balance transfers can vary widely, here are the steps you generally have to take when working with major issuers:

1. Apply for a card with an introductory 0% APR offer on balance transfers or use an offer on a card you already have. To qualify for the best offers, you generally have to have good or excellent credit (typically, FICO scores over 690). Something to keep in mind: Same-issuer transfers generally aren't allowed. For example, if you want to transfer a balance from a Chase card, you can't transfer it to another Chase card.

2. Initiate the balance transfer. If you're doing this online or by phone, you'll need to provide information about the debt you're looking to move, such as the issuer name, the amount of debt and the account information.

Sometimes, balance transfers can also be initiated using convenience checks, or the checks issuers send you in the mail. Before using one, though, read the terms to find out if it will count as a balance transfer and what your interest rate will be.

3. Wait for the transfer to go through. Once the balance transfer is approved, which could take two weeks or longer, the issuer will generally pay off your old account directly. That old balance — plus the balance transfer fee — will show up in your new account.

4. Pay down the balance. When that balance is added to the new card, you'll be responsible for making monthly payments on that account. And if you pay it down during the introductory 0% APR period, for example, you could save a bundle.

Popular balance transfer cards

Balance transfer details

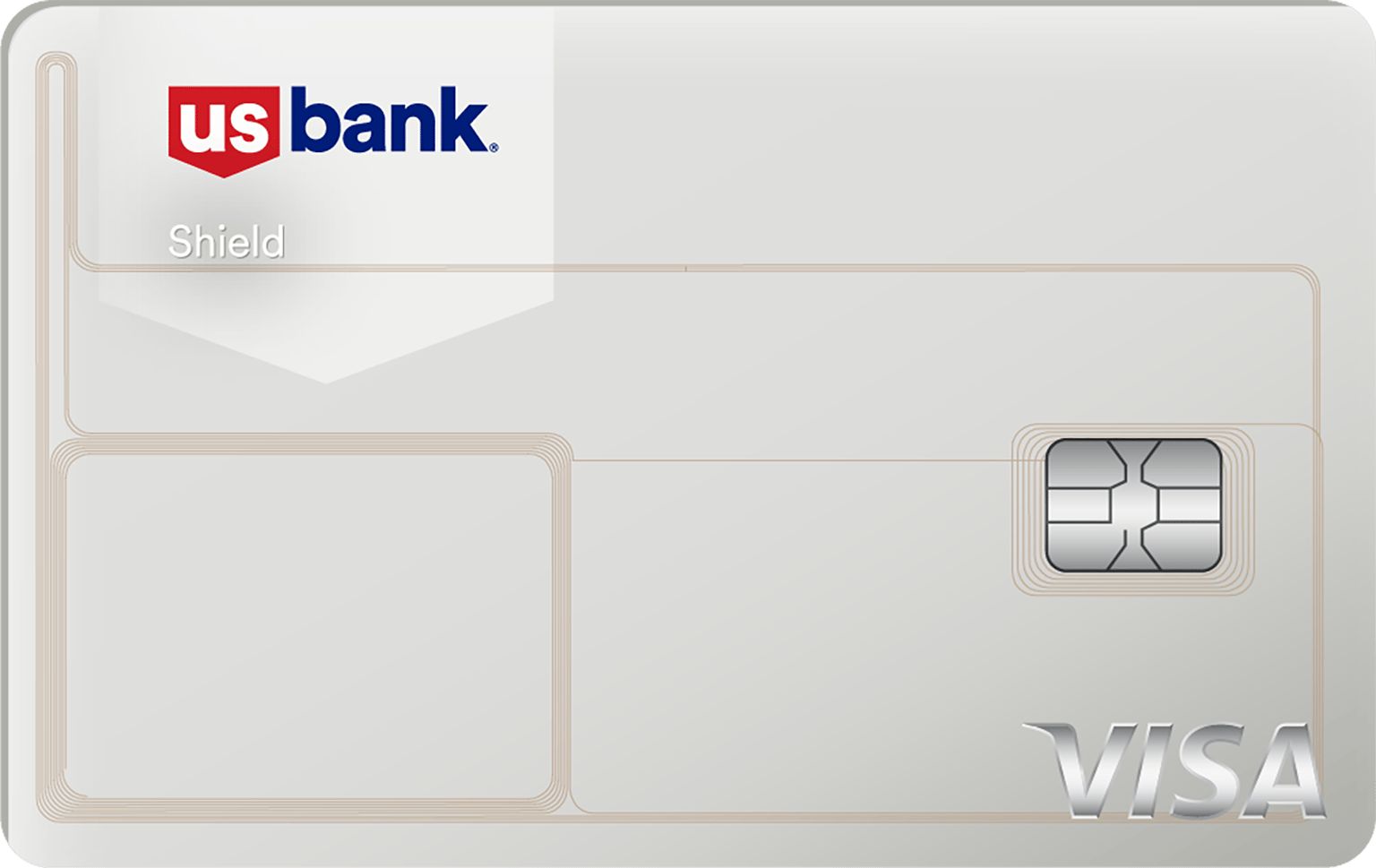

APR: 0% intro APR for 21 billing cycles on purchases and balance transfers, and then the ongoing APR of 16.99%-27.99% Variable APR

Balance transfer fee: Intro fee of 3% of the amount transferred ($5 minimum) within 60 days of account opening. After that, 5% ($5 minimum). This fee may be different if you apply directly via U.S. Bank.

APR: 0% intro APR for 21 months from account opening on purchases and qualifying balance transfers, and then the ongoing APR of 17.49%, 23.99%, or 28.24% Variable APR.

Balance transfer fee: 5% of the amount transferred ($5 minimum).

APR: 0% intro APR on Purchases for 6 months and 0% intro APR on Balance Transfers for 18 months, and then the ongoing APR of 17.49%-26.49% Variable APR.

Balance transfer fee: 3% intro balance transfer fee; up to 5% fee on future balance transfers (see terms).

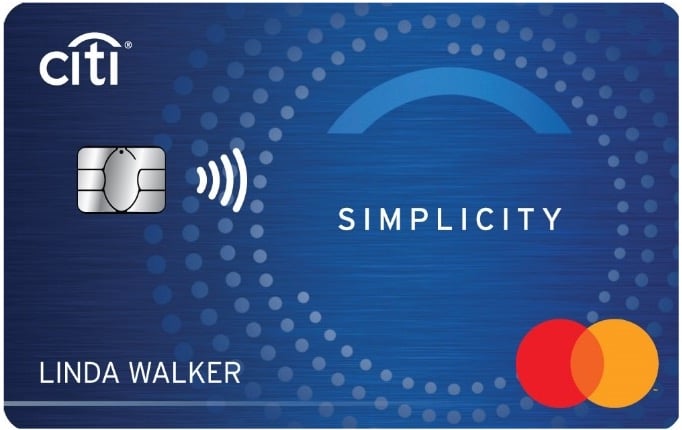

APR: 0% intro APR on purchases and balance transfers for 18 months, and then the ongoing APR of 17.49%-28.24% Variable APR.

Balance transfer fee: 3% intro fee (minimum $5) for transfers completed in the first four months. After that, 5% (minimum $5).

To pay your monthly bill directly: No

Paying a monthly credit card bill with a different card generally isn't an option. Don't expect to earn easy points and miles in a never-ending cycle or quickly buy yourself more time to pay off debt this way.

Credit card issuers usually require you to pay credit card bills with a bank account when you're making payments online or over the phone. You'll have to provide information like an account number and routing number — and you can't just substitute a credit card number instead.

In part, these restrictions exist because issuers want to limit their risk. A customer who pays one credit card with another may be more likely to default on payments.

With a cash advance: Yes, but it’s a bad idea

It's possible to use your credit card to get cash out of an ATM, then use that money to pay off another card. But such a transaction — a cash advance — typically comes with high fees and interest rates, making it an incredibly expensive way to get fast cash.

It's also not the way to go if raking in rewards is your goal. Cash advances generally don't earn rewards. And even if they did, the high fees and interest charges associated with them would eclipse the value of any benefits you might earn.

Can't pay your minimum? What to do

When money is tight, not having the option to pay one credit card with another might leave you with the lingering question of how to cover your minimum payment — especially when your credit card payments are taking a back seat to bad-things-will-happen-if-you-don't-pay-them bills, such as rent, car payments and child care.

If this is the case for you, here's where to start.

- Assess your situation. Review your credit card accounts and overall budget. Knowing the amounts owed, the interest rates and how much you can afford to pay each month can help you get a better idea of how serious your cash shortfall is and help you decide how to prioritize each bill.

- Communicate with your creditors. You may qualify for a credit card hardship program, which might lower your monthly payments and provide temporary relief. This could be a good way to go if your money trouble is temporary and you think you can pay down your balance with more time or adjusted terms.

- For chronic money trouble, consider other options. If you're constantly struggling to pay the minimums and feeling overwhelmed by debt — for example, if your debt (excluding a mortgage) is greater than 40% of your income and you see no way to pay it off within five years — bankruptcy might be your best option. Consider consulting with a bankruptcy attorney to review your situation.

Frequently Asked Questions

Can I pay my credit card bill with a different credit card?

It's virtually impossible to pay the monthly bill on a credit card simply by putting the cost on a different card. Card issuers typically require payment from a bank account — either a check sent by mail or an electronic payment directly from the account. You may be able to pay your credit card bill with a money order, but very few issuers of money orders accept credit cards as payment.

In most cases, the only way to move debt from one credit card to another is through a balance transfer.

Can I pay my credit card bill with a debit card?

To pay your credit card bill online, issuers typically require a direct transfer from your bank account. That means providing a bank routing number and an account number. Providing a debit card number is not an option.

Could I pay a credit card bill with a cash advance?

Paying a credit card bill with a cash advance from another card might be technically possible, but it would be expensive and leave you deeper in debt. To do it, you'd get the advance, then use the cash to buy a money order, which you'd then use to pay your bill. Or, if the bank that issued your credit card has a branch near you, you might be able to go in and pay the bill with cash at the teller window.

However, any debt you "pay off" with a cash advance would just be replaced with new debt for the advance itself, plus any cash advance fee your card charges (and nearly all cards charge them). Cash advances also incur interest, and the interest rate on advances may be even higher than the rate for purchases.