Key takeaways

- Business loan requirements generally include a personal credit score of 670+, $100,000+ in annual revenue and one to two years in business.

- You’ll need to provide tax returns, bank statements, financial statements and a business plan as part of your application.

- Lenders may also ask for collateral and/or a personal guarantee.

Finding and applying for a small-business loan can be time-consuming. By knowing lenders' typical business loan requirements ahead of time, you can streamline the process and avoid potential frustration.

Here are seven things lenders generally look at to decide whether you qualify for a loan.

How much do you need?

We'll start with a brief questionnaire to better understand the unique needs of your business. Once we uncover your personalized matches, our team will consult you on the process moving forward.

1. Personal and business credit scores

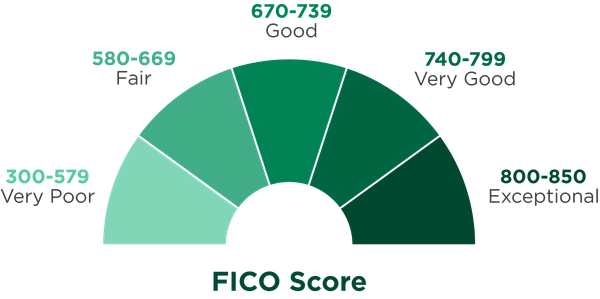

You’ll likely need good personal credit ( a FICO score of 670 or higher) or excellent business credit to qualify for a government-backed SBA loan or traditional bank small-business loan.

Online lenders, on the other hand, can be more lenient with credit scores, instead placing greater emphasis on your business’s cash flow and track record. Some online lenders and nonprofit organizations offer business loans for bad credit — for example, Expansion Capital Group accepts personal credit scores as low as 500.

Personal credit scores indicate your ability to repay personal debts, such as credit cards, car loans and mortgages. Small-business lenders require a personal credit check because they want to see how you manage debt.

FICO scores, commonly used in lending decisions, range from 300 to 850 (the higher, the better). You can get a free credit score on NerdWallet and a free copy of your credit reports at AnnualCreditReport.com.

Fast ways to build your personal credit include disputing any inaccuracies in your report and paying bills on time and in full.

More-established companies will have business credit scores with bureaus such as Experian, Equifax and Dun & Bradstreet. Ranges vary by bureau and scoring model — for example, Dun & Bradstreet’s PAYDEX and Experian’s business credit score both use a 1 to 100 scale.

Steps to building business credit include:

- Opening a business bank account.

- Using trade credit responsibly.

- Keeping public records (like court filings) clean.

🤓 Nerdy Tip

Twenty percent of applicants approved through NerdWallet Small Business reported credit scores of 659 or below.

Want to see if you qualify? Fill out our simple application here.

2. Annual revenue

Many lenders will only consider businesses that bring in at least a minimum monthly or annual revenue. Lenders look at your revenue to make sure that you have enough cash flow to afford your loan.

How much cash flow you’ll need depends on the individual lender — for example, online lender OnDeck requires $100,000 in annual revenue to qualify for its line of credit, while Bank of America’s minimum is $250,000 for its secured business loans.

If you don’t meet lender requirements for a business loan with low revenue, you’ll likely have to rely on alternative financing options, like invoice factoring.

Debt service coverage ratio

Your lender may also look at your debt service coverage ratio, or DSCR. In basic terms, it compares what you earn to what you owe. To find it, you divide your annual operating income by your total annual debt payments.

For example, if your annual income is $150,000 and your total debt payments are $100,000, your debt service coverage ratio would be 1.5.

Most lenders want to see a ratio of at least 1.25 — meaning your income comfortably covers your debts.

3. Years in business

Lenders use your time in business as a quick measure of success. The longer you’ve been operating, the more likely you are to have money to repay your debts.

To qualify for a business loan from a bank, you’ll typically need at least two years in business. Similarly, many SBA lenders require you to have at least two years in business. Online business loans tend to have less stringent requirements but still usually require at least six months in business.

➡️ Are you a new business looking for funding?

Check out our list of the best startup business loans. Businesses with three months or more in operation may be able to qualify.

4. Business industry and size

Every industry has a different risk level — and some industries, like restaurants and beauty services, can be considered high risk because they’re more likely to have inconsistent revenue.

There are also certain industries that many lenders don’t work with at all. These typically include adult entertainment, drug dispensaries or products, gambling and money service businesses.

Industry matters more than you may expect. According to NerdWallet’s 2026 Business Loan Study, general contractors, health services businesses and restaurants, cafes and bars received the largest share of approved loans — showing that even “high risk” categories like food service can and do get funded when the rest of the application is strong.

Government-backed loans from the U.S. Small Business Administration have specific size and industry criteria, among other unique requirements. If you want to qualify for SBA loans, you’ll need:

SBA loan requirements

- Your business must meet the SBA's definition of a "small" business, which varies by industry.

- You must be a for-profit company.

- You can’t operate in an ineligible industry, like real estate investing, gambling or political lobbying activities.

- You must be current on all government loans with no past defaults. For example, being more than 90 days late on a federal student loan or government-backed mortgage could disqualify you.

U.S. Small Business AdministrationSBA 7(a) loan

Max Loan Amount

$5,000,0005. Business plan and loan proposal

Lenders want to see that you’ll use the money wisely — and that you can repay it. You may need to submit:

- A business plan that explains your goals and how you’ll reach them.

- A loan proposal outlining how much money you’re requesting, what you’ll use it for and how you plan to repay it.

These documents should clearly demonstrate that you will have enough cash flow to cover ongoing business expenses and the new loan payments. While a business plan describes your company’s broader vision and strategy, a loan proposal is specific to the financing request itself. This is the document a lender will scrutinize most closely to decide whether to approve your loan.

On the other hand, if you’re a new business that doesn’t have existing revenue to show a lender, a thorough business plan can help convince it that you will be successful in the future.

Use NerdWallet’s business loan calculator to estimate your monthly loan payments:

Estimate payments to understand the cost of a business loan

Over the course of the loan, expect to pay

$0.00/mo

Payment breakdown

Total principal

$0.00

Total interest

$0.00

Total principal & interest

$0.00

| Payment date | Principal | Interest | Balance |

|---|---|---|---|

| Today | $0 | $0 | $0.00 |

6. Collateral or personal guarantee

Many lenders require collateral or a personal guarantee to secure a small-business loan.

- Collateral is an asset, such as equipment, real estate or inventory, that can be seized and sold by the lender if you don’t repay your loan.

- A personal guarantee means you’re responsible for repaying the debt if your business can’t. For example, if your business defaults on a $100,000 loan backed by a personal guarantee, the lender can pursue your personal assets — such as your home, car or savings — to recover the unpaid balance.

SBA 7(a) loans above $50,000 typically require collateral plus a personal guarantee from every owner of 20% or more of the business.

Some lenders offer unsecured business loans, which don’t require physical collateral. However, they may still:

- Require a personal guarantee, or

- Take out a blanket lien on your business assets, which gives them the right to take business assets (real estate, inventory, equipment) to recoup an unpaid loan.

Each lender has its own rules, so ask questions if you're unsure about the loan requirements.

7. Business and financial documents

Banks and other traditional lenders typically require extensive documentation. You may need to provide:

- Personal and business income tax returns.

- Financial documents, such as profit and loss statements, balance sheets and cash flow statements.

- Personal and business bank statements.

- A photo of your driver’s license.

- Commercial leases.

- Business licenses.

- Articles of incorporation.

- Proof of collateral.

- Business plan.

- Existing debt schedule, if applicable.

- Legal contracts and agreements.

- A resume that shows relevant management or business experience.

- Financial projections if you have a limited operating history.

Online lenders may provide a streamlined application process with minimal documents and faster underwriting.

What to do if you don’t qualify for a business loan

If you fall short of a lender’s requirements, you still have options:

- Request a smaller loan amount. Borrowing less lowers the lender’s risk and may improve your approval odds.

- Build your credit before reapplying. Even just a few months of on-time payments can strengthen your credit profile and make your application more attractive to lenders.

- Consider alternative financing. Depending on why you can’t qualify, other options may be worth exploring: microloans if your credit or time in business is limited, business credit cards if you need smaller ongoing access to funds or grants if you’d rather avoid debt altogether.

- Establish a lender relationship early. If you’re just starting out, opening a business bank account or credit card now can help you when you apply later.

- Seek out expert advice. Your local Small Business Development Center and organizations like SCORE can provide financing advice and help you prepare future applications.

Frequently asked questions

How do you qualify for a business loan?

Although business loan requirements vary from lender to lender, you’ll generally need good credit, strong finances and an established business history to qualify for a loan. Traditional lenders typically have the strictest requirements, whereas online lenders have relatively easy business loans to qualify for.

What do banks require for a small-business loan?

Banks generally require that you have good to excellent credit (score of 670 or higher), strong finances and at least two years in business to qualify for a loan. They’ll likely require collateral and a personal guarantee as well.

You’ll typically need to provide detailed paperwork as part of your application — and some banks will require you to apply in person.

What are the documents required for a business loan?

Each lender will have unique documentation requirements, but at the very least, you’ll likely need to provide:

- Business and personal bank statements.

- Business and personal tax returns.

- Financial statements, like balance sheets and income statements.

Traditional lenders typically require more paperwork than online lenders.

What disqualifies you from getting a business loan?

Common reasons for a business loan denial include:

- Too much existing debt.

- Poor credit history.

- Insufficient collateral.

- Not enough time in business.

- Weak cash flow or revenue.

- History of defaults or bankruptcy.

Article sources

NerdWallet writers are subject matter authorities who use primary, trustworthy sources to inform their work, including peer-reviewed studies, government websites, academic research and interviews with industry experts. All content is fact-checked for accuracy, timeliness and relevance. You can learn more about NerdWallet's high standards for journalism by reading our editorial guidelines.

- 1.NerdWallet. 2026 NerdWallet Business Loan Study.

- 2.Chase for Business. Is your business financially fit? Your debt-service coverage ratio can tell you. Accessed Jul 17, 2026.

- 3.U.S. Small Business Administration. SOP 50 10 Lender and Development Company Loan Programs. Accessed Jul 17, 2026.