There’s no bulletproof way to identify an investment bubble before it happens, or even while it’s happening. We can only pinpoint bubbles in hindsight, after they’ve already burst — and lost a lot of investors a lot of money.

But when people look back on bubbles of the past, like the dot-com bubble of the late 1990s or the housing bubble of the mid 2000s, many recall a vague feeling that something was off.

It’s no secret that many experts have that feeling right now about the current AI boom. Even OpenAI CEO Sam Altman, the head of the world’s most prominent AI lab, has sounded the alarm. “Are we in a phase where investors as a whole are overexcited about AI? My opinion is yes,” Altman said in an August interview with The Verge.

Should you make investment decisions based on those kinds of feelings and opinions?

I don’t know. I’m just a guy who writes personal finance articles. I don’t have any groundbreaking insights that conclusively prove that we are or aren’t in an AI bubble.

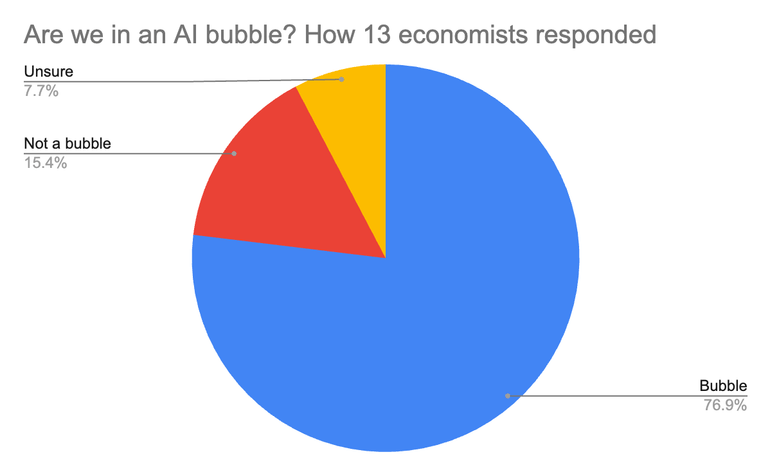

But I did ask financial economists at more than a dozen universities across the United States about it, and their responses were striking: More than 75% of economists we spoke to think the current AI investment boom is, in fact, a bubble.

Most of these economists, who hold positions at prominent universities, gave their answers on condition of anonymity, given the sensitive nature of the topic, but they cited a variety of evidence for their positions. Below, we’re breaking down the arguments for and against the theory that we’re in an AI bubble — and discussing how you can protect yourself if that theory turns out to be true.

Brokerage firms | |

|---|---|

The case against the bubble theory

I’ll start by looking at the “not a bubble” and “maybe a bubble” responses. These were far fewer in number than the “yes” responses from economists, but they brought up an important point: There is real money in AI, and several of the biggest tech stocks are proving that with their earnings and revenue.

In its most recent quarterly earnings report, Nvidia (NVDA) reported a record $57 billion in revenue and $1.30 in earnings per share, giving it a price-to-earnings ratio (PE ratio) in the mid-40s range. Microsoft (MSFT) reported $77.7 billion in revenue and $3.72 in earnings per share in its most recent quarterly report, giving it a PE ratio in the mid-30s. Alphabet (GOOG) reported $102.3 billion in quarterly revenue and earnings per share of $2.87, giving it a PE ratio in the low 30s.

These PE ratios are a little high — a “normal” PE ratio is typically somewhere in the 20s — but they’re not outrageous. All three stocks have actually seen decreases in PE ratio in recent years. Plus, there are plenty of non-AI stocks in much worse shape in terms of PE ratio. For example, CVS Health Corp. (CVS) has a PE ratio over 200.

There are questions about many of the other big AI stocks. Tesla (TSLA) has a PE ratio over 300, and Palantir Technologies (PLTR) has a PE ratio over 400, for example. And there are also questions about whether Microsoft, Nvidia, Alphabet et al would still be able to rake in tens of billions of dollars in AI revenue in the event of a broad downturn in AI investment.

But for the time being, it’s actually kind of hard to make an argument that the multi-trillion-dollar AI behemoths like Nvidia, Microsoft and Alphabet are severely overvalued. They have the earnings to back up their stock prices, to some extent.

The case for the bubble theory

That said, 10 out of 13 economists surveyed by NerdWallet did ultimately say that we’re in a bubble. Here are some of the arguments they made for that position:

- Valuations are on the high end. The PE ratios of the biggest tech stocks, like Alphabet, Microsoft and Nvidia, might not be obscene, but they’re a little higher than what most would consider a typical PE ratio, and many other AI stocks have triple-digit PE ratios.

- Venture capital investment in AI startups is growing at a wild rate. It’s worth remembering that the stock market is not the only type of equity investment. Many economists noted that venture capitalists are throwing ever-growing amounts of seed money into just about any startup that claims to incorporate AI into its business model, and expressed doubts that that investment growth rate is sustainable or that it’ll produce real returns. Venture capital investments in AI companies surged 62% last year, according to Crunchbase.

- There are worries about “circular financing” between big AI companies. In recent years, a number of Big Tech firms have signed AI investment and hardware purchasing deals worth tens of billions of dollars… with each other. This raises the question of whether all of the AI revenue reported by the likes of Microsoft, Nvidia and Alphabet is organic, or whether much of it consists of money from other tech companies that have recently gotten flush with investment due to AI hype themselves.

- AI may have real value, but that doesn’t rule out a dot-com bubble scenario. Many of the “yes” responses did not doubt that AI as a technology has huge potential, but they cautioned that this doesn’t disprove the theory that we’re in a bubble — and that this line of anti-bubble argument is suspicious in and of itself. Some drew comparisons to the dot-com bubble of the 1990s and early 2000s: Back then, investors correctly recognized the transformative economic potential of the nascent internet, but they still got carried away with their investments in internet stocks, eventually leading to a big correction.

What you can do about it

If you’re a longtime reader of The Nerdy Investor, or of NerdWallet in general, you probably have an idea of what we’re going to say here. When we write about a potential downside risk in the market, we often come back to the refrain that investment diversification is the best defense, and that index funds and ETFs are the easiest way for most investors to ensure they’re well-diversified.

Yeah, you could try to actively bet against potentially-overvalued AI companies by buying put options on them, short-selling them, or buying inverse ETFs that contain them, but these are risky moves that lose most people money.

Here’s the thing, though… If we are in an AI bubble, this may be one situation where many popular index funds aren’t that safe, either.

Back in August, I wrote about how Nvidia made up about 8% of the entire S&P 500 index (around 7% today) by market capitalization, and how the seven largest S&P 500 stocks, which are all tech companies with substantial AI interests, make up about a third of the index. The situation is even more dire for the Nasdaq 100, where Nvidia makes up more than 13% of the index, and the top 7 stocks (all AI-related tech names) make up well over half of it.

However, there are still ways to diversify through other types of index funds, if you think outside the box a little bit. Here are a few ideas:

- The Dow Jones Industrial Average is one index that is tracked by several ETFs and mutual funds, and it isn’t disproportionately made up of Nvidia and other tech stocks, because it’s a stock price-weighted index rather than a market cap-weighted index. Nvidia makes up less than 2.5% of the Dow, and Big Tech in general accounts for less than 25% of it. (Check out our article on Dow Jones ETFs for more information).

- The Russell 2000, an index of small-cap stocks tracked by many ETFs and mutual funds, is even less tech-y than the Dow. Tech accounts for less than 14% of it; it mostly consists of companies in the industrial, health care and financial sectors. One caveat: Small-cap stocks can be volatile. Although the Russell 2000 has limited exposure to AI and tech, it may still swoon in an AI bubble-burst scenario if investors are spooked into selling risky stocks in general. (NerdWallet maintains a list of the best-performing small-cap ETFs).

- Equal-weight S&P 500 ETFs are one way to get exposure to the S&P 500 companies while solving the Nvidia/Big Tech concentration problem. As we wrote in this newsletter issue a few weeks ago, they’re less AI-exposed than regular market cap-weight S&P 500 funds, and often pay higher dividend yields, but they tend to have significantly higher fees as well, and have trailed normal S&P 500 ETFs in returns this year.

- International ETFs could also be worth a look. The Vanguard FTSE All-World Ex-US ETF (VEU), for example, is less than 14% tech stocks by market cap. (See our page on international ETFs to learn more).

» MORE: Best brokers for ETFs