We believe everyone should be able to make financial decisions with confidence. While we don't cover every company or financial product on the market, we work hard to share a wide range of offers and objective editorial perspectives.

So how do we make money? Our partners compensate us for advertisements that appear on our site. This compensation helps us provide tools and services - like free credit score access and monitoring. With the exception of mortgage, home equity and other home-lending products or services, partner compensation is one of several factors that may affect which products we highlight and where they appear on our site. Other factors include your credit profile, product availability and proprietary website methodologies.

However, these factors do not influence our editors' opinions or ratings, which are based on independent research and analysis. Our partners cannot pay us to guarantee favorable reviews. Here is a list of our partners.

Mortgage Origination Fee: How To Compare Lender Charges

Compare fees and mortgage rates among lenders to find the best deal.

Robin Rothstein is a NerdWallet writer specializing in housing market trends and home lending topics. She has been writing about residential real estate since 2021. Before joining NerdWallet, Robin was a senior writer at Forbes Advisor producing high-performing content on mortgages, loans, and personal finance topics. Robin is also an Off-Broadway-produced and published playwright. As a longtime homeowner, she follows local land-use issues, which inspired her to write the short play, “Grassroots,” about a cherished local bar forced to close due to high rents. “Grassroots” is included in The Best Ten-Minute Plays 2021, published by Smith and Kraus. Robin is based in New York City.

Barbara Marquand is a former NerdWallet writer covering mortgages, homebuying and homeownership, insurance and investing. Previously, she covered personal finance for QuinStreet and wrote for national consumer and trade publications on topics including business, careers and parenting. Her work has appeared in MarketWatch, MSN Money, The New York Times and The Washington Post.

Chris Jennings is a NerdWallet editor specializing in home lending topics. He has been writing and editing about mortgages and personal finance since 2016. He enjoys simplifying complex mortgage topics for first-time homebuyers and homeowners alike. Before joining NerdWallet, he wrote and edited content for a number of respected finance brands, including Bankrate, Forbes Advisor, and GOBankingRates.

Born and raised in the Chicago suburbs, Chris earned a bachelor's degree in English from Illinois State University. Chris now calls Los Angeles home, where he lives with his wife, daughter, and their dog.

Updated

How is this page expert verified?

NerdWallet's content is fact-checked for accuracy, timeliness and relevance. It undergoes a thorough review process involving writers and editors to ensure the information is as clear and complete as possible.

A mortgage origination fee is an upfront fee a lender charges for processing a loan. The fee is part of the closing costs you pay when the mortgage is finalized.

Like mortgage rates, origination fees vary among lenders, so it pays to shop around. Mortgage origination fees tend to range between 0.5% to 1% of your loan amount. On a $350,000 mortgage, that would be between $1,750 and $3,500.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

N/A

No score credit options are available.

Min. down payment

0%

Provides DPA assistance for no down payment options.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

580

580

Min. down payment

3.5%

First-time home buyers may qualify for 3% down mortgages at Rocket.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

0%

On VA loans, NBKC offers down payments as low as 0%.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

N/A

No score credit options are available.

Min. down payment

0%

Provides DPA assistance for no down payment options.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

3%

Rocket Mortgage offers conventional mortgages with as little as 1% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

580

580

Min. down payment

3%

New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

720

720

Min. down payment

N/A

NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

3%

NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

N/A

No score credit options are available.

Min. down payment

0%

Provides DPA assistance for no down payment options.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

580

580

Min. down payment

3.5%

First-time home buyers may qualify for 3% down mortgages at Rocket.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

0%

Veterans United offers VA loans for as little as 0% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

0%

On VA loans, NBKC offers down payments as low as 0%.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

N/A

No score credit options are available.

Min. down payment

0%

Provides DPA assistance for no down payment options.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

580

580

Min. down payment

3%

Rate offers conventional loans with as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

3%

Rocket Mortgage offers conventional mortgages with as little as 1% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

620

620

Min. down payment

3%

NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

580

580

Min. down payment

3%

New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

580

580

Min. down payment

3%

AmeriSave offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

600

Min. down payment

N/A

New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

600

Min. down payment

N/A

New American Funding works with down payment assistance programs in 14 states, including California, Texas, Florida and Illinois.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

Min. credit score

720

720

Min. down payment

N/A

NBKC offers conventional loans for as little as 3% down.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

You can see how much a lender will charge by checking the Loan Estimate, an official document that spells out the terms and projected costs of the mortgage. The lender must provide a Loan Estimate within three business days after you apply.

The lender fees are detailed on the left side of Page 2 under "A. Origination Charges." Sometimes instead of charging a single origination fee, lenders will divide the fee into fee categories, such as:

Application fee

Processing fee

Underwriting fee

Verification fee

When itemized, each fee may look inconsequential, especially compared to the size of your loan — but don't let that confuse you. Be sure to check the total amount of origination charges when comparing fees among lenders.

Lenders make money by charging interest and fees. Sometimes they charge higher fees to lower their advertised rates, or they might advertise low — or no —fees but charge more interest.

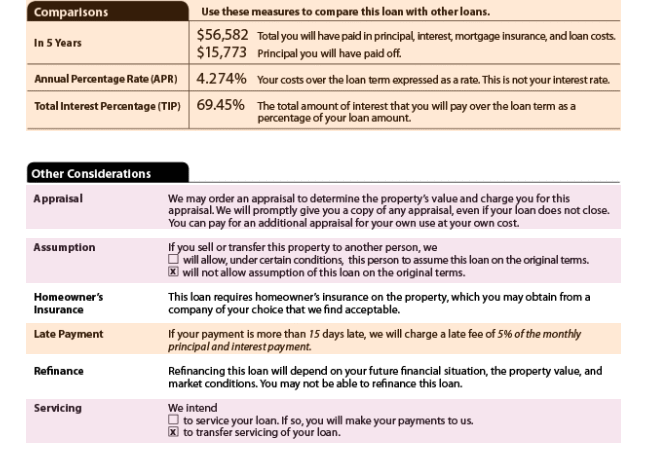

To get a true look at the cost of borrowing, check the mortgage offer's Annual Percentage Rate, or APR. The APR, which is listed on Page 3 of the Loan Estimate, includes the interest rate, origination fees and discount points and provides an apples-to-apples way to compare lenders.

Page 3 of a sample Loan Estimate on the Consumer Financial Protection Bureau's website

Did you know...

Mortgage points, also known as discount points, are optional fees you pay upfront to reduce the interest rate.

Frequently Asked Questions

Can you negotiate mortgage origination fees?Can you negotiate mortgage origination fees?

You can always ask a lender to reduce or waive some of the origination charges, but lenders may not budge. The best way to get a good deal is to apply with more than one mortgage lender, compare Loan Estimates and choose the lowest-cost offer.

Can you avoid paying mortgage origination fees altogether?Can you avoid paying mortgage origination fees altogether?

Yes, one option is to accept a higher interest rate in exchange for the lender waiving the fee. While this typically means you’ll end up paying more in interest over the life of the loan, it can still work in your favor if you plan to refinance within a few years — especially if the added interest costs are lower than the origination fee.

Another possibility is to negotiate the fee as a seller’s concession. For instance, if it’s a buyer’s market, the seller is in a hurry, or the home has been listed a while and gone unsold, the seller may agree to cover this cost to move the deal over the finish line.