Why trust NerdWallet

Why trust NerdWallet

250+ small-business products reviewed and rated by our team of experts.

80+ years of combined experience covering small-business and personal finance.

Objective, comprehensive small-business insurance ratings based on the financial strength, complaint records, digital features and customer service availability of insurance market leaders. Read our methodology.

NerdWallet's small-business insurance content — including our ratings, reviews and recommendations — is produced by a team of writers and editors who specialize in small-business finances. Their journalism has appeared in The Associated Press, Washington Post, MarketWatch, Nasdaq, Entrepreneur, ABC News, MSN and other national and local media outlets. Each writer and editor follows NerdWallet's strict editorial guidelines to ensure fairness and accuracy in our coverage.

Thimble is an online insurance agent that sells coverage by the month, day or hour to people who need business insurance fast. It’s a convenient option if you need to show proof of insurance to someone ASAP.

It’s also useful to business owners who hire contractors. You can use Thimble’s “Certificate Manager” to spell out insurance requirements for the people you’re hiring, and they can buy compliant policies through Thimble.

The downsides: Thimble charges fees alongside its premiums, and Thimble customer support is also only available online. It sells a limited range of policies, too. Consider alternatives if you want to be able to ask questions about your coverage or customize your policies.

Other insurance companies underwrite Thimble’s policies, not Thimble itself. That means Thimble doesn’t receive credit ratings about its financial strength. State regulators don’t collect complaints about it either. For those reasons, we don’t give Thimble a star rating.

Save up to 30% on business insurance

NerdWallet Business Insurance helps you get real-time quotes from 30+ insurers, and instant access to your Certificate of Insurance (COI).

Thimble insurance: Pros and cons

Pros

Can get a quote and buy coverage online in minutes.

Coverage available by the job or the month.

Contractors and the people managing them can use the Certificate Manager to verify that insurance is contractually compliant, or to purchase coverage that is contractually compliant.

Cons

Customer support is only available online.

May charge extra fees when you buy coverage.

Thimble does not sell commercial auto insurance.

What Thimble does well

Flexible, temporary insurance policies

Thimble offers insurance packages for all kinds of entertainers and event-based service providers, from wedding planners to DJs to Santas. Coverage can start the same day you buy it. And while getting a quote, you can automatically add your venue as an additional insured. If you need coverage immediately for compliance reasons, Thimble can probably get it for you.

Certificate Manager tool for contractors

Thimble’s Certificate of Insurance Manager is a free portal where you can send your insurance requirements to your contractors and ask them to upload certificates of insurance verifying their compliance. If contractors don’t already have compliant policies, Thimble will recommend them. This includes policies designed for vendors and sold by the hour and the day.

Where Thimble falls short

No phone support

There isn’t a phone number you can call to talk to someone at Thimble. All customer support is via chat or email.

If you have to file a claim, you’ll at least start the process online with Thimble. The company that underwrites your policy will take your claim from there. A third party, American Claims Management Inc., also handles some claims.

Buying a policy through an agent takes longer than buying one online. But afterward, you’ll have your agent available as a resource when you have questions or claims. Our top-rated company that sells through independent agents is Cincinnati Insurance.

Limited policies for sale

Thimble sells the most insurance policies most companies need, like general liability insurance and commercial property insurance. But you can’t get more specialized types of business insurance, like commercial auto coverage.

If your business has any specialized risks — like selling a physical product or offering financial advice — work with an agent. They can help you get complete coverage for all your operations.

How we evaluated Thimble

Thimble is an insurance producer, which means it doesn’t insure its customers directly. Instead, it sells policies from other insurance companies. For that reason, we don’t currently give Thimble its own star rating.

That said, here’s what I looked at to write this review.

Who underwrites Thimble policies?

Here’s who underwrites Thimble’s policies and how they stack up on our most important considerations:

Markel Insurance Company, which underwrites general liability policies:

- Fewer complaints than we’d expect about commercial property and general liability insurance given the company’s market share.

- “Excellent” financial strength ratings from AM Best.

National Specialty Insurance Company, which underwrites general liability policies:

- No data about customer complaints. But NSIC is a subsidiary of Markel, which had excellent complaint ratios.

- “Excellent” financial strength ratings from AM Best.

Employers Holding Group, which underwrites workers’ comp policies:

- Far more complaints than expected about workers’ comp.

- “Excellent” financial strength ratings from AM Best.

Thimble customer experience

I took two additional steps to understand Thimble users’ experiences:

- Aggregating customer reviews and complaints. I used an AI tool to summarize what policyholders say about Thimble on websites like Reddit, the Better Business Bureau and app stores. This helped me understand what real-world users of a particular company think about it.

- Trying the online quote process. If an insurer offers online quotes, I get one. I use the same location, industry and business size information every time. The quote process can reveal how customizable policies are, hidden fees and more.

Save up to 30% on business insurance

NerdWallet Business Insurance helps you get real-time quotes from 30+ insurers, and instant access to your Certificate of Insurance (COI).

What small-business owners think about Thimble

These themes emerged in online discussion about Thimble. I used an AI tool to help analyze overall sentiment in places like Reddit, TrustPilot and the Better Business Bureau, then chose to highlight the topics I think matter most.

👍 Temporary, easy-to-buy coverage

Thimble’s biggest value prop: You can get coverage in a few minutes that starts today. Reddit users in construction, event photography and film say getting a policy is easy. Thimble does tack on fees (more on that next). But if you only do occasional events, the company makes it simple.

👎 Confusing additional fees

Thimble’s policies are cheap on the surface. But users say fees emerge when you’re checking out, like a “down payment fee” and “checkout fee.”

From going through the quote process, I can confirm some costs don’t show up until the very end. They aren't all extra fees — the “down payment” is two months of your premium, for instance. Still, if you’re in a pinch and need coverage the same day, it’s hard to walk away instead of accepting that fee. I see why users feel frustrated.

Ergo Next, another online insurance company, charges a similar “service fee.” But most insurers don’t charge anything other than the premium.

👍 Easy to get and manage certificates of insurance

Online commenters say Thimble makes it easy to download your COI, add additional insureds and share it with others.

Other online business insurance companies offer quick access to your COI. But most companies still require you to email customer support or call your agent in order to add an additional insured. If you need to provide proof of coverage ASAP, Thimble is a good bet.

👎 Customer support is lacking

Thimble doesn’t offer phone support at all. That can make it hard to get answers about what you bought, what it covers and how much it cost. Commenters report waiting days for email responses. And since Thimble doesn’t manage its own claims, your mileage may vary in terms of how helpful that support is. After all, Thimble won’t be involved in that process at all.

What policies does Thimble sell?

You can buy these policies using Thimble:

- Inland marine insurance, which Thimble calls “business equipment protection."

- Cyber insurance (not available in California, Florida or New York).

- Event insurance (not available in New York, North Carolina or Texas). This includes event liability or liquor liability coverage.

These are some of the most common types of business insurance. Policies are very standard. But some companies face specific risks that require more customization. If you provide legal or financial advice, sell a physical product or need liquor liability insurance on an ongoing basis, you should shop elsewhere.

How to get insurance from Thimble

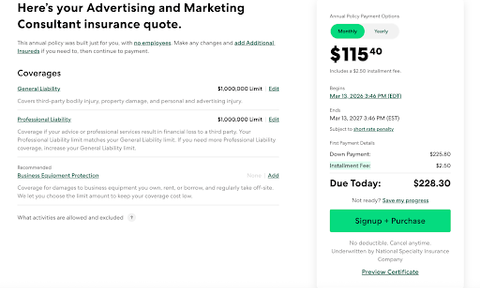

It only took me a few minutes to get a quote from Thimble. I told the company I was a freelance marketing consultant working out of my home and that I earned around $10,000 in annual revenue.

Thimble’s quote process asked for:

- My ZIP code.

- Whether I need business insurance (ongoing policies) or event insurance (a policy covering a specific event).

- What type of work I do.

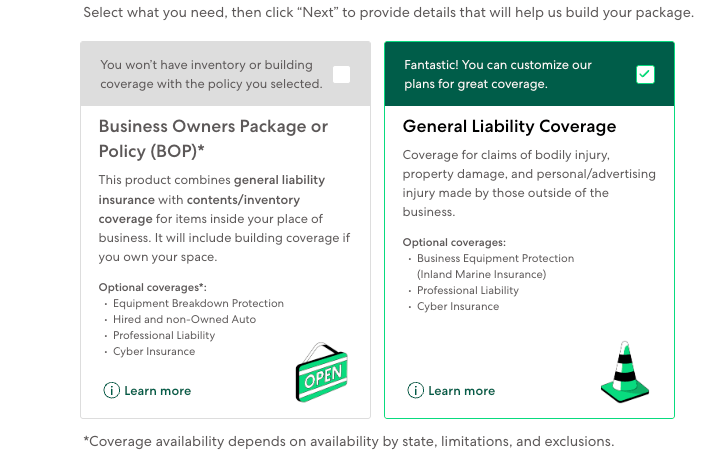

Thimble asked me to choose between a BOP and general liability insurance. I chose general liability coverage.

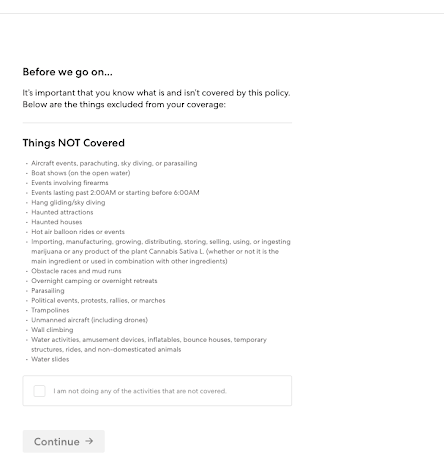

I had to attest that I do not work as an investment advisor or financial planner, work without a license, give legal or medical advice, work with wild animals or use “water activities, amusement devices, inflatables, bounce houses, temporary structures and rides.” Maybe that’s included in event insurance.

After that, I chose between a short-term policy and an ongoing one. Thimble asked for my number of employees, annual payroll and annual revenue.

I claimed $10,000 in revenue. Thimble double-checked that number because it was unlike “customers similar to you.”

I told Thimble I want coverage to start today. That was it! I got my quote.

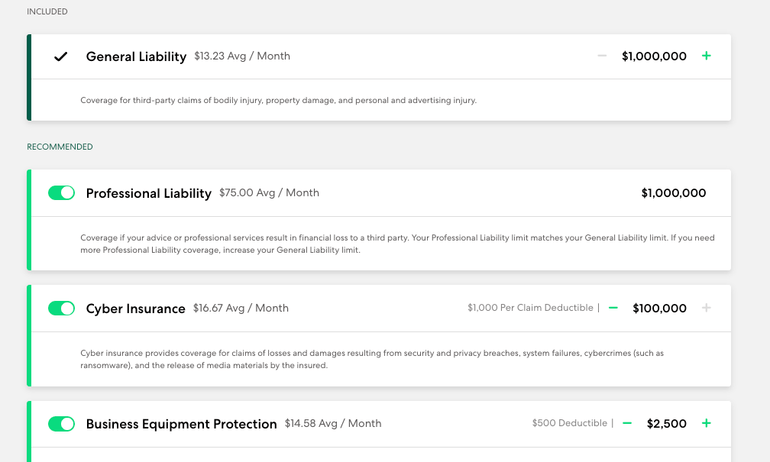

My premium updated in real time as I toggled the recommended coverages on and off. I could adjust limits for general liability insurance, cyber insurance and business equipment protection, but not for professional liability insurance. I could not adjust my deductible. This is less flexibility than most online insurance flows offer — normally you can adjust both limits and deductibles.

I selected my coverages. I had the option to pay monthly or annually, but there was no savings for paying for the year upfront. My editor got an “installment fee” charge when he went through the flow and selected “monthly." A Thimble spokesperson said these fees vary by ZIP code.

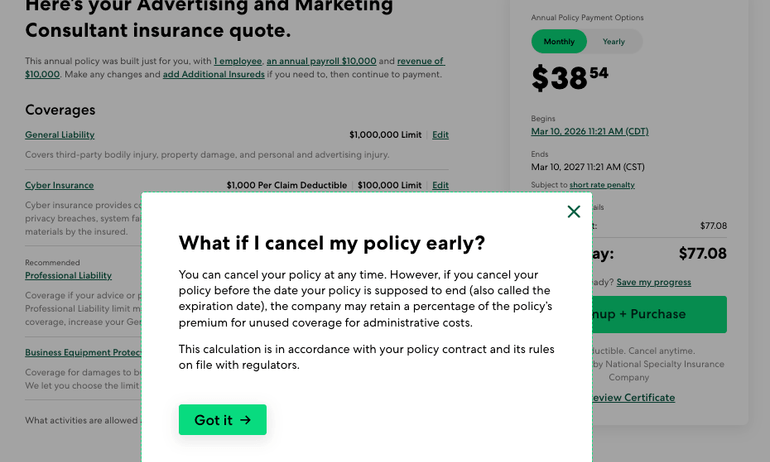

Thimble says you can cancel your policy anytime. That’s true for every insurance company. But Thimble hedges a bit about how much money you’ll get back. They may “retain a percentage of your premium” to cover administrative costs. Thimble does not say how much that could be.

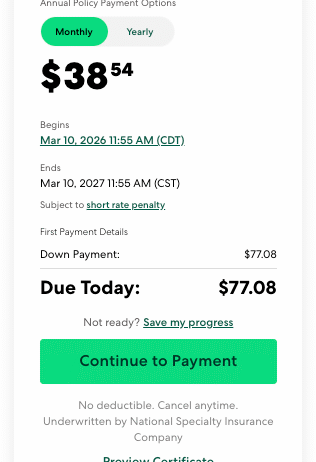

Note, too, that Thimble asks for a “down payment” that’s twice the cost of my monthly premium. Thimble's help center explains that this is two of 12 monthly payments, but it's not immediately clear.

My editor and I didn't initially see the $100 checkout fee that some users have talked about online. We reached out to Thimble for clarification, and a spokesperson said Thimble does charge a fixed transaction fee in some states. They declined to specify how much that was. But we also saw $100 after getting quotes for outside our home states of Illinois and New York — in quotes for Florida and Wisconsin, for instance.

Fees like this are relatively rare. Some online insurance companies charge them. But most only ask you to pay your premium. Many companies offer a discount if you pay your annual premium in full up front, rather than a fee if you don't.

It's certainly possible that it all balances out. Your premiums might be a little higher with companies that don't tack on additional fees, because those premiums still have to cover the company's administrative costs. But these fees also mean Thimble's sticker price on the day you buy might be higher than you expect.

We always recommend getting multiple quotes so you can compare actual monthly or annual costs.

How to get event insurance from Thimble

I’ve long been curious about Thimble’s short-term policies. So I went back to the start of the quote process. This time, I told Thimble I needed insurance for a fundraising event (“business party”).

Once again, I had to stipulate that I understood the policy exclusions. (No haunted houses, folks.)

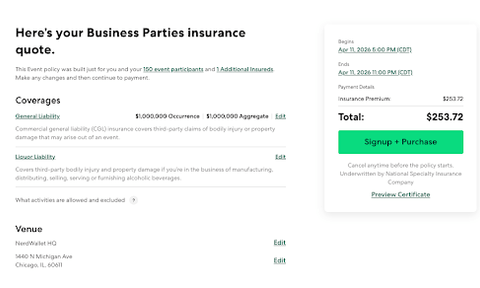

Next, Thimble wanted details about the venue — a private home, rented commercial venue, rented private residence like an Airbnb, or a public space. I gave a venue name, and Thimble added it as an additional insured automatically.

Thimble asked if the event was mostly indoors, outdoors or a mix and whether there would be swimming or water activities available. I assume that’s because swimming introduces significant liability risks.

Finally, I gave the date and time of the event and the number of guests. The quote updated in real time as I changed the size of the party.

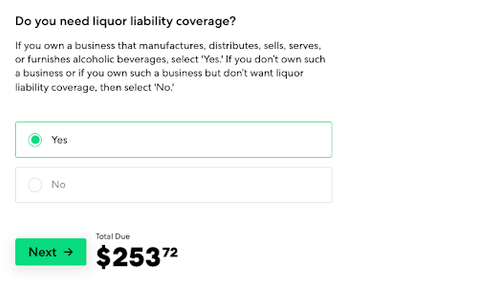

Adding liquor liability coverage increased my quote by about $150.

Thimble asked me to verify that everyone serving alcohol had attended a certification course, would check ID and would adhere to procedures to prevent intoxicated people from driving. After that, I got my quote. (Note that NerdWallet’s address here is made up!)

All in all, this was an easy quote process. And Thimble offers an important service — quick, temporary coverage. But the company could use more transparency around fees, like how many months the initial payment covers.