Optimism abounds for the new year: 63% of Americans say 2026 will be financially better for them than 2025, according to a new NerdWallet survey.

The survey of more than 2,000 U.S. adults, conducted online by The Harris Poll, asked Americans about their confidence to withstand financial setbacks in 2026 and how they think things will go financially in the new year. We also asked about money moves they’ll make in 2026.

Key findings

- One-third of Americans (33%) aren’t confident about their ability to financially withstand a recession if one occurred in 2026.

- Nearly 3 in 5 Americans (57%) plan to make at least one potentially risky money move in 2026, like investing in cryptocurrency (20%) or starting a business (18%).

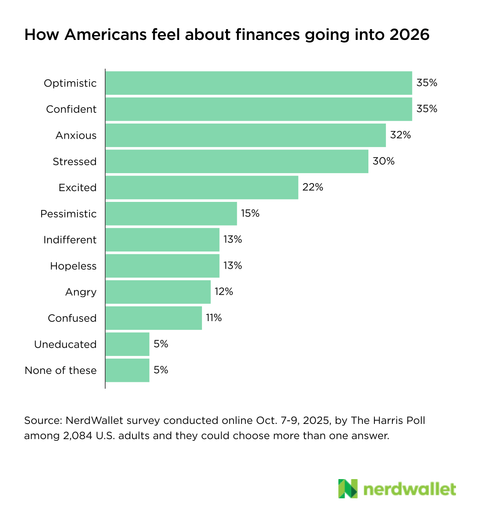

- Over a third of Americans say they feel optimistic (35%) and/or confident (35%) about their finances going into 2026. But nearly as many feel anxious (32%) and/or stressed (30%).

- More than half of Americans (51%) think consumer prices for goods and services will get worse in 2026.

“Making financial and economic predictions for 2026 is difficult. This year has brought a whirlwind of new and potential economic policies (many of them tied up in the courts) and a record-long federal government shutdown. These things don’t only stand to impact your ability to forecast the future, but can have real implications for your household finances,” says NerdWallet Senior Economist Elizabeth Renter.

A majority of Americans say they could handle a financial setback

Generally, Americans think they could handle money misfortune in the new year: The survey finds that they’re more often confident than not about their ability to withstand economic and personal money setbacks if they occurred in 2026.

More than 3 in 5 Americans (62%) feel confident they can financially withstand a 2026 recession, and 67% are confident they could financially withstand tariff-related price increases if they occur in 2026.

Whether this confidence is a sign that many Americans are prepared to handle financial setbacks, or just optimistic about the future, we can only speculate. But according to a recent NerdWallet report, a whopping 70% of Americans report that they’re financially resilient — or able to withstand economic and financial shocks — suggesting that many Americans feel good about their situation, despite the ups and downs in the economy.

Still, plenty of Americans don’t feel confident about their ability to financially withstand a recession (33%), high inflation (33%) or income loss (39%) in 2026, and that’s significant in the current environment. Rising costs and a shaky job market in the year ahead could mean a third or more of the U.S. population could struggle to cover necessities for themselves and their families.

“The confidence to handle economic or financial shocks is a good indicator of how well households are insulated — with savings, available credit or additional income streams,” Renter says. “The 2026 economy may be yet-unknown, but the labor market is currently unfriendly to job seekers and there are risks that it will continue to cool. There are very few households that would weather income loss with no discomfort at all, but the roughly 2 in 5 Americans who don’t know if they could ‘withstand’ it next year are particularly vulnerable.”

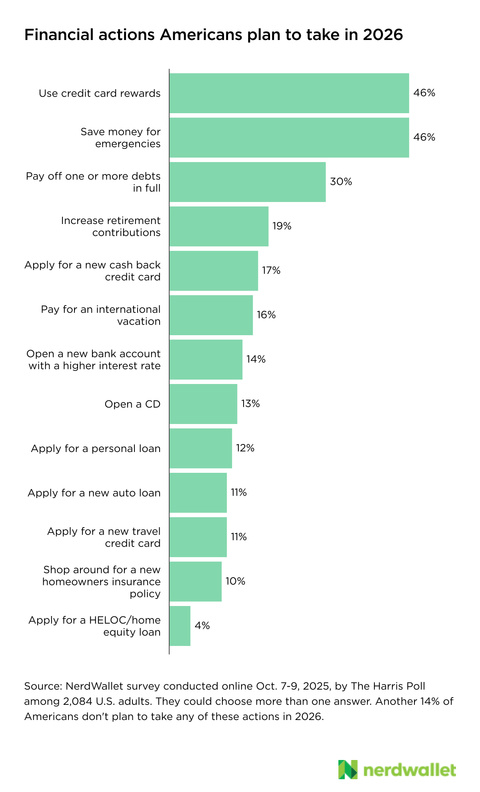

Nearly 3 in 5 Americans plan to take a financial risk in 2026

Americans have plans to make some big money moves in the new year: 57% plan to take at least one potentially risky financial action in 2026, according to the survey. And by “risky”, we don’t mean bad or poorly thought out. Rather, we defined these so-called risky moves as a potentially costly financial action without a certain positive outcome.

One in 5 Americans (20%) say they plan to invest in cryptocurrency in 2026, and 18% plan to invest in AI-related stocks or funds. Some Americans plan to start a business (18%) or buy a new home (17%) in 2026. (We’ll note that these are wildly optimistic statistics based on the number of businesses started and homes purchased in a typical year.)

“Financial risks should always be taken cautiously, after careful consideration of all potential outcomes. If the risk fails, what would recovery look like for you and your household? While the state of the broader economy can certainly play a role in these considerations, much of the decision should rest on the shape of your finances, including the amount of savings you have and the debt you’re currently carrying or may take on,” Renter says.

Americans also plan on taking money steps in the upcoming year with more predictable outcomes. These include using their credit card rewards (46%) and saving money for emergencies (46%), as well as paying off one or more of their debts in full (30%).

Americans split on financial feelings going into the new year

Money feelings going into the new year are pretty mixed: More than a third of Americans feel optimistic (35%) and/or confident (35%) about their financial situation going into 2026. But nearly as many feel anxious (32%) and/or stressed (30%).

Men are more likely than women to say they feel optimistic (40% vs. 31%) or confident (39% vs. 30%) about their financial situation going into 2026, while women are more likely than men to feel anxious (37% vs. 27%) or stressed (35% vs. 24%).

Younger Americans are more likely to go into the new year with feelings of excitement about their finances compared to their older counterparts — 33% of Gen Z (ages 18-28) and millennials (ages 29-44) say this, compared to 20% of Gen X (ages 45-60) and 7% of baby boomers (ages 61-79).

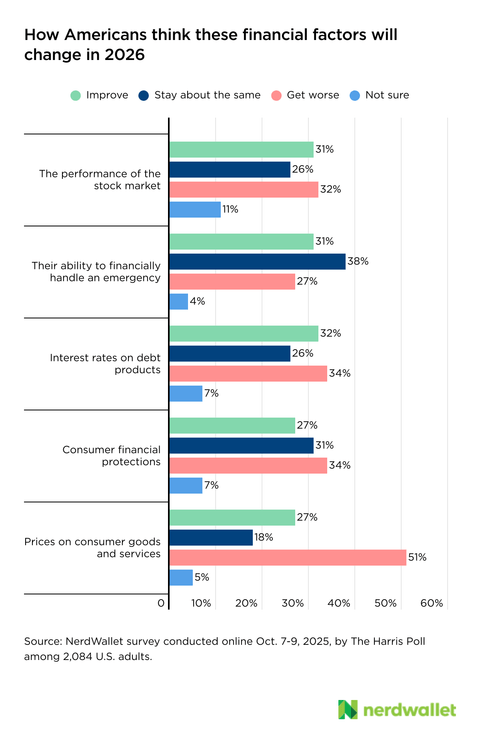

Many Americans say prices will worsen in 2026

So what’s coming next? We asked Americans how they think different financial factors — both personal, like their ability to financially handle an emergency, and broader changes, like interest rates on debt products — might improve or worsen in the new year. And while they’re pretty evenly split on what will happen for most of these factors, there’s a clear outlier: A slight, but notable, majority of Americans (51%) think prices on consumer goods and services will get worse in 2026.

Are they right? It’s impossible to say for sure. We don’t know what the new year will look like, but our feelings about our finances and our predictions about the economy can impact how we behave with money, which can lead to real consequences in the financial world.

“Economic literature shows that people’s expectations shape how they spend and save,” Renter says. “And while some economic optimism is good, and certainly feels better than thinking everything will get worse, consumers should be cautious that their optimism doesn’t drive overspending or reckless financial decisions.”

What you can do in 2026 and beyond

While we hope that 2026 is “your year” financially, it’s undeniable that not every aspect of your financial life is in your control. External factors in the economy and the world at large can impact your money, for good and ill. However, by doing what you can to get your financial house in order — like saving for emergencies, paying off debt and investing for the future — you’ll be better able to weather those unexpected ups and downs.

Save for emergencies: Rainy days come for everyone. Whether that means a burst pipe in your home, a medical emergency or job loss, having money set aside can help turn these emergencies into financial inconveniences rather than calamities.

Experts recommend an emergency fund of three to six months of your basic expenses. If that seems like an insurmountable amount to save up, start with a goal of $1,000, then work toward one month of expenses. A fully funded emergency savings will likely take you years to amass, and that’s OK. Even an in-process emergency fund can help you avoid going into debt when something unexpected arises.

Pay off debt: In addition to costing you interest charges, debt payments may be taking a chunk of your monthly budget that could be put to better use saved, invested or even spent in a way that adds value to your life. Making a debt payoff plan and chipping away at it intentionally every month can help free up those funds.

Some may argue that there’s an ideal way to pay off debt, but the best plan is one that you’ll stick to. So whether you want to pay off your debts based on interest rate, balance or just how much you dislike them, pick a debt payoff strategy and stick with it to knock down your balances.

Invest for the future: We can’t know what the new year will bring, so imagining yourself 20, 30 or 40 years in the future is an impossible task. However, having money ready and waiting gives you options and flexibility no matter what the future holds. Look into available workplace retirement plans (like a 401(k) or 403(b)) and/or an IRA for tax-advantaged retirement savings, and consider whether a taxable brokerage account makes sense for medium term goals that require more flexibility.

» MORE: IRA vs. 401(k): Which is better?

Cite as: NerdWallet (2025). “2026 Consumer Outlook Report — 51% Say Prices Will Get Worse.” Retrieved from https://www.nerdwallet.com/article/studies/2026-consumer-outlook-report

Methodology

The 2026 Consumer Outlook survey was conducted online by The Harris Poll on behalf of NerdWallet from Oct. 7-9, 2025, among 2,084 U.S. adults ages 18 and older. The sampling precision of Harris online polls is measured by using a Bayesian credible interval. For this study, the sample data is accurate to within +/- 2.5 percentage points using a 95% confidence level. This credible interval will be wider among subsets of the surveyed population of interest. For complete survey methodology, including weighting variables and subgroup sample sizes, please contact [email protected].

Disclaimer

NerdWallet disclaims, expressly and impliedly, all warranties of any kind, including those of merchantability and fitness for a particular purpose or whether the article’s information is accurate, reliable or free of errors. Use or reliance on this information is at your own risk, and its completeness and accuracy are not guaranteed. The contents in this article should not be relied upon or associated with the future performance of NerdWallet or any of its affiliates or subsidiaries. Statements that are not historical facts are forward-looking statements that involve risks and uncertainties as indicated by words such as “believes,” “expects,” “estimates,” “may,” “will,” “should” or “anticipates” or similar expressions. These forward-looking statements may materially differ from NerdWallet’s presentation of information to analysts and its actual operational and financial results.