Building credit can be tricky. If you don’t have credit history, or you have a thin credit file, it can be hard to get a loan, a credit card or even rent an apartment.

But how are you supposed to show a history of responsible repayment if no one will give you credit in the first place?

Here are some credit-building tools that can help you break out of that cycle and earn a good credit score.

How to build credit with a credit card | How to build credit without a credit card |

|---|---|

Pay bills on time, every time. | Get credit-builder loan. |

Use 30% or less of your credit limits. | Find a trusted co-signor. |

Ask for a credit limit increase. | Become an authorized user. |

Try a secured card. | Get credit for bills you already pay. |

How to build credit with a credit card

Keep balances low and pay on time

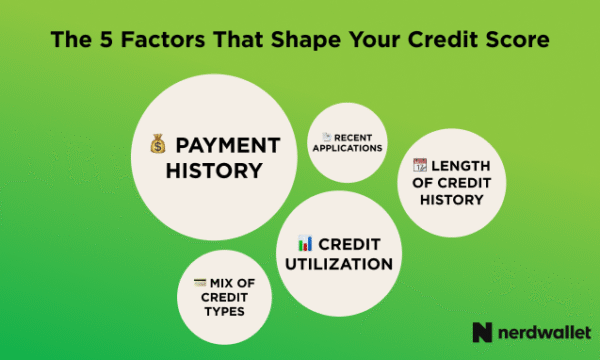

A credit card can be a powerful tool for building credit because it directly affects two key factors in your credit score: payment history and credit utilization.

Used responsibly, you can make purchases, pay the balance in full and avoid interest, all while building a positive history of on-time payments that looks great to potential lenders.

Keeping your balance low also helps your credit utilization, which shows how much of your available credit you're using at a given time.

However, there are downsides to opening a credit card. There is a risk of building up debt that’s hard to pay off, which can lead to costly interest charges. Missing a payment can also hurt your credit score. For example, a payment that's more than 30 days late can stay on your credit report for up to seven years.

Try a secured credit card

If you want to avoid some of the risks of a traditional credit card, consider a secured card. It requires a cash deposit upfront — often starting around $200 — and your deposit usually becomes your credit limit.

Secured cards work like regular credit cards: You make purchases, pay your bill on time, and you may be charged interest if you carry a balance. That means you can still get into debt with most secured cards.

Some newer secured cards work a bit differently. They link your credit limit to a funding account at the same bank, so you can’t spend more than you have deposited. But most secured cards don’t work this way and will charge interest if you carry a balance.

When you close the account in good standing, you typically get your deposit back.

Secured credit cards aren’t meant to be used forever. The goal is to build your credit so you can qualify for an unsecured card — one that doesn't require a deposit and may offer better benefits.

“Think of a secured card as a stepping stone,” says Sara Rathner, a credit cards expert at NerdWallet. “If you pay your credit card statement on time each month and avoid maxing the card out, you can work your way up to cards with generous cash-back and travel rewards programs. Those types of cards require good or excellent credit.”

When choosing a card, look for a low annual fee and make sure it reports payment data to all three credit bureaus: Equifax, Experian and TransUnion.

Your credit score is built using information collected in your credit reports, so cards that report to all three bureaus allow you to build a more comprehensive credit history.

» Ready to get started? Shop the best secured credit cards

Ask for a higher credit limit

If you have a traditional credit card, asking your lender for a higher credit limit can quickly help your score. If approved, the extra credit can lower your credit utilization — the amount of credit you’re using compared with the amount available to you.

The key is to keep your spending the same. That way, you don’t use up the extra room on your card and lose the benefit.

Video: How to build credit as a young person

How to build credit without a credit card

You don’t necessarily need a credit card to build credit. There are several tools that can help you establish a credit history.

Get a credit-builder loan

The purpose of a credit-builder loan is to help people build credit, but it also helps boost savings at the same time.

Typically, the money you borrow is held in an account by the lender and isn't released until the loan is fully repaid. Your payments are reported to the credit bureaus, helping you build a history of on-time payments. These loans are often offered by credit unions and community banks, as well as some online lenders.

Typically, the money you borrow is held in an account by the lender and isn't released until the loan is fully repaid. Your payments are reported to the credit bureaus, helping you build a history of on-time payments. These loans are often offered by credit unions and community banks, as well as some online lenders.

Use a co-signer

It’s also possible to get a loan or an unsecured credit card using a co-signer. A co-signor is someone — often a parent, family member or trusted friend — who agrees to apply with you and share responsibility for the account. Because the co-signor typically has stronger credit, it can help you qualify or get better terms.

But be sure that both of you understand the risks. The co-signer is legally on the hook for the full amount owed if you don't pay, and any missed payments can hurt both your credit scores.

An authorized user is someone who is added to another person's credit card account without being responsible for the balance. Because the account appears on their credit report, they can benefit from the primary cardholder's on-time payments, low credit utilization and longer credit history.

Before an authorized user is added, both parties should agree on whether and how the authorized user can use the card. Authorized users don't have to use — or even carry — the card at all to benefit from the arrangement.

After a few months, the account may appear on the authorized user’s credit reports. But not all issuers report authorized user activity, so it’s important that the primary cardholder check first.

This strategy can be helpful for someone new to credit, and it may speed up the process of building a credit score and establishing a positive credit history. The goal is to use this as a stepping stone to build an authorized user’s own credit so that when the primary cardholder removes them from their account, any impact on their score is minimal

Get credit for rent and utility payments

Rent-reporting services take a bill you're already paying and add it to your credit reports. This helps to build a positive history of on-time payments. Some rent reporting services are provided by landlords or property managers and renters can opt in, while other services come at a cost to the renter.

Not every credit score takes these payments into account, but some do, and that may be enough to get a loan or credit card that firmly establishes your credit history for all lenders.

You can get credit for other kinds of bills, too. For example, Experian Boost offers a way to have your cell phone and utility bills reflected in your credit report with that credit bureau. Note that the effect is limited only to your credit report with Experian — and any credit scores calculated using Experian credit report data.

Key habits for credit score maintenance

Make on-time payments and pay at least the minimum

Paying credit card or loan payments on time, every time, is the most important thing you can do to help build your score. If you are able to pay more than the minimum, that is also helpful for your score.

Keep your credit utilization at 30% or less

Credit utilization is the percentage of your credit limit you use. We recommend keeping your credit utilization below 30% on all cards when possible. The lower your utilization, the better it is for your score.

Space out credit applications

Credit applications can cause a small, temporary drop in your score. However, multiple applications during a short period of time can cause significant damage. NerdWallet recommends spacing applications by about six months if you can.

Keep old credit card accounts open, even if you don’t use them much

Unless you have a compelling reason to close an account, like a high annual fee or poor customer service, consider keeping it open. Closing an account can affect your credit utilization. You can also explore downgrading it or transferring your credit limit to another card.

» LEARN: What affects your credit score?

Check your credit scores and credit reports

There are two things you should check often to stay on track as you build your credit:

Check credit reports for errors and account activity

A credit report shows how you've used credit in the past.

You have three credit reports, one from each major credit bureau. Your credit report contains your personal information (like your name, addresses, phone numbers), a list of all your accounts and their balances and any recent credit checks made by lenders. It also includes negative marks, such as missed payments and bankruptcies.

Request your credit reports and check each for errors and discrepancies. You can check your reports for every week by using AnnualCreditReport.com. Dispute any credit report errors you find that might be lowering your scores.

Get your credit reports in Spanish

You can request your credit report in Spanish directly from each of the three major credit bureaus:

- TransUnion: Call 800-916-8800.

- Equifax: Visit the link or call 888-378-4329.

- Experian: Click on the link or call 888-397-3742.

Usted puede solicitar una copia de su informe crediticio (gratis y en español) de cada una de las tres principales agencias de crédito:

- TransUnion: Llame al 800-916-8800.

- Equifax: Visite el enlace o llame al 888-378-4329.

- Experian: Haga clic en el enlace o llame al 888-397-3742.

Review credit scores to track your progress

Your credit score predicts how you'll handle credit in the future, using the information in your credit reports. Credit scores fall anywhere between 300 to 850, and the higher the score, the better.

Your credit scores might differ slightly based on which company is calculating the score (FICO or VantageScore). Your credit score is not found on your credit reports, but you can look at your monthly bank statements or bank app to get a free score.

Meet MoneyNerd, your weekly news decoder

So much news. So little time. NerdWallet's new weekly newsletter makes sense of the headlines that affect your wallet.

Tips for building credit from Redditors

We used AI to sift through Reddit forums and get a pulse check on building credit. Here are the tips that rose to the top of our analysis. People post anonymously, so we cannot confirm their individual experiences or circumstances.

Reddit users focus on simple credit-building habits: pay on time, keep things easy and let your accounts age over time.

One message comes up again and again: don’t overthink it. Open a starter credit card and use it for everyday spending. Users suggest using preapproval tools (Capital One and Discover are popular) to make sure you qualify before applying. Then set up autopay to pay your full balance each month.

Reddit users also push back on common myths. You don’t need to carry a balance to build credit, and focusing too much on your score can be misleading. They point out details that are often glossed over.

For example, being an authorized user can help, but your own accounts matter more.; They note that many free scores are VantageScore. But FICO is more popular among lenders.

Users continually stress that you can build credit for free by using a credit card responsibly, which helps avoid interest and fees entirely.

Frequently Asked Questions

What’s the No. 1 way to build a good credit score?

The most important thing you can do to build a strong score is to make all your payments on time. FICO and VantageScore, the two major credit scoring companies, weigh payment history as the biggest credit scoring factor. That means, somewhere between 30% to 35% of your credit score is determined by your record of making on-time payments.

How do you build credit fast?

If you’re just starting out, you might be wondering how long it takes to build credit. Building a good credit score takes time and a history of on-time payments. To have a FICO score, you need at least one account that’s been open six months or longer and at least one creditor reporting your activity to the credit bureaus in the past six months. A VantageScore, from FICO's biggest competitor, can be generated more quickly.

How can an 18-year-old build credit?

Becoming an authorized user on a trusted adult’s credit card can help you take advantage of someone else’s long credit history and record of on-time payments without financial responsibility for the bill. If you are responsible for rent payments or other utility payments, you can enroll in a service that gives credit for on-time payments.