One of the Chase Sapphire Reserve®'s marquee benefits — and a key way to justify the card’s hefty $795 annual fee — is its annual dining statement credit.

It’s a $300 annual statement credit, split into one $150 statement credit for dining purchases processed between January 1 and June 30, and another for July 1 through December 31. The credit applies to Sapphire Reserve Exclusive Tables restaurants, a curated collection on OpenTable, the dining reservation platform. It's automatic, with no minimum spend and no complex activation required.

After spending a year trying to maximize this benefit in my home base of San Francisco, I have a few tried-and-true tips.

I check the restaurant list, because it changes

In July 2026, the Sapphire Reserve Exclusive Tables Collection got a major update that should come as good news for most (but bad news for some, including many diners in Las Vegas).

The good news, which I confirmed with Chase, is that it just added about 90 new restaurants nationwide. Notable additions to the program include:

- Bacanora (Phoenix).

- Kasama (Chicago).

- Bludorn (Houston).

- The Pink Door (Seattle).

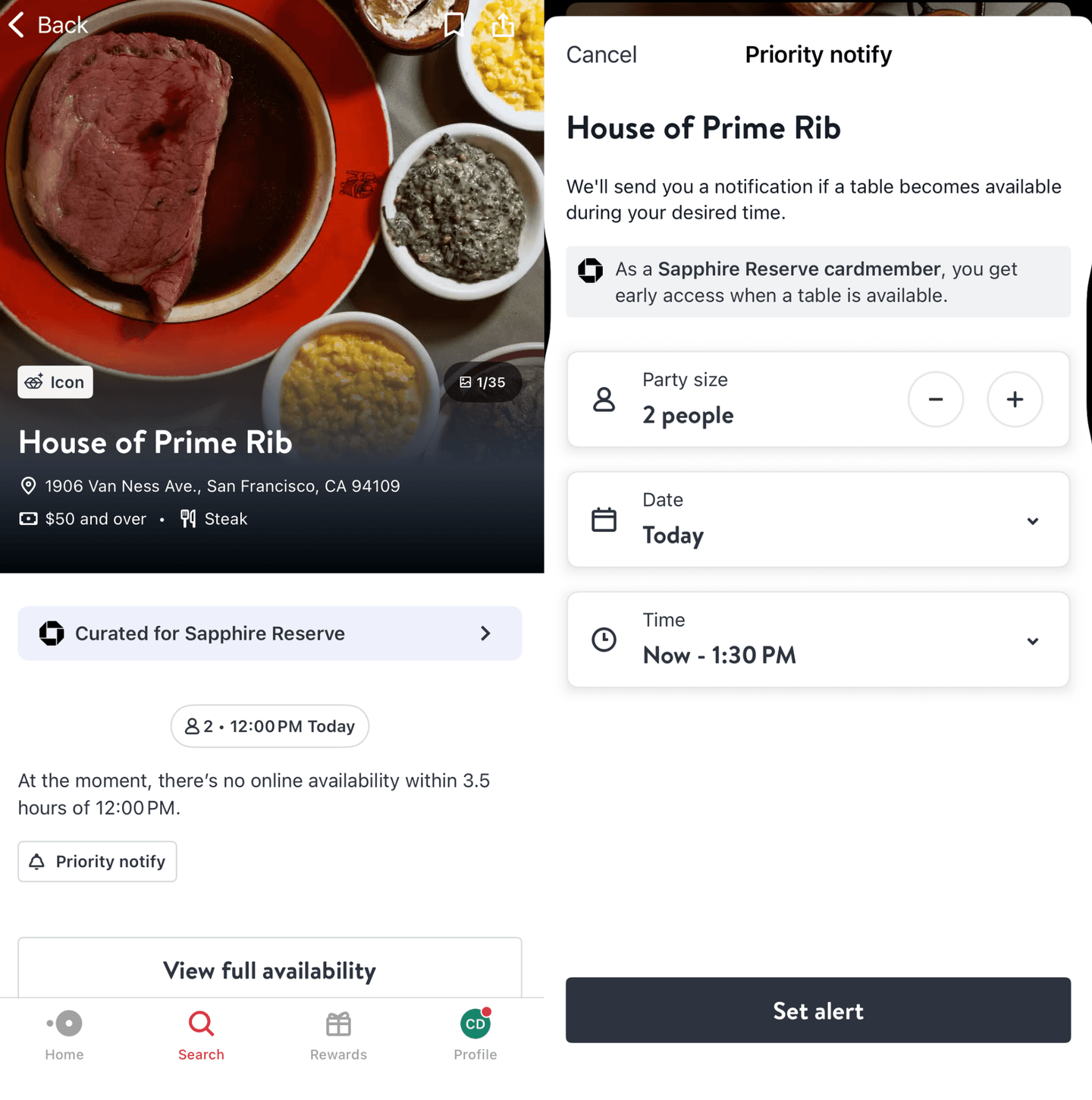

In San Francisco, the addition of the iconic House of Prime Rib is a game-changer for fans of classic dining and hearty steaks (hello, me!), though it’s notoriously hard to book.

But the program also removed about 70 restaurants, including many in Las Vegas, where you’ll find just one restaurant on the platform.

It’s also worth noting that smaller cities still have few or no options, though. In all of Maine, there are just three eligible restaurants, and all are in Portland. The entire state of New Mexico has just one option, and it’s in Albuquerque.

You can browse the updated OpenTable collection to ensure your favorite restaurant wasn’t removed (or perhaps be delighted to find a new restaurant on the list!).

I use the Priority Notify feature

By connecting your Chase Sapphire Reserve® to OpenTable, you get a priority window to book reservations before the general public. In competitive dining markets, this alone is a real perk — and you can bet I’ll be using this to land a House of Prime Rib reservation.

I check prices ahead of time

The restaurants in the Sapphire Reserve Exclusive Tables Collection lean heavily toward high-end, chef-driven establishments. They’re great for the "foodie" experience, but they can also create a challenge for the budget.

In a city like San Francisco, it’s incredibly difficult to walk out of any of these restaurants with a bill under $150 for two. For example, at Saison, a tasting menu ranges from $368 to $566 per person. To be fair, the restaurant holds two Michelin stars, and I’m not saying it’s not worth it. I’m just saying that — even with the credit — it’s tough not to find yourself paying a significant chunk out of pocket when you use it.

I’ve found a few gems in San Francisco that don’t cost as much, including Vietnamese restaurant Bodega SF, where I usually get away with owing just a couple of extra dollars at the end.

I don’t cut it too close to the deadline

Because this $300 credit is split into two $150 windows (January through June, and July through December), timing your meals is everything. Waiting until the final day of a six-month period to treat yourself to an expensive dinner is risky.

That’s because Chase calculates the credit based on the official date the transaction posts to your statement rather than the date you physically signed the receipt. Typically, credit card charges don't post to your account immediately (when you swipe or drop your card at a restaurant, the charge initially sits as a "pending" transaction) and instead take anywhere from two to five business days for the merchant to finalize and settle the bill.

Give yourself at least a week’s buffer before the end of each six-month window to ensure you get the credit for the period you intended.

I stack rewards with other dining programs

You don’t have to rely solely on the dining credit to maximize your rewards on this meal. Here are some ways I "triple-dip" a single meal:

- Credit card multipliers: When you pay the bill with your Chase Sapphire Reserve®, you will still earn the bonus 3x Ultimate Rewards® points per dollar spent on your dining purchase — even on the portion of the bill that gets erased by the statement credit.

- OpenTable rewards: OpenTable has its own rewards program that lets you earn 100 points per standard reservation, and up to 1,000 points per booking for select restaurants. You can turn those points into credits toward your dining bills or Amazon gift cards.

- Frequent flyer or other bank dining programs: Link your card to a secondary dining rewards program such as MileagePlus Dining (United Airlines), SkyMiles Dining (Delta Air Lines) or AAdvantage Dining (American Airlines). If your restaurant is part of their program, you'll automatically trigger bonus airline miles in the background. I have my card linked to my Bilt Rewards account and have earned bonus Bilt from my Bodega SF meals — even though I paid with my Chase Sapphire Reserve® rather than a Bilt-branded credit card.

My honest take

The Chase Sapphire Reserve® dining credit is one of the easiest credits to use in the premium card space. It avoids the "spend to get" games that make other cards feel like a chore. However, because the network is curated toward high-end dining, you shouldn't view it as a way to "eat for free.” Instead, view it as a $300 "gift card" toward the premium dining experiences you were already planning to seek out.

How to maximize your rewards

You want a travel credit card that prioritizes what’s important to you. Here are some of the best travel credit cards of 2026:

- Flexibility, point transfers and a large bonus: Chase Sapphire Preferred® Card

- No annual fee: Wells Fargo Autograph® Card

- Flat-rate travel rewards: Capital One Venture Rewards Credit Card

- Bonus travel rewards and high-end perks: Chase Sapphire Reserve®

- Luxury perks: American Express Platinum Card®

- Business travelers: Ink Business Preferred® Credit Card

Explore more on