The investing information provided on this page is for educational purposes only. NerdWallet, Inc. does not offer advisory or brokerage services, nor does it recommend or advise investors to buy or sell particular stocks, securities or other investments.

Understanding financial health

Financial health is your ability to handle money stress and reach your long-term goals. The areas of financial health typically considered are:

- Net worth: The value of everything you own minus everything you owe gives you a picture of your wealth. Tracking this number over time shows whether you're moving in the right direction.

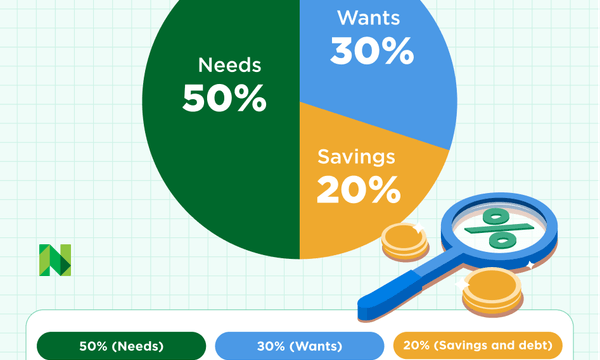

- Savings and debt paydown: Are you able to cover your needs, your wants and still have enough to build savings and pay down debt over time? The 50/30/20 budget is a good measure.

- Debt-to-income ratio: This comparison of your monthly debt payments to your monthly gross income gives you a good idea of how manageable your debt load is. Lenders often use it to weigh approval decisions — many look for a DTI of 36% or below.

- Credit score: A good score (from the mid-600s to mid-700s) or excellent score (in the high 700s or above) can help even if you don't plan to apply for more credit. Scores can affect apartment applications, insurance costs, utility deposits and more.

- Emergency fund: Having enough in the bank to weather financial shocks protects you from debt spirals and credit score damage from missing bill payments. Aim for three to six months' worth of expenses (a few hundred dollars is a good start).

- Insurance: This protects assets such as vehicles, personal possessions and your home. It can also protect dependents in case you're unable to work.

- Financial planning: Staying financially healthy means saving toward retirement, working on estate planning and more.

» MORE: Get your free credit score with NerdWallet

Meet MoneyNerd, your weekly news decoder

So much news. So little time. NerdWallet's new weekly newsletter makes sense of the headlines that affect your wallet.

How to improve your financial health

For most people, attaining financial health is a journey — one that lasts a lifetime. Very few people are lucky enough to have instant security from generational wealth or a massive lottery jackpot.

Instead, the progression tends to look like this: build a foundation, strengthen your finances and grow your wealth.

1. Build a foundation

Start by creating an emergency fund, balancing expenses and building your credit score. Begin planning for retirement as soon as you can to give your savings more time to grow through compound interest.

These guides can help you handle basics, like choosing a bank, getting some savings going and learning how to manage money:

- How to Build an Emergency Fund: Financial shocks are common: Nearly 6 in 10 adults had at least one major, unexpected expense in the past 12 months, according to the Fed's Economic Well-Being of U.S. Households in 2025. Saving even a few hundred dollars can keep shocks from derailing your financial life.

- How to Build a Budget: A plan for maximizing your money doesn’t have to be complex.

- How to Build Credit: Building your score can save you money and let you borrow at better rates.

Setbacks can hit anyone, at any time. If you're having trouble keeping up with your bills and don’t have a financial cushion, explore these resources that may help you and lay the groundwork for greater financial security:

- Get Help Paying Your Bills: If you can't cover everything, check out these resources for help and strategies to minimize the fallout.

- Ways to Get Free Money From the Government: Programs include help with utility costs, child care, college — and even a down payment on a house.

- Beware of Predatory Lenders: Know the warning signs of a toxic loan.

2. Strengthen your finances

As you gain momentum, continue to grow your financial stability. This could mean things like paying down debt balances and knowing what your needs will be in retirement. Paying bills on time and keeping track of your credit score can help push it higher, which gives you more financial choice.

You may be thriving in some areas but not yet on top of others. Here are ways to address possible financial pain points and shore up your security.

Manage debt

- Tools and Tips to Pay Off Debt: Learn strategies to speed up debt payoff.

- Understanding Debt Relief: Struggling with debt? Learn options for help, plus their pros and cons.

Keep building your credit score

- How to Build Credit Fast: Adding more points to your score saves you money and unlocks access to things you want.

- How to Rebuild Your Credit: If you’ve made some missteps, you can recover — these strategies will help.

Work toward financial goals

- How to Manage Your Money: These strategies help you make sure each dollar does the most for you.

- Intro to Retirement Planning: Start where you are and with what you have. Every bit helps.

- Beginner Guide to Investing: What to know about goals, timelines and the amount of risk that makes sense for you.

- College Savings Strategies: Explore the ways you can set aside money over time and find the best plan.

Save for a home

- First-Time Home Buyer Guide: Those new to the housing market have some key help.

- Buying a Home With Bad Credit: It is possible — here’s what to know.

- How to Save for a Down Payment: You might not need as much as you think.

- How Much House Can I Afford? Enter your income, monthly debt payments and available cash for a down payment to get your answer.

3. Grow your wealth

Financially healthy people successfully manage all areas of their financial life. They have good to excellent credit, a handle on debt, an emergency fund and a retirement fund. If that's you, stay the course and hit your financial goals.

Here are some resources to maximize your efforts and ensure you’re getting the most out of the optimal position you’re in.

Maintain financial health

- Net Worth Calculator: Enter your assets and liabilities to measure your net worth.

- The Benefits of Diversification: Why financial pros suggest you spread investment dollars across a range of assets to reduce investment risk.

- Choosing a Financial Advisor: Find a professional to help you meet your goals.

Save and invest for retirement

- IRAs vs. 401(k): How to Choose: How to weigh what account is best for you.

- How to Invest in Stocks: Get started with an online brokerage account — it’s easier than you might think.

- Best Investments: Fine-tune your approach, depending on your circumstances.

- Choosing the Best Index Funds: It all starts with deciding a goal for your money.

Meet MoneyNerd, your weekly news decoder

So much news. So little time. NerdWallet's new weekly newsletter makes sense of the headlines that affect your wallet.Article sources

NerdWallet writers are subject matter authorities who use primary, trustworthy sources to inform their work, including peer-reviewed studies, government websites, academic research and interviews with industry experts. All content is fact-checked for accuracy, timeliness and relevance. You can learn more about NerdWallet's high standards for journalism by reading our editorial guidelines.

- 1.Federal Reserve Board. Economic Well-Being of U.S. Households in 2025. Accessed Jul 7, 2026.