We believe everyone should be able to make financial decisions with

confidence. While we don't cover every company or financial product on

the market, we work hard to share a wide range of offers and objective

editorial perspectives.

So how do we make money? Our partners compensate us for advertisements that

appear on our site. This compensation helps us provide tools and services -

like free credit score access and monitoring. With the exception of

mortgage, home equity and other home-lending products or services, partner

compensation is one of several factors that may affect which products we

highlight and where they appear on our site. Other factors include your

credit profile, product availability and proprietary website methodologies.

However, these factors do not influence our editors' opinions or ratings, which are based on independent research and analysis. Our partners cannot

pay us to guarantee favorable reviews. Here is a list of our partners.

What Is a HELOC, or Home Equity Line of Credit?

A HELOC lets you borrow against your home's value to access cash as needed.

Taylor Getler is a home and mortgages writer for NerdWallet. Her work has been featured in outlets such as MarketWatch, Yahoo Finance, MSN and Nasdaq. Taylor is enthusiastic about financial literacy and helping consumers make smart, informed choices with their money.

Kate Wood is a lending expert and certified financial health counselor (CHFC) who joined NerdWallet in 2019. With an educational background in sociology, Kate feels strongly about issues like inequality in homeownership and higher education, and relishes any opportunity to demystify government programs. Prior to NerdWallet, she wrote about home remodeling, decor and maintenance for This Old House.

Johanna Arnone helps lead coverage of homeownership and mortgages at NerdWallet. She has more than 15 years' experience in editorial roles, including six years at the helm of Muse, an award-winning science and tech magazine for young readers. She holds a Bachelor of Arts in English literature from Canada's McGill University and a Master of Fine Arts in writing for children and young adults.

Practice making complicated stories easier to understand comes in handy every day as she works to simplify the dizzying steps of buying or selling a home and managing a mortgage. Johanna has also completed coursework in Boston University’s Financial Planning Certificate program. She is based in New Hampshire.

Updated

How is this page expert verified?

NerdWallet's content is fact-checked for accuracy, timeliness and

relevance. It undergoes a thorough review process involving

writers and editors to ensure the information is as clear and

complete as possible.

A home equity line of credit, or HELOC, is a second mortgage that gives you access to cash based on the value of your home. You borrow against your equity, which is the home’s value minus the amount you owe (if anything) on your primary mortgage. While every lender has its own borrowing limit, you can usually borrow up to 85% of your equity.

You can make withdrawals from your line of credit up to your limit, which you’ll pay back in monthly installments. Since a HELOC is backed by your home, you’ll likely get a better interest rate than you would for an unsecured loan.

You could lose your home to foreclosure if you can’t keep up with payments, so it’s best to use your equity in a way that will build your wealth, like for home improvements.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account loan types and loan products offered, online conveniences, online mortgage rate information, and the rate spread and origination fee lenders reported in the latest available HMDA data.

HELOCs are broken up into two parts: the draw period, which you can think of as the borrowing period, and the repayment period.

Draw period: You can borrow money from the account, up to your approved limit. You have to make interest payments, but payments towards the principal are optional. This period typically lasts 10 years.

Repayment period: You can’t take out any more money, and you have to pay towards principal and interest until you’ve paid off what you’ve borrowed. If you chose not to pay towards the principal balance during the draw period, your minimum payments could go up by a lot. The length of the repayment period varies, but you’ll usually have up to 20 years.

How you’ll access your HELOC

You’ll have a few options to withdraw money from your HELOC, depending on what your lender offers. For example, you can access it via online transfer, with a bank card at an ATM or you can write checks from the account.

HELOC costs

In addition to interest, there are other costs to consider before taking out a HELOC.

Closing costs, which are often between 2% and 5% of the loan amount. Some lenders don’t charge closing costs at all, but be aware that this can require you to keep the line open for a certain amount of time.

Annual fees. Some lenders charge annual fees for HELOC customers, which are often around $50 per year.

HELOC requirements

Lender requirements will vary, but here's what you'll generally need to get a HELOC:

What should I look for when comparing HELOC options?

Taylor Getler

Lead Writer and Content Strategist

As a homeowner, you're probably familiar with what it's like to shop for a mortgage. Finding the right HELOC is a little different, however, because these products can be totally customized from lender to lender. Conventional and government-backed mortgages have strict guidelines that all lenders must follow. While HELOCs have industry norms, there's not exactly a rule book. This means that the little details really matter — fees, repayment terms, minimum draw requirements and and flexibility can all affect how much this loan really costs you over time.That’s what I focused on when building our best HELOC lenders list. It’s an easy place to help you start comparing without needing to comb through the fine print, because we've done that for you. We reviewed 35+ lenders and assessed them across 14 categories. I even stayed on hold with one lender for over 20 minutes to put their customer service to the test!

As a homeowner, you're probably familiar with what it's like to shop for a mortgage. Finding the right HELOC is a little different, however, because these products can be totally customized from lender to lender. Conventional and government-backed mortgages have strict guidelines that all lenders must follow. While HELOCs have industry norms, there's not exactly a rule book. This means that the little details really matter — fees, repayment terms, minimum draw requirements and and flexibility can all affect how much this loan really costs you over time.That’s what I focused on when building our best HELOC lenders list. It’s an easy place to help you start comparing without needing to comb through the fine print, because we've done that for you. We reviewed 35+ lenders and assessed them across 14 categories. I even stayed on hold with one lender for over 20 minutes to put their customer service to the test!

Taylor Getler

Lead Writer and Content Strategist

Taylor Getler

Lead Writer and Content Strategist

As a homeowner, you're probably familiar with what it's like to shop for a mortgage. Finding the right HELOC is a little different, however, because these products can be totally customized from lender to lender. Conventional and government-backed mortgages have strict guidelines that all lenders must follow. While HELOCs have industry norms, there's not exactly a rule book. This means that the little details really matter — fees, repayment terms, minimum draw requirements and and flexibility can all affect how much this loan really costs you over time.That’s what I focused on when building our best HELOC lenders list. It’s an easy place to help you start comparing without needing to comb through the fine print, because we've done that for you. We reviewed 35+ lenders and assessed them across 14 categories. I even stayed on hold with one lender for over 20 minutes to put their customer service to the test!

As a homeowner, you're probably familiar with what it's like to shop for a mortgage. Finding the right HELOC is a little different, however, because these products can be totally customized from lender to lender. Conventional and government-backed mortgages have strict guidelines that all lenders must follow. While HELOCs have industry norms, there's not exactly a rule book. This means that the little details really matter — fees, repayment terms, minimum draw requirements and and flexibility can all affect how much this loan really costs you over time.That’s what I focused on when building our best HELOC lenders list. It’s an easy place to help you start comparing without needing to comb through the fine print, because we've done that for you. We reviewed 35+ lenders and assessed them across 14 categories. I even stayed on hold with one lender for over 20 minutes to put their customer service to the test!

Taylor Getler

Lead Writer and Content Strategist

Taylor Getler

Lead Writer and Content Strategist

As a homeowner, you're probably familiar with what it's like to shop for a mortgage. Finding the right HELOC is a little different, however, because these products can be totally customized from lender to lender. Conventional and government-backed mortgages have strict guidelines that all lenders must follow. While HELOCs have industry norms, there's not exactly a rule book. This means that the little details really matter — fees, repayment terms, minimum draw requirements and and flexibility can all affect how much this loan really costs you over time.That’s what I focused on when building our best HELOC lenders list. It’s an easy place to help you start comparing without needing to comb through the fine print, because we've done that for you. We reviewed 35+ lenders and assessed them across 14 categories. I even stayed on hold with one lender for over 20 minutes to put their customer service to the test!

As a homeowner, you're probably familiar with what it's like to shop for a mortgage. Finding the right HELOC is a little different, however, because these products can be totally customized from lender to lender. Conventional and government-backed mortgages have strict guidelines that all lenders must follow. While HELOCs have industry norms, there's not exactly a rule book. This means that the little details really matter — fees, repayment terms, minimum draw requirements and and flexibility can all affect how much this loan really costs you over time.That’s what I focused on when building our best HELOC lenders list. It’s an easy place to help you start comparing without needing to comb through the fine print, because we've done that for you. We reviewed 35+ lenders and assessed them across 14 categories. I even stayed on hold with one lender for over 20 minutes to put their customer service to the test!

Taylor Getler

Lead Writer and Content Strategist

Today’s HELOC rates

Rates vary by lender, and the annual percentage rate, or APR, that you’re offered depends on factors such as your credit score, debt and the amount you need to borrow.

Most HELOC rates are indexed to a base rate called the prime rate, which is the lowest credit rate lenders are willing to offer their most attractive borrowers. Lenders consider a borrower’s profile, and add a margin to the prime rate to calculate a rate offer.

For example, if a lender adds a margin of 1.5% to a prime rate of 8.5%, that borrower’s rate will be 10%.

Prime Rate, Effective 12/11/25

Current prime rate — last changed Dec. 2025

Prime rate last week

Prime rate in the past year — low

Prime rate in the past year — high

Projected median prime rate for 2026

6.75%

6.75%

6.75%

7.5%

6.8%

Variable vs. fixed interest rates

Most HELOCs have adjustable interest rates. This means that as interest rates go up or down, your HELOC rate will change too.

Some lenders also offer a fixed-rate option. This lets you lock in your APR when you draw from your equity, which protects your loan from rising interest rates and can make long-term financial planning a little easier.

Getting the best HELOC rate

You should shop around with at least three lenders when looking for the best HELOC rate. Check your bank or mortgage provider to see if they offer discounts to existing customers. Also, take note of introductory offers like initial rates that will expire at the end of a given term.

After you’ve completed the application process, you’ll go through underwriting. This can take several weeks. Once you’ve been approved you’ll close on the loan and sign the paperwork.

🤓Nerdy Tip

Don't assume the price you paid at closing is what your home is worth today. If home prices in your area have gone up while you've owned your home, you may have more equity than you realize. You can estimate your home’s current value here.

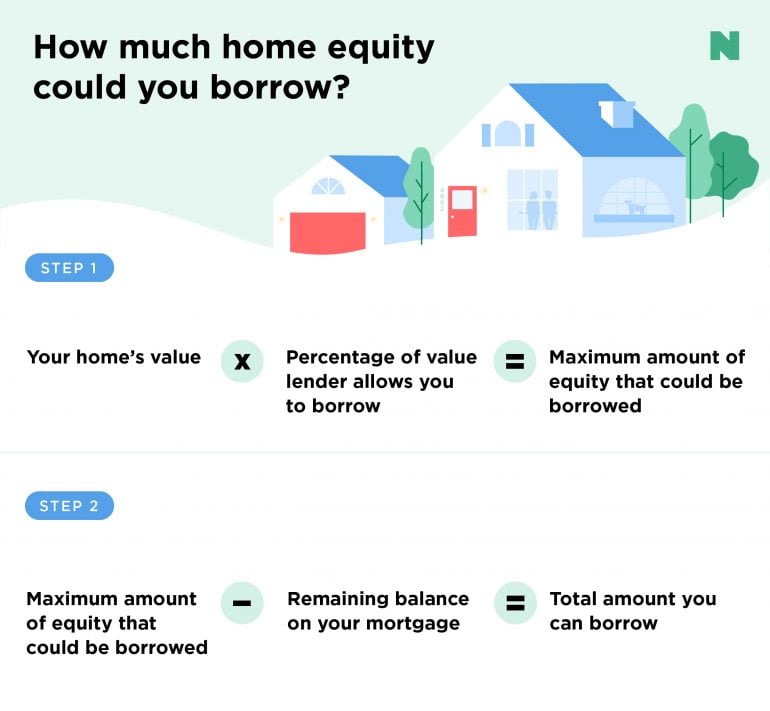

How much can you borrow with a HELOC?

The maximum amount of your home equity line of credit will vary based on the value of your home, the lender’s maximum borrowing limit and how much you owe on your mortgage. Two quick calculations can give you an idea of what you might be able to borrow with a HELOC.

Your home's current value x the percentage of value the lender allows you to borrow = the maximum amount of equity that could be borrowed.

Maximum amount of equity that could be borrowed - the remaining balance on your mortgage = the total amount you can borrow.

Say you have a home worth $300,000 with a balance of $200,000 on your first mortgage and your lender will allow you to access up to 85% of your home’s value. Multiplying the home's value ($300,000) by the percentage the lender will allow you to borrow (85%, or 0.85) gives you a maximum amount of $255,000 in equity that could be borrowed. Subtract the amount you still owe on your mortgage ($200,000) to get the total amount you can borrow with a HELOC — $55,000.

Is getting a HELOC a good idea?

Whether a home equity line of credit is a good idea really comes down to your goals and financial situation.

Pros

A HELOC is often used for home repairs and renovations, which can increase your home's value.

You could get a better rate with a HELOC than with an unsecured loan.

The interest on your HELOC may be tax-deductible if you use the money to buy, build or “substantially improve” your home, according to the IRS. This requirement expires after the 2025 tax year.

Cons

You run the risk of foreclosure if you can’t pay the loan.

A HELOC is not recommended if your income is unstable or if you won’t be able to afford payments if interest rates rise.

It may not be the best choice if you’re planning to move soon. One of the main benefits of a HELOC is its long borrowing and payment timeline, and you’ll have to pay it off entirely at the time of sale.

A HELOC may also not be the right choice if you aren’t looking to borrow much money (in which case the costs may not be worth it, and you should consider a low interest credit card instead), or if you intend to use it for basic needs, small purchases or expenses that don’t build personal wealth (like a new car or vacation).

Is it better to get a home equity loan or line of credit?

Choosing between a HELOC and a home equity loan depends on your financial situation and needs. The main difference between the two loan products is that a HELOC is a line of credit that you can draw from as needed, while a home equity loan is a lump sum that you receive all at once.

This makes HELOCs more suited to borrowers who want flexibility, while a home equity loan could be a fit for a borrower who wants the full loan amount upfront.

Another key difference is that HELOCs typically have variable interest rates, while home equity loans have fixed interest rates. Some borrowers prefer home equity loans because the payments are fixed and predictable.

What to do if you can’t keep up with your HELOC payments

Because most HELOCs have an adjustable rate, it’s possible your payments could exceed what you’d originally planned. If you can’t pay back what you’ve withdrawn, the lender could foreclose on your home. This makes it important to act fast if there’s a problem. Reach out to the lender to understand your options, and consider refinancing to lower your rate or change your payment terms.

Frequently Asked Questions

What is the monthly payment on a $50,000 HELOC? What is the monthly payment on a $50,000 HELOC?

Your monthly payment for a $50,000 HELOC draw would depend on factors like your interest rate, the value of your home and your remaining mortgage balance.

For example, let’s assume your home is worth $300,000. Since most HELOC lenders have a maximum borrowing limit of 85% CLTV, your remaining mortgage balance can’t be more than $205,000 to borrow $50,000.

If you drew $50,000 from your HELOC at a rate of 8.9%, your initial minimum payments could be about $370. This would change if your interest rate fluctuates: the prime rate could go up or down. It would also change when your minimum payment begins to include principal after the end of the draw period.

Is there a downside of having a HELOC? Is there a downside of having a HELOC?

The main downside to having a HELOC is the risk that come with having a secured loan. HELOCs are backed by your home, meaning that you could lose it if you can’t make your minimum monthly payments.

Is HELOC interest tax-deductible? Is HELOC interest tax-deductible?

You may be able to claim a tax deduction on your HELOC interest if you used the loan for home improvements. This requirement is set to expire after the 2025 tax year.

How does a HELOC affect your credit score? How does a HELOC affect your credit score?

Like any line of credit, a new HELOC on your report will likely reduce your credit score temporarily. However, if you borrow responsibly — making timely payments and not utilizing the full credit line — your HELOC could help you build your credit score over time.