Most budgets are built around your expenses. But the pay-yourself-first method flips that approach on its head by saving before you spend on anything else, even bills.

Instead of waiting to see what’s left at the end of the month, you set aside part of your paycheck as soon as you get it. This method is also called “reverse budgeting.”

Pay yourself first definition

'Pay yourself first' is a reverse budgeting strategy where you build your spending plan around savings goals, such as retirement, instead of focusing on fixed and variable expenses. This prioritizes savings, but not at the expense of necessary expenses like housing, utilities and insurance.

How pay yourself first budgeting works

Use these steps to set up your own reverse budget.

Step 1: Assess your spending

To make this budget successful, you’ll have to prepare. Rachel Podnos O’Leary, a certified financial planner in Austin, Texas, recommends reviewing your typical spending by pulling up your bank and credit card statements.

“Do the math and start conservative,” Podnos O’Leary says. “You can always increase (your savings contributions) later. You don’t want to risk an overdraft or bounced check or something like that.”

Step 2: Determine how much to pay yourself

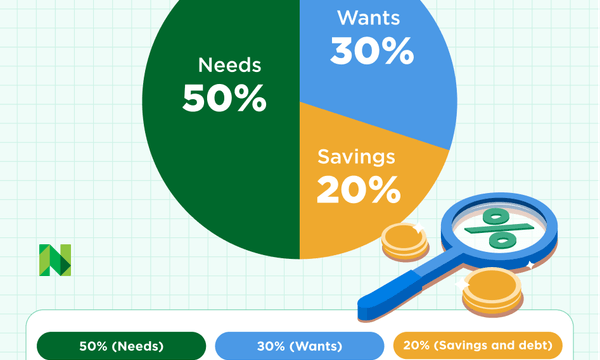

Let’s say you make $3,400 a month. Using this plan, you’d first put aside about $680 for savings. Then you'd allocate $1,700 for needs and $1,020 for wants. This example shakes out to 50% on needs, 30% on wants and 20% on savings, like with the 50/30/20 budget, but in reverse budgeting, the amounts aren’t set in stone. You can adjust your saving and spending percentages as needed to fit your life. For example, you might save more and spend less on wants if you want to reach your goals faster.

Step 3: Identify your savings goals

Make a list of your short-term and long-term savings goals. Saving for retirement and building an emergency fund should be your first priorities, followed by paying down debts like a mortgage, auto loan or student loans.

You can put a little money toward each goal or choose a couple to focus on first. Decide how much you need to reach those goals and how much you can afford to save each month.

For example, if you take home $3,400 a month, 20% — or $680 — would go toward savings and extra debt payments. Let’s say you save $200 for your emergency fund and $250 for retirement. That’s $450 total. You’d “pay yourself” that money first, and the leftover $230 from your savings category could go toward paying down debt. The rest of your income — $2,720 — would be split between needs and wants.

Just remember: the 20% savings category covers retirement and your emergency fund. Other savings goals, like a vacation, wedding or holiday gifts would come out of your “wants.”

Step 4: Adjust as needed

Ideally, your income should cover your needs, wants and savings goals. But if money feels tight, there are ways to adjust. You could try focusing on one savings goal at a time, cut back on spending in your "wants" category, or try both. Another option is to boost your income with a side job.

Pros and cons of paying yourself first

Pros

Low maintenance compared with other methods like zero-based budgeting (where you have to track every expense).

Helps you focus on big-picture goals and avoid impulse spending.

Easy to automate. Use payroll deductions for retirement accounts or set up automatic transfers to savings/IRAs.

Cons

May not be the best choice if you have high-interest debt.

Savings could take priority over more urgent financial needs, like paying down debt.

Paying yourself first could leave you short on bills if you don’t plan carefully.

Ready, set, save

Paying yourself first is a great option if you prefer a hands-off budgeting system or don't want to feel as though you’re budgeting at all. Remember to automate your savings for an easier experience.

If you need more structure, consider a more involved budgeting method:

- Envelope system portions out your entire income in cash toward all of your expenses at once using individual envelopes labeled for every item in your budget.

- Zero-based budgeting gives every dollar a job, such as paying bills, saving or spending, until there's nothing left unassigned.

There are also a variety of budget apps that allow for customization, track monthly spending and even cater to couples.