The zero-based budgeting method, also known as the ZBB budget, encourages you to use every penny of your monthly income. But that doesn’t mean spending it on a shopping spree. Important goals, such as saving money and paying off debt — as well as spending on fun stuff — are all part of the plan.

The idea behind the zero-based budget, sometimes also called the zero-sum budget, is to give every cent a purpose.

What is zero-based budgeting?

Zero-based budgeting is a method that has you allocate all of your money to expenses for needs and wants, as well as short- and long-term savings and debt payments. The goal is that your income minus your expenditures equals zero by the end of the month.

The difference between zero-based budgeting and living paycheck to paycheck is that all of your financial needs are met. You can repeat expense categories and amounts every month, or mix it up.

If you come in under budget in a certain category at the end of the month, add the remaining amount to next month’s budget, or move it to another category, such as your emergency fund.

It’s the same concept as the envelope system, which involves distributing money for different expense categories into envelopes.

How to start a zero-based budget

Before implementing this budget, take a few steps to ensure you're realistically planning your spending:

- Know your income. Total your paycheck, benefits and other sources of monthly income to find out how much money you have to work with.

- Track your expenses for a few months. Knowing what you typically spend — and on what — creates a framework you can use going forward. You’ll spot areas in which you can cut back and in which you want to allocate more.

- Categorize your expenses. Identify all of your priorities and expenses, including your needs and wants, emergency fund and other savings goals, plus your debt repayments.

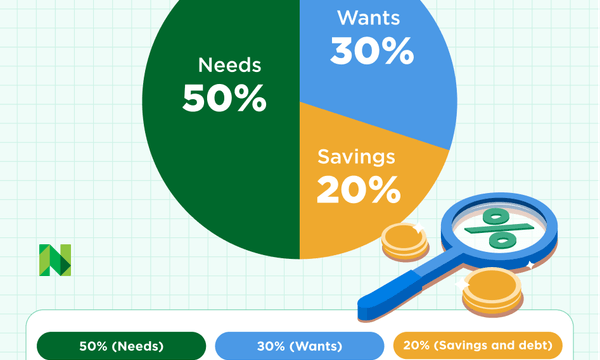

How much should you allocate to each category? NerdWallet recommends the 50/30/20 rule. With this approach, 50% of your income goes to needs, 30% to wants, and 20% toward debt repayment and savings.

Zero-based budgeting example

Let’s say you make $3,000 per month. Your budget might look like this:

Note that once you've budgeted for the essentials, the other spending categories can be for anything else. Want to pay off a credit card in six months? Build it into your budget. Buy a house? Set aside money for the down payment. Big vacation? Pad that travel fund with a few more bucks. Build your ZBB budget with an app — such as YNAB or Goodbudget — a spreadsheet, or pen and paper.

» MORE: Explore our roundup of best budget apps for 2025

Meet MoneyNerd, your weekly news decoder

So much news. So little time. NerdWallet's new weekly newsletter makes sense of the headlines that affect your wallet.

The pros and cons of zero-based budgeting

The pros

The zero-based budget keeps you aware of how much money flows in and out. This can prevent you from spending what you don’t have.

“If you haven’t tracked where your money is going, or if you feel like you don’t have control of your money or spending, then I think that this is a really good method,” says Catherine Hawley, a certified financial planner in Monterey, California.

This system is also customizable, which can be especially useful if you're new to managing your money.

The cons

Following a zero-based budget eats up quite a bit of time. To hold yourself accountable, you’ll have to closely and consistently monitor your spending. And that’s not the only challenge you may experience.

“I think one thing that can be problematic with it is that there are a lot of variable expenses,” Hawley says. “If you don’t account for your irregular expenses, the zero budget is going to potentially not leave you with enough money on average.”

These variable expenses might include holiday purchases, traveling to a friend’s wedding or replacing a broken phone.

But there’s a way to solve this: Set aside money specifically for these costs. Create a savings fund, separate from your emergency fund and other savings goal funds, and contribute to it each month.

The zero-based budgeting method might also pose a problem if you have an irregular or unpredictable income, for example if you’re a freelancer or an hourly worker whose schedule fluctuates.

If you don't always know how much money you’ll have to allocate, consider using the previous month’s income for the current month’s budget. Note that you’ll need to save up a month’s worth of income as a buffer first.

See if zero-based budgeting is right for you

Now that you know what the zero-based budgeting system is all about, you’re ready to give it a shot. If it doesn’t work for you, try another budgeting method. If your financial situation is complex, you might benefit from speaking to a financial advisor.

Watch this video to learn about other budgeting methods that may better align with your personality and lifestyle.