Using a secured credit card is perhaps the quickest and easiest way to build credit — as long as you're smart about how you use it.

Secured cards are different from regular credit cards in one key way: They require a cash security deposit, which the credit card company holds onto just in case the cardholder doesn't pay the bill. The deposit reduces the risk to the card issuer, so secured cards are easier to qualify for. And that makes secured cards an ideal tool for people looking to improve their credit.

Here’s how to use a secured credit card to build credit.

1. Choose the right secured card

A secured credit card isn't a long-term commitment. Get it, use it to improve your credit enough to qualify for better options, and then move up to an unsecured card (and get your deposit back). Among factors to consider:

- Credit bureau reporting. The whole point of getting a secured card is to build credit, and that can happen only if the card issuer reports your account activity to the credit bureaus — the companies that compile the credit reports that form the basis of credit scores. If a card doesn't report to the bureaus, it's not worth getting.

- A deposit you can afford. Most secured cards have a minimum security deposit of $200 or $300, but some require as much as $500. A few don't have a set minimum, but your card is secured by the balance in a linked bank account.

- Reasonable fees. Some cards designed for people with bad credit (or no credit) come with outrageous fees — annual fees of $99, monthly maintenance fees and so on. There are numerous options at $0, or at least less than $50.

- A path to an upgrade. Ideally, you'll be able to move up to an unsecured card from the same issuer and get your deposit back without having to close the account.

Some secured cards offer rewards and maybe even a few perks, but don't focus too much on those. The generally low credit limits on secured cards make it hard to rack up significant rewards, and, ideally, you won't be using the card very long anyway.

2. Pay the deposit quickly

Many people who apply for and are approved for a secured credit card end up losing it before they even get it. That's because they didn't provide the security deposit. In most cases, the card issuer won't actually open the secured card account until you pay the deposit — and you usually have to do so within a certain time frame.

Losing a card because you neglected to pay the deposit can be harmful to your credit at the exact time you're trying to build it. The application itself will likely shave some points off your score. If you get a card, those lost points are worth it because now you have a credit-building tool. But if you don't even get the card, all you have is the downside.

Pulling together the $200 to $300 necessary for a secured card deposit can be difficult for many people. If you think it'll take some time, save up the deposit before applying for the card, so you can fund the deposit quickly.

Trying to get approved for a card?

Create a NerdWallet account for insight on your credit score and personalized recommendations for the right card for you.

3. Use the card — but use it wisely

Your credit score essentially measures one thing: how risky it is to lend you money. The higher the risk, the lower your score. Improving your credit means demonstrating that you can handle borrowed money responsibly. And that means using your secured card — buying things with it, and then paying it off.

Use the card at least once a month so that your account shows regular activity. But don't max out the card. Use it for smaller purchases that keep you well below your credit limit. A big part of your credit score is determined by "credit utilization," or the amount of your available credit you're using.

That doesn't leave a lot of room for big purchases, but remember that the primary purpose of a secured card is to build your credit, not to bolster your purchasing power.

4. Pay on time and in full

Although this is Step 4 on our list, it's No. 1 in terms of sheer importance for credit building. The single biggest factor in your credit score is your payment history. If you can't pay your bills on time every month, you're just not going to build good credit. So when your credit card bill comes, pay it ASAP. Set up automatic payments if that helps.

To keep your account in good standing, you have to pay at least the minimum payment amount by the due date. But you're better off paying the entire balance in full. Secured credit cards tend to charge extra-high interest rates, usually well above 20%, so carrying a balance from month to month will be costly. If you're using the card as directed — making only small purchases — paying in full shouldn't be too difficult.

5. Monitor your credit score

As you use your secured card to establish a positive credit history, you'll want to keep an eye on your credit score. You can get your score for free through NerdWallet.

If you're seeing progress, it's a sign that your effort is paying off. That's a good feeling! As your credit improves, you may become eligible to apply for a regular unsecured card.

If you're not seeing progress, however, it could point to other problems with your credit history. Get your credit report — you're entitled to free reports from the three major credit bureaus — and check it for errors or other problems.

6. Upgrade to an unsecured card

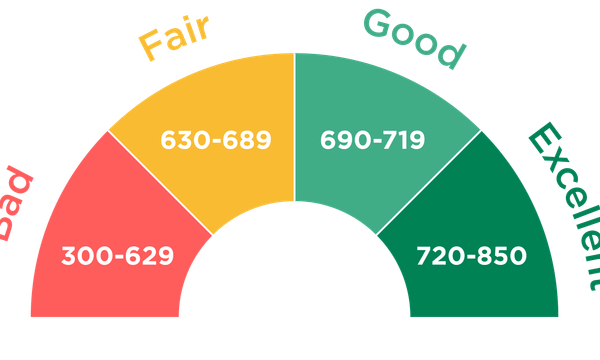

Once you’ve been using your secured credit card carefully for some time, you might move into "fair" credit territory, also called "average" credit. This is generally considered to be a score above 630. At that point, you have a good chance of qualifying for an unsecured credit card. The issuer of your secured card might agree to convert it to a regular credit card, or you can apply for a credit card for fair credit. When you close or convert a secured card, you should get your security deposit back.

The habits you formed while you had a secured card will serve you well with an unsecured card, too. Keep on using your card regularly, maintain a low credit utilization and pay at least the minimum by the due date every month, and your credit will continue to get healthier.