Money drives many decisions that we make day to day. Setting goals can help us feel more confident that the decisions we're making will take us where we want to go.

Ready to get started? First, learn what financial goals are and why they’re important.

What are financial goals?

Financial goals are the personal, big-picture objectives you set for how you’ll save and spend money. They can be things you hope to achieve in the short term or further down the road. Either way, it’s often easier to reach your goals if you name them early on.

» Get started: Learn how to set and reach financial goals

Financial goals examples

Think about what’s important to you as you begin to set goals. It’s normal to have several goals, and for them to change over time.

Examples of financial goals include:

- Paying off debt.

- Building credit.

- Saving for retirement.

- Building an emergency fund.

- Buying a home.

- Saving for a vacation.

- Starting a business.

- Feeling financially secure.

NerdWallet's 2026 Consumer Outlook Report dug into some financial goals for 2026.

One in 5 Americans (20%) say they plan to invest in cryptocurrency in 2026, and 18% plan to invest in AI-related stocks or funds. Some Americans plan to start a business (18%) or buy a new home (17%) in 2026.

Your goals may depend on whether you're managing money on your own or working with a partner.

» MORE: Read the full Consumer Outlook Report

Why do financial goals matter?

Having goals can help you understand the actions you need to take to improve your financial situation or reach the lifestyle you want.

For example, say your goal is to pay off a credit card bill.

You might cut back on takeout dinners and use the money you save to make extra payments instead. Without establishing that goal, you’re more likely to continue spending as usual while your debt piles up.

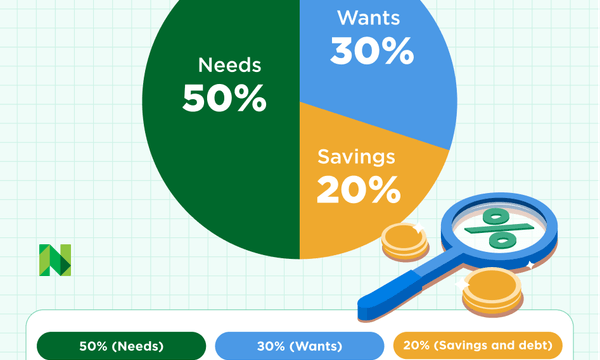

Like all expenses, financial goals should be included in your budget. That way, you can take concrete steps toward reaching them while leaving room for other costs. Plan out how much time it will take to reach each goal and how much money you’ll need to contribute within that period.

Identifying goals and creating a realistic plan for them allows you to track progress and can motivate you to keep going.

Employed Americans who have a savings goal are more likely to regularly save a portion of their income than those who don’t — 75% versus 62%, respectively — according to a NerdWallet survey.

Even if you fall short, you might develop some healthy money habits along the way.

Meet MoneyNerd, your weekly news decoder

So much news. So little time. NerdWallet's new weekly newsletter makes sense of the headlines that affect your wallet.