If you’ve ever felt like your money disappears before you know where it went, a budget can help you get a handle on it.

But that doesn’t mean you need a complicated system or a color-coded spreadsheet — some people prefer pen and paper, while others rely on budget apps to track their spending.

There’s no one-size-fits-all approach. The key is choosing a method that works for your life and sticking with it.

5 steps for making your own budget

- Figure out your take-home pay (income after taxes and deductions like healthcare premiums and retirement savings).

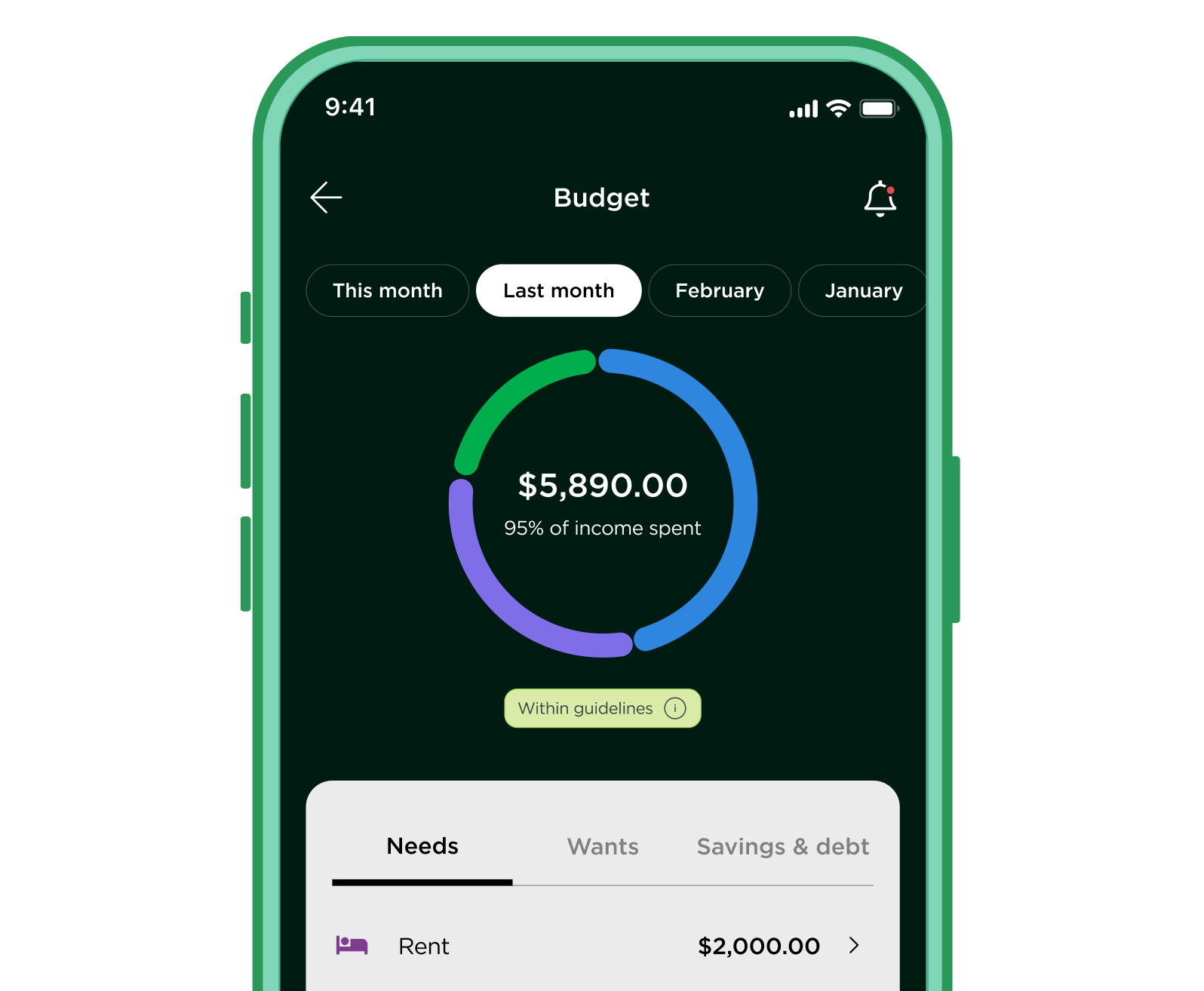

- Track your expenses for a month. Keep track of everything you buy and categorize it into needs, wants and savings/debt.

- Choose a budgeting method. There are tons of great options, but the 50/30/20 is one place to start.

- Compare your spending with your method’s suggested categories. If your “wants” exceed 30% of your budget, for example, then shift money and priorities to meet your goals next month.

- Review your budget regularly. Take a look at your spending and see how it’s stacking up to your budgeting categories weekly. This can help you correct your behavior if you’re not meeting your goals. Monthly reviews help you see what’s working and what’s not and make changes for the next month.

Meet MoneyNerd, your weekly news decoder

So much news. So little time. NerdWallet's new weekly newsletter makes sense of the headlines that affect your wallet.

Budgeting methods: How to choose the right one for you

When it comes to budgeting, there’s no one-size-fits-all method. The right approach depends on your income, goals and spending habits. Here are a few popular options to consider:

50/30/20 budget

Split your take home pay into three buckets — 50% for needs (like housing and groceries), 30% for wants (like dining out and entertainment) and 20% for savings and extra debt payments.

✅ Best for people who want a simple framework that balances spending and saving without tracking every dollar. Works well for people with steady income and predictable expenses.

»Try our 50/30/20 calculator to see if this budget is right for you

60/30/10 budget

A variation that puts 60% toward needs, 30% toward wants and 10% toward savings or debt — a good option if saving 20% feels out of reach right now.

✅ Great for people who live in a high-cost of living area or a big line item in their budget like child care.

Envelope method

Set spending limits for categories (like groceries or shopping) and use cash — or digital equivalents — to stick to those limits. When the “envelope” is empty, you stop spending.

✅ A good option for people who tend to overspend and want clear limits, especially those who benefit from a hands-on, visual way to see exactly how much is left in each category.

Zero-based budgeting

Assign every dollar a job so your income minus expenses equals zero. This method is more hands-on and helps you track exactly where your money goes each month.

✅ Best for detail-oriented planners who want full control over their money and like tracking every dollar to see exactly where it’s going each month.

Did you know...

Saving is a regular habit for many Americans: 66% of employed workers say they save monthly in a bank account, and 44% say they put away at least 20% of their take-home pay, according to a NerdWallet survey.Why is budgeting important?

Budgeting encourages you to put your money to work in the best way possible and can help you identify overspending. Think of a budget as a next step toward reaching your financial goals. It can help you:

👀 See where your money is going

Budgets show your income and how much you're spending in various areas of your life. Tracking expenses can help you spot patterns in your spending. From there, you can identify where to make adjustments, if needed.

For example, maybe your budget shows that you spend less than you earn, but you’re paying for subscriptions or services you no longer need. Cutting those "wants" can free up money so you can more easily meet monthly needs, invest in your future and more quickly pay down debt..

📅 Plan for upcoming expenses

Budgets can also help you plan for how you’ll cover upcoming expenses, including rent, car payments or holiday spending. Mapping out expenses in advance can help reduce the risk of overspending.

Savings buckets, or sinking funds, can help spread out the costs over time. For example, you could put $100 into a vacation fund and $50 into a holiday gift fund each month. When it’s time to book that flight or buy presents, you’ll have the cash ready.

» Have a big expense on the horizon? Set up a sinking fund now

💰 Save for the future

A good budget encourages you to set aside money for an emergency fund and savings goals, like a vacation or retirement. Budgets can also help you plan for larger purchases, like saving money every month for a car or a downpayment on a house.

“Start small and start now,” Dasha Kennedy, author and financial influencer, said in an interview. “I don’t care if it’s $10 a week. Consistency matters more than the amount.”

» Ready for a financial glow up? Here are Dasha Kennedy’s tips for living well within your means.

💳 Manage debt

Here’s how a budget can help you manage debt:

- Budgets create awareness about where your money is going so you can cut back on unnecessary spending and redirect it toward high-interest debt first.

- Budgets help you prioritize debt repayment. You can make sure your minimum payments are covered and decide how much extra you can afford to put toward your debt. The extra is what helps speed up the repayment process and reduces interest over time.

- Budgets keep you consistent. Regular debt payments keep you motivated and prevent missed payments.

- Budgets prevent you from taking on more debt. When you’re tracking spending and setting limits, you’re less likely to rely on credit cards to cover necessary costs.

😵💫 Relieve stress

Budgeting can help you feel more prepared for the challenges life brings. Having a clear picture of your finances can help reduce the stress of uncertainty, and make it easier to plan.

A good budget can help you get through seasons where spending is higher — like around the holidays or during the summer, when travel is at a premium or summer camps are needed — with smart planning and preparation.

» Ready to get started? Read our 5-step guide to how to budget

Your budget builds itself, instantly