You have reached the most recent version of this annual NerdWallet report. Previous years’ reports are available at the bottom of this page.

As of the date of publication, a partial government shutdown is impacting the Transportation Security Administration (TSA). TSA agents are essential employees who are expected to work during this time, but they aren't getting paid until the shutdown ends, which could lead to staffing shortages as TSA agents call out sick at higher rates. For you, this could mean longer queues at the airport – check your airport's website for expected wait times and arrive early to avoid missing your flight.

Spring has sprung, and many Americans have plans to get out of town for an upcoming summer vacation. But debt may be putting a damper on making sun-soaked memories.

Nearly half of Americans (45%) plan to take a vacation in summer 2026 that requires a flight and/or paid lodging, like a hotel or vacation rental stay, according to NerdWallet’s annual summer travel survey. They expect to spend $3,940, on average, for these summer travel costs. That’s more than 120 million travelers spending over $475 billion on flights and lodging.

The survey, conducted online by The Harris Poll, asked over 2,000 Americans if they’re traveling this summer and, if so, how much they’re spending on airfare and lodging. We asked these 2026 summer travelers — defined as Americans who plan to take a vacation that requires a flight and/or paid lodging between June and August 2026 — how they plan to pay for these expenses and what steps they’ll take to save on summer trip costs. We also asked those who traveled last summer about their lingering credit card balances.

Key findings

- Most 2025 summer travelers who paid for their travel with a credit card (74%) didn’t pay it off right away. In fact, more than a third of those who charged last year’s vacation (35%) still haven’t paid off the balances.

- The vast majority of 2026 summer travelers (89%) will take action to save money on their vacation. But a majority of Americans overall say it’s worth paying extra to buy refundable flights (67%) and travel insurance (62%) for the flexibility.

- Over 2 in 5 Americans (42%) say they’d rather skip a vacation altogether than book budget airfare and lodging.

- While about a third of 2026 summer travelers (32%) plan to use credit card points or miles to cover travel expenses in order to save money, close to half of Americans overall (48%) say travel points and miles programs are too complicated.

“For many travelers, vacation math can hit differently,” says Sally French, a NerdWallet travel expert and co-host of Smart Travel Podcast. “In the moment, it might just be $200 more for an ocean view or $40 extra for that seat upgrade, but multiplied across all the meals, tours and transit over a week or two, and your vacation budget can easily balloon. The trick is planning a trip that feels meaningful — without the debt.”

Subscribe to our free TravelNerd newsletter for inspiration, tips and money-saving strategies, delivered straight to your inbox.

By signing up, you will receive newsletters and promotional content and agree to our Terms of Use and acknowledge the data practices in our Privacy Policy. You may unsubscribe at any time.

Summer travel debt lingers from 2025 for some

Last year’s summer vacation may be memorable for all the wrong reasons. According to the survey, just over a quarter of 2025 summer travelers who put their travel expenses on a credit card (26%) paid off that balance with the first statement. It’s likely that the remaining 74% incurred or are still incurring interest on their vacation.

Over a third of 2025 summer travelers who charged their travel expenses (35%) still haven’t paid the balances off. And some may be adding to their debt this summer.

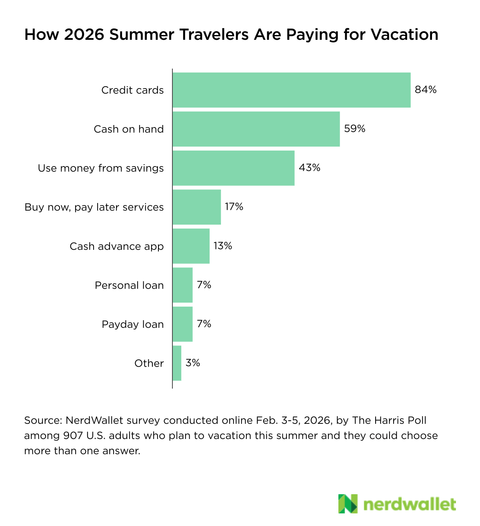

The survey found the majority of 2026 summer travelers (84%) will use credit cards to pay for at least some of their vacation travel expenses, making cards the most popular payment method for these costs, by far. Additionally, 59% of summer travelers will use cash on hand — or money in their checking account — and 43% will use money from savings.

Not all Americans who plan to use credit cards for their upcoming trip will rack up interest charges. Nearly two-thirds of 2026 summer travelers (61%) say they’ll use a credit card for travel expenses and pay it off with the first statement. But nearly a quarter (23%) say they’ll charge summer travel expenses on their credit card and won’t pay them off right away.

Credit cards aren’t the only potential debt vehicle Americans are using for their upcoming trips. About one-sixth of 2026 summer travelers (17%) say they’ll pay travel expenses with buy now, pay later services, and others will opt for cash advances (13%) and payday loans (7%).

Going into debt for summer vacation can make this time of supposed rest and relaxation a source of financial stress. But often, you can avoid debt for nonessential trips by keeping travel costs as low as possible.

About 9 in 10 summer travelers will take action to save on trips

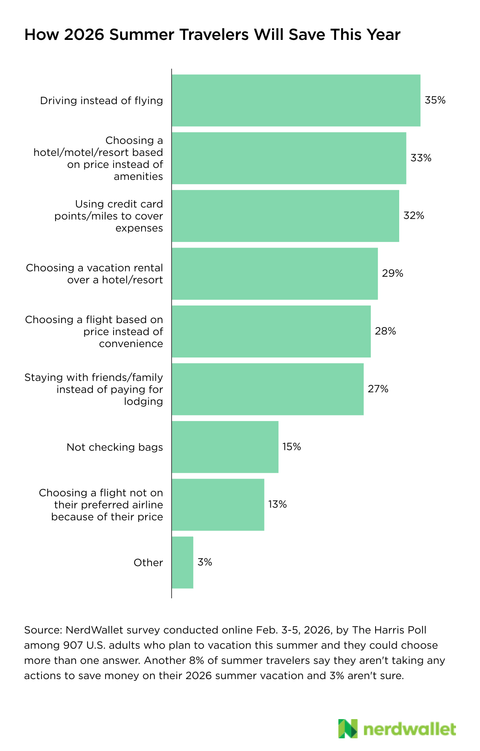

Flights and lodging can be pricey, but there are plenty of ways to keep expenses down. According to the survey, a majority of 2026 summer travelers (89%) are taking action to save money on their travel costs. Some of the cost-saving strategies include driving instead of flying (35%) and choosing lodging based on price instead of amenities (33%).

On the flip side, something many may be willing to pony up for is flexibility. The survey found that around two-thirds of Americans (67%) say paying extra for refundable flights is worth it for the flexibility, and 62% say the same about travel insurance.

“Flexibility is key with travel — particularly if you’re booking a hurricane-season beach trip, traveling with kids, or juggling a complicated trip where one missed connection could derail your itinerary,” French says. “Especially in those cases, paying extra for refundable fares or travel insurance can be a smart hedge. Think of it as buying yourself options.

“Then again, if you’re taking a quick, low-cost domestic trip that could be rebooked out of pocket, you might be better off skipping that expense and saving the money for souvenirs.”

42% would skip vacation rather than book budget travel

Not everyone is willing to travel on the cheap. According to the survey, more than 2 in 5 Americans (42%) say they’d rather skip a vacation altogether than book budget airfare and lodging. Interestingly, this sentiment is truer for younger Americans than their older counterparts — 50% of Gen Zers (ages 18-29) and 47% of millennials (ages 30-45) would rather skip a vacation than book budget, compared to 38% of Gen Xers (ages 46-61) and 36% of baby boomers (ages 62-80).

While budget airfare and lodging can save cash, there are plenty of other ways to cut costs. Whether that’s booking midtier accommodations instead of swankier options, flying early in the morning or late in the evening, or opting for a road trip, you can keep expenses down by compromising on things that aren’t a priority.

About half of Americans say rewards programs are too complicated

Nearly a third of 2026 summer travelers (32%) plan to use credit card points or miles to cover travel expenses to save money. Travel rewards programs can be a great way to earn free or reduced-cost flights or lodging. But some may be shying away from using them because they can be challenging to navigate.

Around half of Americans (48%) say travel points and miles programs are too complicated. Gen Zers are more likely to say this than older generations — 56% vs. 47% of millennials, 46% of Gen Xers and 45% of baby boomers.

Travel points programs can be complicated, but oftentimes, they’re only as complicated as you make them. Sure, you might get the most value out of points or miles by painstakingly learning and applying all the ins and outs of travel hacking, but you can also settle for good enough and still end up with free or cheap travel.

Play the points game on easy mode by using travel rewards in straightforward ways, like booking a flight directly with the airline, or using your travel credit cards’ redemption portal to book accommodations. When you’re ready to level up, read up on how to travel with points and miles to demystify the process so you aren’t missing out on potential savings for future vacations.

What summer travelers can do

Pay down last year’s debt, avoid debt on this year’s summer travel

Interest charges from carrying credit card debt can significantly increase your summer vacation expenses. This is particularly true if you’re still in debt from last year when planning this year’s trip. Cards assessing interest carried an average interest rate of 22.3%, as of November 2025, according to the Federal Reserve Bank of St. Louis. Before booking anything, make a plan to pay off last year’s credit card debt and consider setting limits on future spending.

Decide which travel expenses are most important

Most of us are constrained by some sort of budget when traveling, which means making some trade-offs. Think about what you’re willing to spend more on — perhaps a more convenient flight time for a family trip, so your kids aren’t completely exhausted — and where you can save to make up for it, like opting for a hotel with a good price but fewer amenities. Splurge where it matters, save where it doesn’t.

Use credit card points or miles

If you have a pile of points or miles you’re saving up, reconsider your strategy. Over time, travel rewards can lose value, so points might not be worth as much next summer as they are now. Unless you’re planning on redeeming those points for a specific trip in the near future, we recommend using rewards sooner rather than later.

“Travel doesn’t have to be luxury to be impactful — and no vacation should follow you home as credit card debt. Before committing to any reservations, decide what actually matters to you,” French says. “Maybe that five-star hotel or fancy meal will make your trip that much better. But could you also have a great trip exploring a new city on your own while sampling local food from roadside stands?

“Remember that the goal of travel is the memories — and not the kind of memories you get every month when you’re still making minimum payments a year from now.”

Cite as NerdWallet (2026). “2026 Summer Travel Report: 42% Would Rather Stay Home Than Book Budget Travel.” Retrieved from https://www.nerdwallet.com/travel/studies/summer-travel-report

Methodology

This survey was conducted online by The Harris Poll on behalf of NerdWallet from Feb. 3-5, 2026, among 2,082 U.S. adults ages 18 and older, among whom 907 plan to take a vacation this summer that requires a flight and/or paid lodging. The sampling precision of Harris online polls is measured by using a Bayesian credible interval. For this study, the sample data is accurate to within +/- 2.7 percentage points using a 95% confidence level. This credible interval will be wider among subsets of the surveyed population of interest. For complete survey methodology, including weighting variables and subgroup sample sizes, please contact [email protected].

Summer travel is defined as June, July and August 2026, for the purposes of this survey.

Disclaimer

NerdWallet disclaims, expressly and impliedly, all warranties of any kind, including those of merchantability and fitness for a particular purpose or whether the article’s information is accurate, reliable or free of errors. Use or reliance on this information is at your own risk, and its completeness and accuracy are not guaranteed. The contents in this article should not be relied upon or associated with the future performance of NerdWallet or any of its affiliates or subsidiaries. Statements that are not historical facts are forward-looking statements that involve risks and uncertainties as indicated by words such as “believes,” “expects,” “estimates,” “may,” “will,” “should” or “anticipates” or similar expressions. These forward-looking statements may materially differ from NerdWallet’s presentation of information to analysts and its actual operational and financial results.

Explore more on