Homeowners insurance offers financial protection for what may be your most valuable asset — your home. However, shopping for home insurance is often treated as an afterthought instead of an important decision in its own right. That can leave homeowners vulnerable to financial ruin should disaster strike.

This guide will help you understand what you need to know when shopping for home insurance so you can make the best choice for your needs.

We encourage you to shop for home insurance once a year to make sure you're getting the best coverage and price. By getting at least three quotes as part of the shopping process, you can be confident you're getting the best deal available on the coverage you need.

Get personalized quotes without the work

Let NerdWallet Insurance Experts compare quotes from popular carriers to find the right insurance coverage and rate for you. No guesswork — just expert, personalized help.

Get my quotes

NerdWallet Insurance Experts, LLC is a wholly owned subsidiary of NerdWallet.

Insurance Services offered through NerdWallet Insurance Experts, LLC (AZ resident license no. 3003649891).

How to shop for homeowners insurance

1. Decide how much coverage you need

Your first step in shopping for homeowners insurance is to figure out how much you need. If you don’t buy enough coverage, you run the risk of being underinsured. That could mean you won’t receive enough money from your insurance company to rebuild after a total loss.

Before getting quotes, it helps to understand what kinds of coverage are included in a policy. Standard home insurance policies typically include six types of coverage:

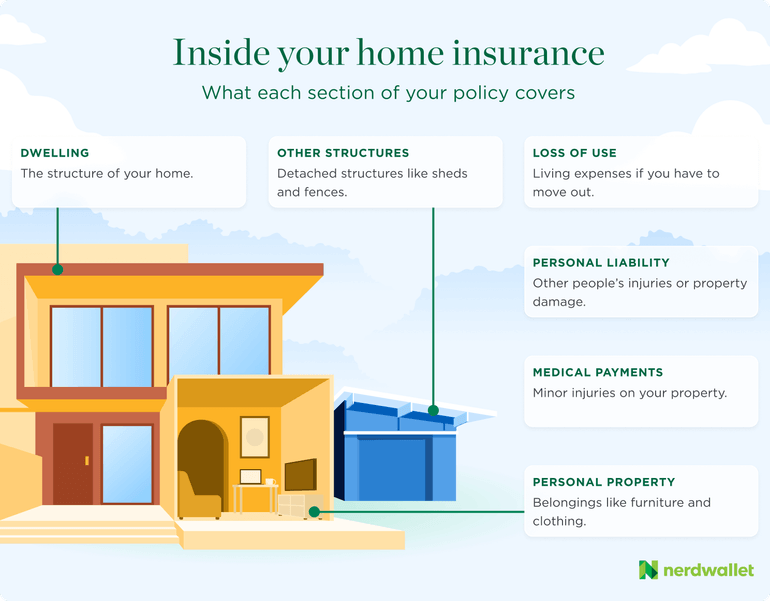

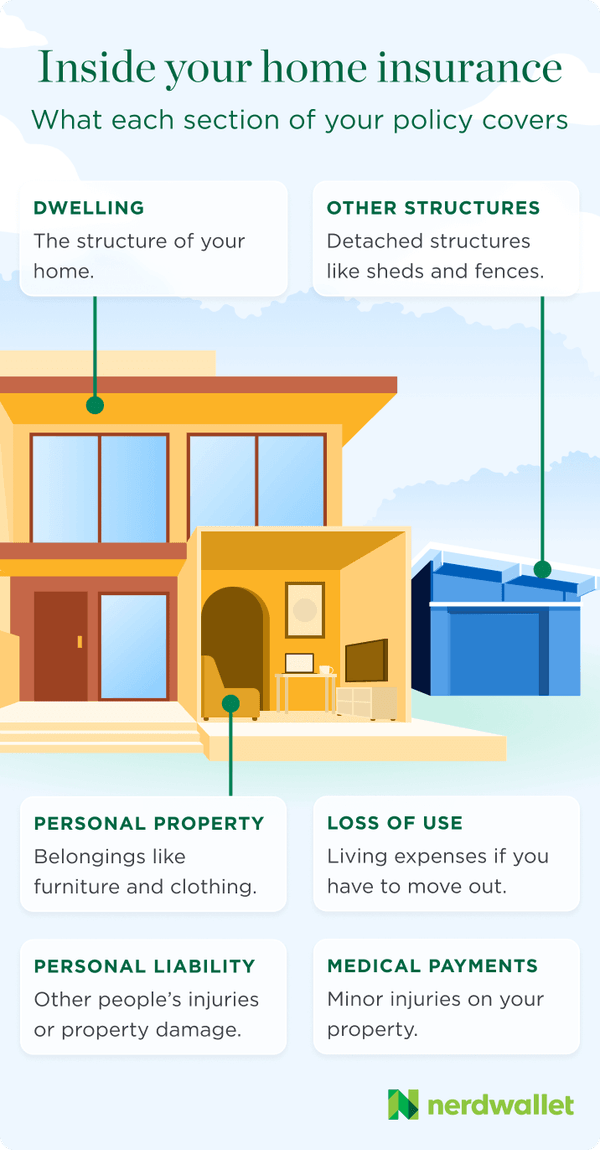

Dwelling coverage

Dwelling coverage covers the structure of your home, such as the walls, floors and roof. It can also apply to built-in appliances and attached structures like a garage, porch or deck. If your home is damaged for a reason covered by your policy, you’ll pay your deductible and the insurer pays the rest up to your dwelling coverage limit.

At a minimum, you’ll want enough coverage to fully rebuild your home. This is known as replacement cost coverage and reflects the size of your house, its features and the cost of building in your area. Your insurance company should be able to help you determine this amount.

Because of inflation and rising building costs, consider extended replacement cost coverage. This pays an additional percentage over your dwelling limit, usually 10% to 50%. Some insurers also offer guaranteed replacement cost coverage, which covers the full cost of rebuilding your home after a covered loss, no matter how high.

Personal property coverage

Personal property coverage covers the contents of your home if they’re stolen, damaged or destroyed due to a covered event. This can include furniture, clothing and electronics, among other things.

Personal property coverage usually pays 50% to 70% of your dwelling coverage limit. Make a home inventory to get a sense for whether this amount is enough.

Many home insurance policies cover personal property on an actual cash value basis. This means you’ll get enough money to cover the value of your property at the time of the loss. You typically won’t receive enough to buy brand-new replacements. To avoid this, look into upgrading to replacement cost coverage for your belongings.

Other structures coverage

Other structures coverage insures the structures on your property that aren’t attached to your house. This could be a fence, gazebo or detached garage. The policy limit for other structures coverage is normally 10% of your dwelling coverage limit.

Loss of use coverage

Loss of use coverage pays for additional living expenses, up to your limit, if you’re unable to live in your home due to a covered event, like a fire or tornado. These expenses can include hotel bills, groceries and laundry costs.

Personal liability coverage

Personal liability coverage kicks in if you’re held legally responsible for causing bodily injury or property damage to someone else. For example, say your dog bites someone while you’re out hiking. Liability coverage can help pay for legal expenses, medical bills and other damages, up to your coverage limit.

🤓Nerdy Tip

You’ll want to make sure you have enough personal liability coverage to protect your assets, which means calculating your net worth.Medical payments coverage

Medical payments coverage covers medical expenses for guests who are injured on your property, regardless of who’s at fault. It can help pay for medical bills, ambulance fees and other related expenses.

2. Evaluate add-ons and endorsements

Add-ons and endorsements can provide coverage beyond what's in a standard home insurance policy. They’re designed to fill gaps in coverage for specific types of damage or losses.

You may want to consider these common add-ons:

Inflation guard

Inflation guard automatically raises your coverage limits annually to keep up with rising costs. Some insurers include this feature as part of a standard homeowners policy.

Scheduled personal property

Scheduled personal property provides extra coverage for high-value items like jewelry, art and electronics that may exceed your standard policy limits.

Sewer or water backup coverage

Sewer or water backup coverage is for damage caused by water backing up into your home through pipes or drains, or because of a sump pump failure.

Ordinance or law coverage

Ordinance or law coverage pays to bring your home up to current building codes during repairs or rebuilding after a covered loss.

Equipment breakdown coverage

Equipment breakdown coverage is for sudden and accidental breakdowns of HVAC systems and large appliances. This coverage applies when, for example, the compressor stops working in your fridge.

Service line coverage

Service line coverage pays for damage to water, electric or other utility lines that you’re responsible for.

Home business endorsements

Home business endorsements provide extra coverage for home-based businesses beyond standard home insurance.

3. Consider insurance for flooding and earthquakes

Most home insurance policies won’t cover damage from floods or earthquakes. You'll need to purchase separate policies to handle these risks.

Flood insurance 🌊

What it covers: Flood insurance covers damage caused by flooding. This includes scenarios such as a river overflowing its banks, a hurricane storm surge, a heavy downpour or flooding caused by snowmelt.

Who needs it: Homeowners in high-risk areas or flood zones.

How to get it: Flood insurance is available through the National Flood Insurance Program (NFIP) and private insurers. Here’s how to find the best flood insurance.

Earthquake insurance 🫨

What it covers: Earthquake insurance is for damage caused by earthquakes and other earth movement.

Who needs it: Homeowners in some western states and along major fault lines. In California, home insurance companies are required to sell earthquake insurance.

How to get it: You may be able to buy a standalone earthquake insurance policy or add coverage as an endorsement. If you have difficulty finding earthquake insurance, contact an independent insurance agent.

4. Decide your deductible

When you get quotes, you’ll usually have the option to choose your home insurance deductible. This is the amount of a claim you’re responsible for paying before your insurance kicks in.

Raising your deductible from $1,000 to $2,500 could save you an average of 9%, according to NerdWallet’s rate analysis. However, before you choose a higher deductible, make sure that you can cover that amount should you have to file a claim.

Did you know...

Your home insurance policy may have special deductibles for damage from hurricanes, windstorms or other events. These deductibles are often a percentage of your dwelling coverage and may be much higher than your main deductible. Read your policy carefully to ensure you understand when these deductibles may apply.5. Get quotes from at least three companies

You can get quotes online, call companies directly, or work with an independent insurance agent who shops around on your behalf. You’ll typically need to have this information on hand to get a quote:

Your insurance history.

Your insurance history, including past claims, the name of your most recent insurer and your last date of coverage.

Who lives with you.

Personal information for anyone living in your house.

How your house is used.

You’ll be asked to identify the type of residency (primary home, secondary, etc.) and whether you conduct any business on your property.

Facts about your home.

Be prepared with the square footage of your home, the year it was built and the type of construction (wood, brick, etc.) Note any recent home renovations and the number of stories, bedrooms, bathrooms and detached structures.

Any special features.

Any security features, such as a burglar alarm, smoke detectors or deadbolts.

When you get quotes, make sure you're comparing similar coverage limits and deductibles. You might not get the same coverage limits or deductible options with every company. However, try to match them as closely as you can to ensure you’re not sacrificing coverage for a lower premium.

Note that quotes are estimates, and they may not exactly match the price you end up paying for coverage.

For a more detailed look at what’s involved with this process, read our guide to home insurance quotes.

Find the best homeowners insurance in your state

6. Buy your home insurance policy and read it closely

Once you’ve compared quotes and picked a policy, it's time to finalize the details. Sign the paperwork to lock in your policy, and make your first payment. If you’re in the process of buying a house, your first payment may be rolled into your closing costs.

After you sign the contract, you’ll receive a home insurance declarations page from your insurer. This one- to two-page document lays out the most important information about your policy. It usually includes how much your policy costs, what it covers and its start and end dates.

🤓Nerdy Tip

Be as accurate as possible when giving your information to insurance companies. If you misrepresent your home or your belongings to get a lower premium, you may be denied coverage or even charged with fraud.We recommend reading your home insurance policy in its entirety, as it will lay out the details of what your policy does and does not cover. Understanding the limits of your coverage will help you avoid unwanted surprises later. Keep a copy of your policy in a safe place so you can refer to it if you need to file a claim.

Best home insurance companies

We evaluated dozens of carriers to find the best homeowners insurance companies. These insurers received our highest star ratings based on their coverage options, consumer experience and financial strength.

Company | NerdWallet star rating | Why we picked it |

|---|---|---|

Best for high-value homes | ||

Best regional insurer | ||

Best coverage | ||

Best for consumer satisfaction | ||

Best for sustainability | ||

Best for discounts | ||

Best big national insurer | ||

USAA* | Best for military and veterans | |

*USAA membership is open only to active military, veterans, some federal employees and their families. | ||

Frequently Asked Questions

What is the 80% rule in homeowners insurance?

The 80% rule is also called the 80/20 rule. It refers to when insurers require homeowners to have coverage for 80% of the home's replacement value in order to be fully covered. That means homeowners could be required to pay as much as 20% of costs after a covered loss out-of-pocket.

How can I pick a good homeowners insurance company?

One of the first steps to choosing a home insurer is to look for one that’s known for customer satisfaction. For insight, see home insurance studies from JD Power, a firm that surveys thousands of homeowners every year. You can also check with the National Association of Insurance Commissioners (NAIC) to see how many complaints were filed with state regulators against an insurer.

How much does homeowners insurance cost?

Before you start shopping for a policy, it’s important to know how much you might pay for home insurance so you can compare quotes. A NerdWallet analysis shows home insurance costs an average of $2,490 a year, or about $208 a month. But this can vary widely from state to state. It can also be more or less expensive depending on the home you have and personal factors such as your credit score and claims history.

Methodology

Homeowners insurance star ratings methodology

NerdWallet’s homeowners insurance ratings reward companies for customer-first features and practices. Ratings are based on weighted averages of scores in several categories, including financial strength, consumer experience, coverage and discounts. These ratings are a guide, but we encourage you to shop around and compare several insurance quotes to find the best rate for you. NerdWallet does not receive compensation for any reviews. Read our full ratings methodology for home insurance.

Homeowners insurance rates methodology

NerdWallet calculated median rates for 40-year-old homeowners from various insurance companies in ZIP codes across all 50 states and Washington, D.C. All rates are rounded to the nearest $5.

Sample homeowners were nonsmokers with good credit living in a single-family, two-story home built in 1984. They had a $1,000 deductible and the following coverage limits:

- $400,000 in dwelling coverage.

- $40,000 in other structures coverage.

- $200,000 in personal property coverage.

- $80,000 in loss of use coverage.

- $300,000 in liability coverage.

- $1,000 in medical payments coverage.

We made minor changes to the sample policy in cases where rates for the above coverage limits or deductibles weren’t available.

These are sample rates generated through Quadrant Information Services. Your own rates will be different.

Explore more on