What Is a HELOC, or Home Equity Line of Credit?

A HELOC lets you borrow against your home's value to access cash as needed.

Some or all of the mortgage lenders featured on our site are advertising partners of NerdWallet, but this does not influence our evaluations, lender star ratings or the order in which lenders are listed on the page. Our opinions are our own. Here is a list of our partners.

What is a HELOC?

A home equity line of credit, or HELOC, is a second mortgage that gives you access to cash based on the value of your home. You borrow against your equity, which is the home’s value minus the amount you owe (if anything) on your primary mortgage. While every lender has its own borrowing limit, you can usually borrow up to 85% of your equity.

You can make withdrawals from your line of credit up to your limit, which you’ll pay back in monthly installments. Since a HELOC is backed by your home, you’ll likely get a better interest rate than you would for an unsecured loan.

You could lose your home to foreclosure if you can’t keep up with payments, so it’s best to use your equity in a way that will build your wealth, like for home improvements.

HELOC & Home Equity Loans from our partners

on FourLeaf Federal Credit Union

670

$1,000,000

on FourLeaf Federal Credit Union

Key takeaways

A HELOC is a way to borrow cash from the value of your home.

HELOCs can have better interest rates than personal loans, credit cards and other kinds of unsecured debt.

Most HELOC lenders will let you borrow up to 85% of the value of your home (minus what you owe), though some have higher or lower limits.

You typically have 10 years to withdraw cash from a home equity line of credit. You only have to pay interest during this time.

After the draw period ends, you’ll typically have up to 20 years to pay back your principal plus interest.

Most HELOCs have a variable interest rate.

In order to qualify, lenders usually want you to have a credit score over 640.

How does a HELOC work?

HELOCs are broken up into two parts: the draw period, which you can think of as the borrowing period, and the repayment period.

Draw period: You can borrow money from the account, up to your approved limit. You have to make interest payments, but payments towards the principal are optional. This period typically lasts 10 years.

Repayment period: You can’t take out any more money, and you have to pay towards principal and interest until you’ve paid off what you’ve borrowed. If you chose not to pay towards the principal balance during the draw period, your minimum payments could go up by a lot. The length of the repayment period varies, but you’ll usually have up to 20 years.

How you’ll access your HELOC

You’ll have a few options to withdraw money from your HELOC, depending on what your lender offers. For example, you can access it via online transfer, with a bank card at an ATM or you can write checks from the account.

HELOC costs

In addition to interest, there are other costs to consider before taking out a HELOC.

Closing costs, which are often between 2% and 5% of the loan amount. Some lenders don’t charge closing costs at all, but be aware that this can require you to keep the line open for a certain amount of time.

Annual fees. Some lenders charge annual fees for HELOC customers, which are often around $50 per year.

HELOC requirements

Lender requirements will vary, but here's what you'll generally need to get a HELOC:

A debt-to-income ratio that's 43% or less.

A credit score of 640 or higher.

At least 15% home equity.

Today’s HELOC rates

Rates vary by lender, and the annual percentage rate, or APR, that you’re offered depends on factors such as your credit score, debt and the amount you need to borrow.

Most HELOC rates are indexed to a base rate called the prime rate, which is the lowest credit rate lenders are willing to offer their most attractive borrowers. Lenders consider a borrower’s profile, and add a margin to the prime rate to calculate a rate offer.

For example, if a lender adds a margin of 1.5% to a prime rate of 8.5%, that borrower’s rate will be 10%.

Prime Rate, Effective 12/11/25

Current prime rate — last changed Dec. 2025 | Prime rate last week | Prime rate in the past year — low | Prime rate in the past year — high | Projected median prime rate for 2026 |

|---|---|---|---|---|

6.75% | 6.75% | 6.75% | 7.5% | 6.4% |

Variable vs. fixed interest rates

Most HELOCs have adjustable interest rates. This means that as interest rates go up or down, your HELOC rate will change too.

Some lenders also offer a fixed-rate option. This lets you lock in your APR when you draw from your equity, which protects your loan from rising interest rates and can make long-term financial planning a little easier.

Getting the best HELOC rate

You should shop around with at least three lenders when looking for the best HELOC rate. Check your bank or mortgage provider to see if they offer discounts to existing customers. Also, take note of introductory offers like initial rates that will expire at the end of a given term.

After you’ve completed the application process, you’ll go through underwriting. This can take several weeks. Once you’ve been approved you’ll close on the loan and sign the paperwork.

Don't assume the price you paid at closing is what your home is worth today. If home prices in your area have gone up while you've owned your home, you may have more equity than you realize. You can estimate your home’s current value here.

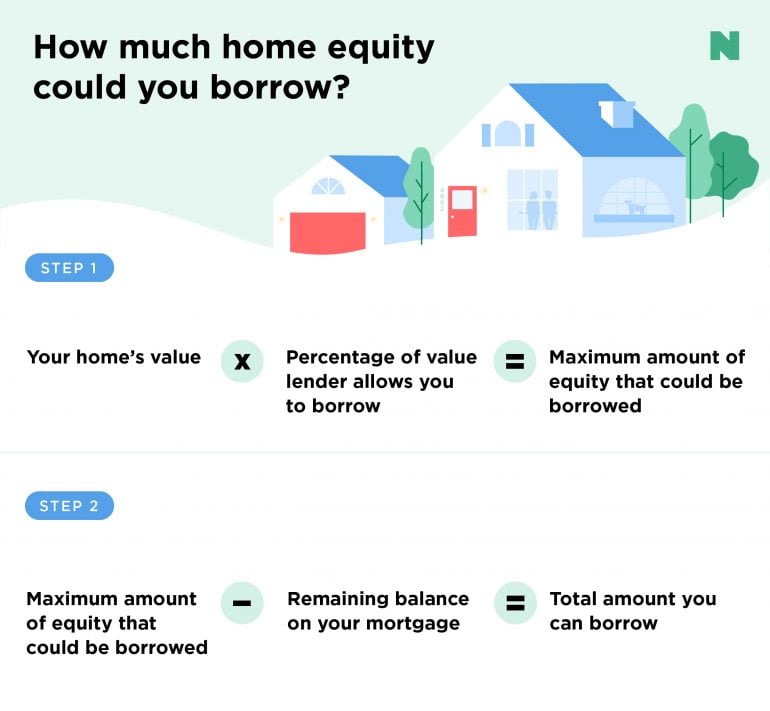

How much can you borrow with a HELOC?

The maximum amount of your home equity line of credit will vary based on the value of your home, the lender’s maximum borrowing limit and how much you owe on your mortgage. Two quick calculations can give you an idea of what you might be able to borrow with a HELOC.

Your home's current value x the percentage of value the lender allows you to borrow = the maximum amount of equity that could be borrowed.

Maximum amount of equity that could be borrowed - the remaining balance on your mortgage = the total amount you can borrow.

Say you have a home worth $300,000 with a balance of $200,000 on your first mortgage and your lender will allow you to access up to 85% of your home’s value. Multiplying the home's value ($300,000) by the percentage the lender will allow you to borrow (85%, or 0.85) gives you a maximum amount of $255,000 in equity that could be borrowed. Subtract the amount you still owe on your mortgage ($200,000) to get the total amount you can borrow with a HELOC — $55,000.

Is getting a HELOC a good idea?

Whether a home equity line of credit is a good idea really comes down to your goals and financial situation.

Pros

A HELOC is often used for home repairs and renovations, which can increase your home's value.

You could get a better rate with a HELOC than with an unsecured loan.

The interest on your HELOC may be tax-deductible if you use the money to buy, build or “substantially improve” your home, according to the IRS. This requirement expires after the 2025 tax year.

Cons

You run the risk of foreclosure if you can’t pay the loan.

A HELOC is not recommended if your income is unstable or if you won’t be able to afford payments if interest rates rise.

It may not be the best choice if you’re planning to move soon. One of the main benefits of a HELOC is its long borrowing and payment timeline, and you’ll have to pay it off entirely at the time of sale.

A HELOC may also not be the right choice if you aren’t looking to borrow much money (in which case the costs may not be worth it, and you should consider a low interest credit card instead), or if you intend to use it for basic needs, small purchases or expenses that don’t build personal wealth (like a new car or vacation).

Is it better to get a home equity loan or line of credit?

Choosing between a HELOC and a home equity loan depends on your financial situation and needs. The main difference between the two loan products is that a HELOC is a line of credit that you can draw from as needed, while a home equity loan is a lump sum that you receive all at once.

This makes HELOCs more suited to borrowers who want flexibility, while a home equity loan could be a fit for a borrower who wants the full loan amount upfront.

Another key difference is that HELOCs typically have variable interest rates, while home equity loans have fixed interest rates. Some borrowers prefer home equity loans because the payments are fixed and predictable.

What to do if you can’t keep up with your HELOC payments

Because most HELOCs have an adjustable rate, it’s possible your payments could exceed what you’d originally planned. If you can’t pay back what you’ve withdrawn, the lender could foreclose on your home. This makes it important to act fast if there’s a problem. Reach out to the lender to understand your options, and consider refinancing to lower your rate or change your payment terms.

» MORE FOR CANADIAN READERS: What is a home equity line of credit?

This article has been updated to reflect the most recent fact-checking as of September 3, 2025.