What Is a VantageScore?

A VantageScore is a credit score that is a competitor to FICO. It is used by lenders and landlords.

Many, or all, of the products featured on this page are from our advertising partners who compensate us when you take certain actions on our website or click to take an action on their website. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

Updated · 2 min read

Written by

Senior Writer & Content Strategist

Edited by

Lead Assigning Editor Co-written by

personal finance writer A VantageScore is a credit score jointly developed by the three major credit bureaus to predict how likely you are to repay borrowed money. It is used by lenders, landlords and financial institutions to evaluate creditworthiness.

Credit bureaus Experian, TransUnion and Equifax came up with the algorithm to produce VantageScore in 2006, competing against the better-known FICO scores. Initially, VantageScore was on a different scale from FICO, but the most recent revisions have a 300 to 850 scale, just like FICO’s.

VantageScore has begun to get lenders’ attention, and it is widely offered to consumers for free.

What matters most for VantageScores

The factors that matter most in FICO scores are also the most heavily weighted for VantageScores. With both, the single most important thing consumers can do to help their scores is to pay on time.

VantageScore prefers to express credit factors by how "influential" they are on consumers' credit scores. Here's how its VantageScore 3.0 model breaks down the factors:

- Payment history is “extremely influential.”

- Credit utilization (the percentage of credit limits in use) is “highly influential,” as is age and type of credit accounts.

- Total balances and debt are “moderately influential.”

- Recent credit behavior and amount of debt are “less influential.”

However, VantageScore has also expressed its scoring system using percentages, like FICO does.

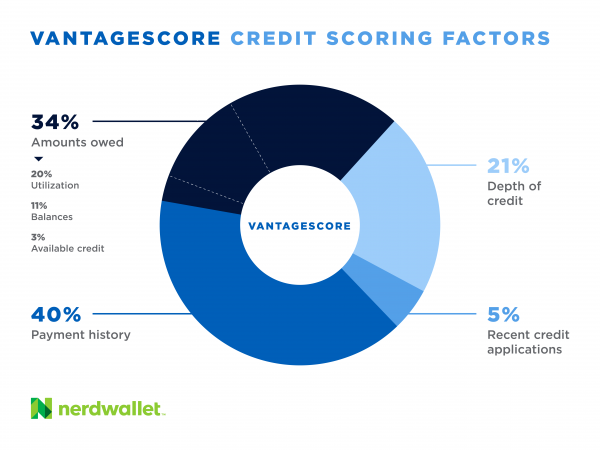

- Payment history makes up 40%, earning that "extremely influential" label.

- Credit utilization accounts for 20% — but this gets grouped into a broad "amounts owed" factor, along with balances at 11% and available credit, at 3%. Together, they account for 34%, which is seen as highly influential.

- Credit age and mix, also called "depth of credit," makes up 21%.

- Recent credit applications account for 5%.

Stress less. Track more.

See the full picture: savings, debt, investments and more. Smarter money moves start in our app.

VantageScore range

VantageScores are on a range of 300 to 850, which is the same range as a typical FICO. A score closer to the maximum 850 means better credit.

The proprietary VantageScore formula is applied to the data in your credit reports. Often the credit bureaus have slightly a different mix of data because not every creditor reports activity to all three, so your score may vary for each bureau.

VantageScore 4.0

VantageScore 4.0 is the latest version of the company's scoring model. It was introduced in 2017 but is not yet as widely used as the VantageScore 3.0 model.

The 4.0 model includes trended data, which looks at your credit usage over time, rather than taking a snapshot of one moment in time. Both the 4.0 and 3.0 VantageScore calculations exclude all paid and unpaid medical collections — however how much is owed or however long the debt has been in collections. The company says VantageScore 4.0 uses machine learning to help score consumers with little recent credit usage.

How to get a VantageScore

You can get a free VantageScore from NerdWallet and from some other personal finance sites. NerdWallet’s scores update every seven days and include a free credit report summary from TransUnion.

VantageScore also maintains a list of free credit score providers, along with information on which credit bureau’s score is offered and how often it updates.

VantageScore vs. FICO

It can take less time to establish a VantageScore than a FICO score. VantageScore can produce a score with just a month or two of a consumer opening a credit account. FICO scores require six months of credit history.

Another difference is that some consumers who can’t be scored by most FICO models because of a limited credit history can still get a VantageScore.

VantageScore 3.0 also:

- Ignores paid collections. (So does the FICO 9 and the FICO 10 and FICO 10T. FICO 9, 10 and 10T are not as widely used as FICO 8.

- Weighs late mortgage payments more heavily than other late payments, though all can damage your score.

- Allows just 14 days for rate-shopping for a car or mortgage (counting all inquiries in that time as one), compared with 45 days for FICO.

- Makes allowances for consumers affected by natural disasters.

If you are looking to track your score over time for credit-building purposes, a VantageScore will do the job as well as a FICO. The same behaviors influence them both.

The strategy for achieving a good score remains the same: pay bills on time and keep balances low. Conversely, paying late or using too much of your credit limit lowers your score.

Stress less. Track more.

See the full picture: savings, debt, investments and more. Smarter money moves start in our app. Article sources

NerdWallet writers are subject matter authorities who use primary,

trustworthy sources to inform their work, including peer-reviewed

studies, government websites, academic research and interviews with

industry experts. All content is fact-checked for accuracy, timeliness

and relevance. You can learn more about NerdWallet's high

standards for journalism by reading our

editorial guidelines.