Tax Credit vs. Tax Deduction

Tax deductions reduce your taxable income, but tax credits reduce your bill dollar for dollar.

Many, or all, of the products featured on this page are from our advertising partners who compensate us when you take certain actions on our website or click to take an action on their website. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

Tax credits and tax deductions may be the most satisfying part of preparing your tax return. Both reduce your tax bill but in very different ways.

Tax credits directly reduce the amount of tax you owe, giving you a dollar-for-dollar reduction of your tax liability. A tax credit valued at $1,000, for instance, lowers your tax bill by the corresponding $1,000.

Tax deductions, on the other hand, reduce the amount of your income subject to taxes. Deductions lower your taxable income by the percentage of your highest federal income tax bracket. So if you fall into the 22% tax bracket, a $1,000 deduction saves you $220.

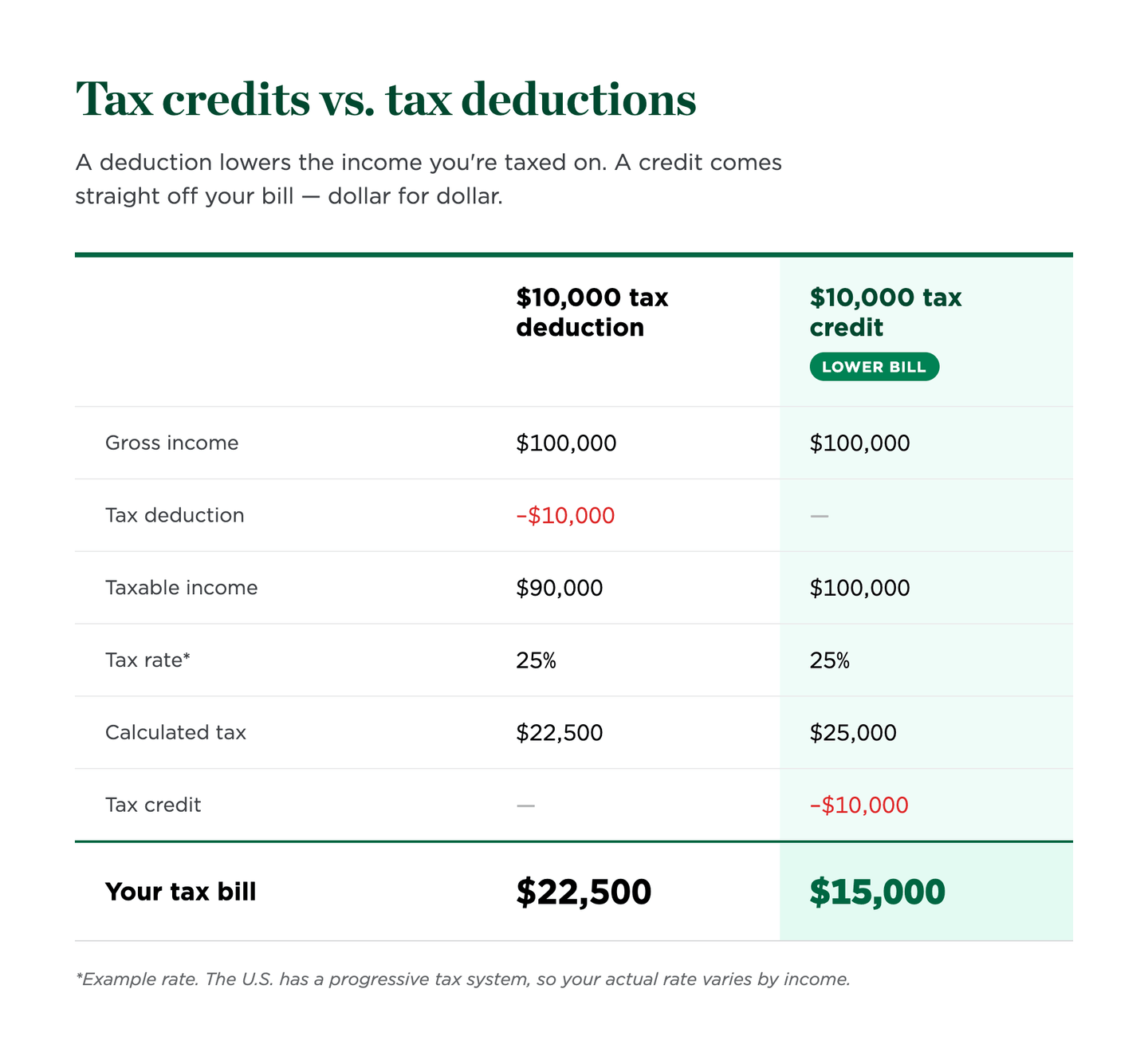

Tax credit vs. tax deduction example

The example scenario below illustrates the difference between how tax deductions and tax credits work. As you can see, both benefits can lower your taxes owed — but how they are applied differs. Generally, a tax credit can have a larger impact because it reduces your taxes owed instead of reducing the income you'll get taxed on. Still, it's worth learning about both types of benefits when looking for ways to catch a break on your taxes.

This image was created by our editorial team with the assistance of AI. It has been reviewed by our team for accuracy and quality.

The catch to tax credits

Some tax credits are nonrefundable. That means that if you don’t owe a lot in taxes to begin with, you don’t get the full value if the credits take your tax bill below zero. In other words, a $600 tax bill combined with a $1,000 nonrefundable credit doesn’t get you a $400 tax refund check — just a $0 tax bill.

Some tax credits are refundable. If you qualify to take refundable tax credits — things such as the earned income tax credit or the child tax credit — the value of the credit goes beyond your tax liability and can result in a refund check.

The IRS lays out specific criteria you must meet to qualify for both nonrefundable and refundable credits.

on Anthem Tax Services' website

on Alleviate Tax's website

A big decision about tax deductions

There are two types of tax-deduction strategies: taking the standard deduction or itemizing. It's also an either/or situation: you can do one or the other, but not both.

The standard deduction

The standard deduction is a one-size-fits-all reduction in the amount of your income that’s subject to tax. You don’t have to do anything to qualify for the standard deduction or provide any documentation. You can claim the standard deduction on Form 1040. The amount varies depending on your filing status. These are the deductions for 2026 (taxes filed in 2027).

Filing status | Deduction amount |

|---|---|

Single | $16,100. |

Married filing separately | $16,100. |

Head of household | $24,150. |

Married filing jointly | $32,200. |

Surviving spouse | $32,200. |

Itemizing

Itemizing allows you to take advantage of deductions such as home mortgage interest, medical expenses or charitable donations. If together your itemized deductions exceed the value of the standard deduction, you'll want to itemize so you pay less tax. You'll need to use the regular Form 1040 and Schedule A.

Just as with tax credits, taking certain deductions requires meeting certain qualifications based on your filing status, current life events and the amount of your income that’s taxable. Be sure you meet IRS criteria to qualify for both tax credits and deductions.

on Anthem Tax Services' website

on Alleviate Tax's website