We believe everyone should be able to make financial decisions with confidence. And while our site doesn’t feature every company or financial product available on the market, we’re proud that the guidance we offer, the information we provide and the tools we create are objective, independent, straightforward — and free.

So how do we make money? Our partners compensate us. This may influence which products we review and write about (and where those products appear on the site), but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services. Here is a list of our partners.

College-Bound Students Could Face $37,200 in Loans. Here’s How to Ease the Load

It's unclear what campuses will look like this fall, but students will still depend on loans to pay for college.

Many, or all, of the products featured on this page are from our advertising partners who compensate us when you take certain actions on our website or click to take an action on their website. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

Updated · 6 min read

How is this page expert verified?

NerdWallet's content is fact-checked for accuracy, timeliness and relevance. It undergoes a thorough review process involving writers and editors to ensure the information is as clear and complete as possible.

As NerdWallet’s Senior Economist, Elizabeth Renter spends her time analyzing economic trends and data to help people make more informed decisions about their personal finances. Her work has been cited by The New York Times, The Washington Post, the "Today" show, CNBC and elsewhere. Prior to joining NerdWallet in 2014, she was a freelance journalist. She received a Masters of Science in Finance and Economics from West Texas A&M University, and focused her elective coursework on macroeconomics and analytics. When she’s not at work, Elizabeth enjoys college football, old houses, traveling to old cities and powerlifting. She is based in Durham, North Carolina.

Des Toups was a lead assigning editor who supported the student loans and auto loans teams. He had decades of experience in personal finance journalism, exploring everything from car insurance to bankruptcy to couponing to side hustles.

NerdWallet ratingNerdWallet's ratings are determined by our editorial team. The scoring formula for student loan products takes into account more than 50 data points across multiple categories, including repayment options, customer service, lender transparency, loan eligibility and underwriting criteria.

Fixed APR

3.19-17.99%

College Ave Student Loans products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or M.Y. Safra Bank, FSB, member FDIC. All loans are subject to individual approval and adherence to underwriting guidelines. Program restrictions, other terms, and conditions apply. (1)All rates include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit. Variable rates may increase after consummation. (2)As certified by your school and less any other financial aid you might receive. Minimum $1,000. (3)This informational repayment example uses typical loan terms for a freshman borrower who selects the Flat Repayment Option with an 8-year repayment term, has a $10,000 loan that is disbursed in one disbursement and a 7.78% fixed Annual Percentage Rate (“APR”): 54 monthly payments of $25 while in school, followed by 96 monthly payments of $176.21 while in the repayment period, for a total amount of payments of $18,266.38. Loans will never have a full principal and interest monthly payment of less than $50. Your actual rates and repayment terms may vary. Information advertised valid as of 6/30/2025. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s), lowest advertised rates only available to the most creditworthy applicants and require selection of the Flat Repayment Option with the shortest available loan term.

Variable APR

4.24-17.99%

College Ave Student Loans products are made available through Firstrust Bank, member FDIC, First Citizens Community Bank, member FDIC, or M.Y. Safra Bank, FSB, member FDIC. All loans are subject to individual approval and adherence to underwriting guidelines. Program restrictions, other terms, and conditions apply. (1)All rates include the auto-pay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit. Variable rates may increase after consummation. (2)As certified by your school and less any other financial aid you might receive. Minimum $1,000. (3)This informational repayment example uses typical loan terms for a freshman borrower who selects the Flat Repayment Option with an 8-year repayment term, has a $10,000 loan that is disbursed in one disbursement and a 7.78% fixed Annual Percentage Rate (“APR”): 54 monthly payments of $25 while in school, followed by 96 monthly payments of $176.21 while in the repayment period, for a total amount of payments of $18,266.38. Loans will never have a full principal and interest monthly payment of less than $50. Your actual rates and repayment terms may vary. Information advertised valid as of 6/30/2025. Variable interest rates may increase after consummation. Approved interest rate will depend on creditworthiness of the applicant(s), lowest advertised rates only available to the most creditworthy applicants and require selection of the Flat Repayment Option with the shortest available loan term.

NerdWallet ratingNerdWallet's ratings are determined by our editorial team. The scoring formula for student loan products takes into account more than 50 data points across multiple categories, including repayment options, customer service, lender transparency, loan eligibility and underwriting criteria.

Fixed APR

3.19-16.99%

Lowest rates shown include the auto debit discount. Advertised APRs for undergraduate students assume a $10,000 loan to a student who attends school for 4 years and has no prior Sallie Mae-serviced loans. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment. Advertised APRs are valid as of 6/23/2025. Loan amounts: For applications submitted directly to Sallie Mae, loan amount cannot exceed the cost of attendance less financial aid received, as certified by the school. Applications submitted to Sallie Mae through a partner website will be subject to a lower maximum loan request amount. Miscellaneous personal expenses (such as a laptop) may be included in the cost of attendance for students enrolled at least half-time. Examples of typical costs for a $10,000 Smart Option Student Loan with the most common fixed rate, fixed repayment option, 6-month separation period, and two disbursements: For a borrower with no prior loans and a 4-year in-school period, it works out to a 10.28% fixed APR, 51 payments of $25.00, 119 payments of $182.67 and one payment of $121.71, for a Total Loan Cost of $23,134.44. For a borrower with $20,000 in prior loans and a 2-year in-school period, it works out to a 10.78% fixed APR, 27 payments of $25.00, 179 payments of $132.53 and one payment of $40.35 for a total loan cost of $24,438.22. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not.

Variable APR

4.37-16.49%

Lowest rates shown include the auto debit discount. Advertised APRs for undergraduate students assume a $10,000 loan to a student who attends school for 4 years and has no prior Sallie Mae-serviced loans. Interest rates for variable rate loans may increase or decrease over the life of the loan based on changes to the 30-day Average Secured Overnight Financing Rate (SOFR) rounded up to the nearest one-eighth of one percent. Advertised variable rates are the starting range of rates and may vary outside of that range over the life of the loan. Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period. To receive a 0.25 percentage point interest rate discount, the borrower or cosigner must enroll in auto debit through Sallie Mae. The discount applies only during active repayment for as long as the Current Amount Due or Designated Amount is successfully withdrawn from the authorized bank account each month. It may be suspended during forbearance or deferment. Advertised APRs are valid as of 6/23/2025. Loan amounts: For applications submitted directly to Sallie Mae, loan amount cannot exceed the cost of attendance less financial aid received, as certified by the school. Applications submitted to Sallie Mae through a partner website will be subject to a lower maximum loan request amount. Miscellaneous personal expenses (such as a laptop) may be included in the cost of attendance for students enrolled at least half-time. Examples of typical costs for a $10,000 Smart Option Student Loan with the most common fixed rate, fixed repayment option, 6-month separation period, and two disbursements: For a borrower with no prior loans and a 4-year in-school period, it works out to a 10.28% fixed APR, 51 payments of $25.00, 119 payments of $182.67 and one payment of $121.71, for a Total Loan Cost of $23,134.44. For a borrower with $20,000 in prior loans and a 2-year in-school period, it works out to a 10.78% fixed APR, 27 payments of $25.00, 179 payments of $132.53 and one payment of $40.35 for a total loan cost of $24,438.22. Loans that are subject to a $50 minimum principal and interest payment amount may receive a loan term that is less than 10 years. A variable APR may increase over the life of the loan. A fixed APR will not.

Credible lets you check with multiple student loan lenders to get rates with no impact to your credit score. Visit their website to take the next steps.

A 2020 high school graduate who depends on student loans for college could expect to borrow $37,200 in pursuit of a bachelor’s degree, according to NerdWallet analysis.

It’s unclear if and how the pandemic and resulting economic fallout could affect college enrollment numbers and costs this fall and beyond. But looking at the most recent available data can provide at least some direction for incoming college freshmen and their parents as they plan.

If prior years' enrollments are any indication, an expected 1.4 million of the nation’s high school graduates — 43% of them — could enroll in four-year colleges or universities. About half of those would take on student loan debt, according to our analysis of data from the National Center for Education Statistics. With a bachelor’s degree taking an average of about five years to complete, according to the National Student Clearinghouse, these students could be looking at $37,200 in student loans.

This loan total is a conservative estimate because our projections were limited to public colleges and universities. The projections did not include private institutions where loan amounts and the number of borrowers tend to be higher. The math also assumes the average loan amount per student will continue growing at the relatively slow pace seen in the latest available data.

"What college will look like in the fall and beyond is uncertain, but one thing is clear: Students will still need to take loans to pay for higher education," says Anna Helhoski, NerdWallet’s student loan expert. Though interest rates on federal student loans are expected to drop dramatically for the fall, "at best that shaves a few bucks off your monthly payment. I still strongly advise incoming college freshmen to consider how much they can expect to earn after college and to take on a manageable amount of debt."

Here are tips for students and parents to make education loans more manageable before, during and after college.

1. Exhaust all other reasonable funding sources

Loans are the most expensive way to pay for college. Other ways to lighten the load include grants and federal work-study, with eligibility determined annually. Plan to submit the Free Application for Federal Student Aid, known as the FAFSA, every year you’re in school.

Those attending school in fall 2020 should submit their FAFSA as soon as possible if they haven’t already, as state and institutional deadlines may have passed. Check with the financial aid office to be sure. For the 2020-21 school year, the official FAFSA deadline is June 30, 2021, to allow for students attending classes next summer. You’ll be eligible again for financial aid based on new income numbers when applications open in October for the following fall term.

Scholarships from colleges and organizations are available after freshman year as well. Minimize your overall debt load by keeping an eye out and applying for these sources of funding throughout the year, every year, not just as you prepare for your first semester.

2. Parents: Don’t sacrifice retirement savings

It can be tempting for parents to want to help reduce their child’s student loan debt by tapping into retirement savings. But depleting your retirement fund will only put you in a bind down the road. Unless your ideal retirement is asking your college-educated child to help with your living costs, keep on saving.

"It’s hard to tell any parent to put themselves first, but the reality is you can’t borrow money for retirement," Helhoski says. "But your children can borrow for college."

3. Borrow only what you need

You don’t have to accept all of the loans offered. Use your school’s net price calculator to determine how much you’ll need and use that as a guide. While you can use student loans to pay for living expenses — such as rent and groceries — be conservative. Every dollar you accept increases the total debt and monthly payment you’ll be saddled with after graduation.

As a rule of thumb, aim to limit borrowing so monthly payments aren’t more than 10% of your estimated, after-tax future income in your first year after college. A student loan affordability calculator can help you gauge an appropriate amount of debt to take on.

4. Make payments during school to save on interest

For unsubsidized federal student loans, parent PLUS loans and private loans, interest accrues while you’re in school. Because of this interest, any amount you can put toward your debt while in school will lessen the amount you ultimately pay.

Maintain an edge by making monthly interest payments, if possible. Depending on your loan balance and interest rate, these payments could be less than a night on the town.

5. Choose the right repayment plan before you graduate

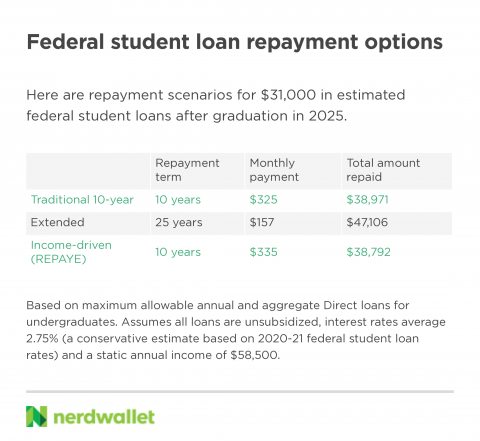

When college graduation is on the horizon, it’s time to start thinking about repayment. That $37,200 in projected student loans is a lot, so much so that the federal government won’t let most high school graduates borrow the entire amount from it directly. Currently, undergraduates can typically borrow a total of $31,000. Anything more will need to be supplemented with parent loans or private loans with a co-signer.

Fortunately, $31,000 represents a good portion of the total projected debt, and the federal government offers a few repayment options to make getting out from under school loans more manageable.

Borrowers will be automatically funneled into a standard 10-year repayment plan. And it’s not a bad option if you can handle the payments. You’ll generally pay your debt off in a shorter time frame, which means you’ll save on interest and pay less overall.

"Sticking to a standard repayment plan for 10 years is often the fastest and cheapest plan to pay off your debt, but it doesn’t take your other finances into account," Helhoski says. "An income-driven repayment plan is designed to adapt the amount you pay to an affordable amount. It’s also the plan you need to enroll in if you plan to pursue Public Service Loan Forgiveness."

Income-driven repayment options can have lower payments. They’re capped at 10% to 20% of discretionary income — payments can be as low as $0 — and your remaining balance can be forgiven after 20 to 25 years. In some scenarios, an income-driven repayment plan actually works out to slightly higher payments, but for someone who starts out with very low wages, payments can be $0.

The catch with income-driven plans: Interest keeps mounting even when payments are reduced, which means your balance could increase. And any forgiven amount is taxed as income.

If any of your loans come from private lenders, contact your lender directly to see what options are available. Refinancing at a lower interest rate may be an option if your credit has improved since you first took out the loans.

"When you’re figuring out how to pay for college, student loans feel abstract — something to worry about later," Helhoski says. "But when you get that first bill six months after you graduate, you’ll be thankful your younger self didn’t take on more debt than you could handle."

METHODOLOGY

Projected college enrollment, the percentage of students who are awarded student loans and debt amounts for the high school class of 2020, were calculated using data from the National Center for Education Statistics.

These projections represent a conservative estimate as they focus on public, four-year institutions only. Private nonprofit and for-profit institutions generally have higher student loan award rates and higher loan amounts, on average, when compared with public institutions.

The average student loan amounts in the group analyzed grew 5.3% annually from 2000 to 2005 and 8% annually from 2005 to 2010. They slowed dramatically from 2010 through 2017 to a rate of 1.6% year over year, which includes inflation and is the most recent data available. This analysis assumes this continued, most-recent conservative growth rate (1.6%) from 2018 on.

The analysis assumes a student who takes out student loans will borrow each year of their undergraduate career.

The calculations assume a five-year undergraduate career, based on estimates of the average time required to complete a bachelor’s degree from the National Student Clearinghouse.

Repayment estimates are based on all unsubsidized loans, each accruing 2.75% interest annually, where a total of $34,038 is owed on $31,000 in loans at the beginning of the repayment period. This interest rate is an extremely conservative one given rates set for the 2020-21 year. Income-based repayment is based on a static annual income of $58,500, based on a Class of 2018 estimate by the National Association of Colleges and Employers plus an average annual inflation of 2% to 2025.