Is an SBA 504 loan right for you?

An SBA 504 loan is a good fit if:

- You’re an established business, but can’t qualify for a bank loan.

- You have good credit and finances.

- You’re looking to finance equipment or real estate.

- You can create or retain at least one job for every $90,000 in CDC financing.

- You can wait for funding.

You should consider an alternative if:

- You’re a brand new business.

- You have a low credit score.

- You need funds quickly.

- You’re looking for working capital or to purchase inventory.

Not a fit? Click here to learn about top alternatives.

SBA 504 loans are an affordable way to finance equipment purchases and real estate projects. These loans are best for established businesses with strong credit who can’t qualify for a bank loan.

What is an SBA 504 loan?

An SBA 504 loan, or CDC/504 loan, is a small-business loan funded by Certified Development Companies and third-party lenders and backed by the U.S. Small Business Administration. These loans are designed to promote business growth and job creation through the purchase or upgrade of major fixed assets.

Min Credit

680

Max Loan Amount

$5,000,000

Min Time In Business

24 months

with NerdWallet Small Business

What can an SBA 504 loan be used for?

SBA 504 loans can be used to buy land, real estate, equipment, machinery, furniture or fixtures. They can also be used to build or upgrade facilities, including utilities, streets or parking lots. In specific scenarios, you can use a 504 loan to refinance debt or change ownership in your business.

You cannot, however, use an SBA 504 loan for working capital, to purchase inventory or to invest in real estate.

💡 Nerdy Insight

If your expenses don’t qualify, an SBA 7(a) loan may be a better fit, provided you can meet the eligibility requirements. Learn more about how the SBA 7(a) loan compares to the 504 loan.

How do SBA 504 loans work?

Unlike other types of SBA loans, 504 loans come from three different sources:

- A third-party lender. This is typically a bank or credit union.

- A Certified Development Company (CDC). CDCs are SBA-certified organizations that support economic development in their communities.

- The borrower. This is the small-business owner taking out the loan.

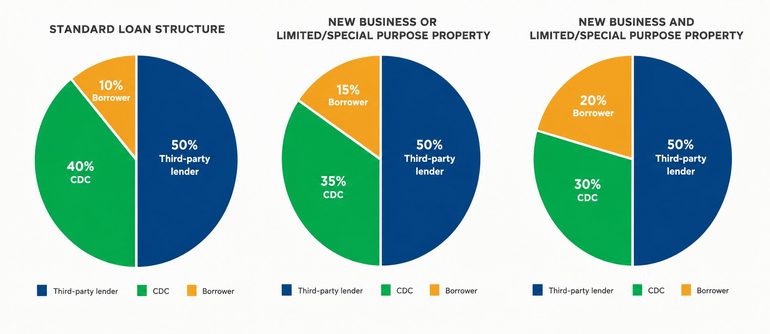

In most cases, the third-party lender provides 50% of the loan, the CDC provides 40% and the borrower provides 10% in the form of a down payment, sometimes called an equity injection. The loan structure may change, however, based on certain circumstances.

According to the SBA, a new business refers to any company in operation for less than two years. A limited or special purpose property, on the other hand, is a property with “a unique physical design, special construction materials or a layout that restricts its utility to the use for which it was built.” Examples include bowling alleys, farms, gas stations, hotels, theaters and wineries, among others.

Regardless of the specific structure, the SBA provides a 100% guarantee on the CDC portion of all 504 loans.

SBA 504 loan rates and terms

SBA 504 loans offer long-term, fixed-rate financing. Your loan amount, interest rates and repayment terms will vary based on your individual business, as well as the CDC and bank you work with.

Loan amount | $25,000 to $5 million. Energy public policy projects and small manufacturers may be eligible for up to $5.5 million. |

Repayment terms | 10, 20 or 25 years, based on the remaining useful life of the property being financed. |

Interest rates | Rates are tied to the 10-year U.S. Treasury notes and are typically around 5% to 7% of the amount financed. |

Collateral | The equipment or property being financed serves as collateral. In some cases, borrowers may be asked to provide additional collateral. |

Fees | Fees typically include SBA, CDC and bank or credit union fees, which vary. These fees are baked into the total loan amount, so a business owner’s only upfront cost is the 10% down payment.* |

Funding speed | Varies, but generally ranges between 30 and 90 days. |

*For fiscal year 2026, which started on Oct. 1, 2025, the SBA will waive the annual- and guarantee fees for small manufacturers (North American Industry Classification System sectors 31 to 33).

For 504 loans of more than $50,000, the SBA will require you to take out hazard insurance on all assets being pledged as collateral. You’ll also be required to sign a personal guarantee stating that you’ll repay the business’s debt in the case of default.

How much do you need?

We'll start with a brief questionnaire to better understand the unique needs of your business. Once we uncover your personalized matches, our team will consult you on the process moving forward.

SBA 504 loan requirements

To qualify for an SBA 504 loan, you’ll need to meet general SBA loan requirements, criteria specific to the 504 loan program, as well as any additional requirements from your lender.

Standard SBA loan requirements include:

- Must be a for-profit business operating in the U.S.

- Business must be 100% owned by U.S. citizens or U.S. nationals.

- Must be a small business, as defined by the SBA.

- Must have sought out other forms of financing before turning to an SBA loan.

- Must be able to demonstrate the need for a loan and show the business purpose for which you’ll use the funds.

- Cannot be delinquent on any government loans, including federal student loans.

- Must be able to show your ability to repay the loan.

SBA 504 loan requirements include:

- Net worth of less than $20 million.

- Average net income of less than $6.5 million for the two years prior to the application.

- You must be financing a major fixed asset purchase, upgrade or other eligible use case.

- Your project must create or continue a certain number of jobs or meet other public policy goals.

Nonprofit organizations, life insurance companies, private clubs and businesses that primarily engage in lending, lobbying or legal gambling are not eligible to receive an SBA 504 loan.

Your CDC and bank lender will have specific criteria that you’ll need to meet as well. These criteria can vary, but it’s generally helpful to have:

- Two years in business.

- Credit score of 680+.

- At least $100,000 in annual revenue.

So far in fiscal year 2026, over 80% of 504 loans have gone to businesses with two or more years in operation.

How to get an SBA 504 loan

1. Find a lender

To get an SBA 504 loan, you'll need to find a Certified Development Company. These nonprofit economic development organizations will process your application, coordinate your financing and submit the loan package to the SBA. You can find a list of CDCs on the SBA’s website.

Once you’ve identified a CDC, they’ll work with you to confirm that you’re a good candidate for a 504 loan and help you find a third-party lender.

❗Keep in mind that CDCs are local organizations and tend to service only one or a few states. Learn more about how to find an SBA lender here.

2. Gather project information

Next, you’ll need to prepare information about the major fixed asset you’re going to purchase or upgrade. You may need to get quotes from a vendor or calculate overall project costs.

This will help determine how much financing you qualify for and how much of a down payment you need, as well as confirm that you meet all 504 loan requirements.

3. Complete SBA 504 loan application

The 504 loan process will require extensive documentation, but specifics may vary based on your lender. In general, you’ll be asked to provide:

- Business and personal tax returns.

- Business and personal financial statements (e.g., balance sheet, income statements).

- Business plan.

- Accounts payable and receivable.

- Contractor estimates (for construction loans).

- Cost documentation (for equipment loans).

- Existing debt schedule.

- Cash flow analysis.

- Description of owner/manager’s experience.

- Description of additional collateral.

- Real estate and/or equipment appraisal.

- SBA Form 1244, Application for Section 504 loan.

- SBA Form 413, Personal Financial Statement.

If your application is approved, SBA 504 loans typically take one to two months to close. But closing can take longer for larger and more complex purchases.

Alternatives to SBA 504 loans

If an SBA 504 loan isn’t right for you, consider:

- For faster SBA financing. If you need $500,000 or less, you might opt for an SBA Express loan. Although they have a smaller loan maximum, these SBA loans offer faster approval times.

- For new businesses or borrowers with bad credit. Look into SBA microloans for funding needs of $50,000 or less. Participating lenders have more flexible qualification requirements, but still offer competitive rates.

- For immediate financing needs. If you need financing as quickly as possible, consider online lenders. These lenders can offer funding in as little as 24 hours but will charge higher rates.

Frequently asked questions

How long does it take to get an SBA 504 loan?

It can take anywhere from 30 to 90 days from the time you apply for an SBA 504 loan to when your loan is funded. That time frame can stretch as long as six months for more complex projects, such as real estate purchases.

How much down payment do you need for an SBA 504 loan?

At a minimum, you’ll need a down payment of 10% of the total loan amount for an SBA 504 loan. If you’re a new business or you’re funding a special use property (like a gas station or hotel), you’ll need to provide a 15% down payment. If you’re both a new business and funding a special use property, you’ll need a 20% down payment.

Is it hard to get an SBA 504 loan?

It may be harder to get an SBA 504 loan than other types of SBA loans. The SBA 504 loan has unique program criteria, including a job creation/public policy goal requirement. You must also meet all the standard SBA loan requirements, including good credit and strong revenue.

Article sources

NerdWallet writers are subject matter authorities who use primary, trustworthy sources to inform their work, including peer-reviewed studies, government websites, academic research and interviews with industry experts. All content is fact-checked for accuracy, timeliness and relevance. You can learn more about NerdWallet's high standards for journalism by reading our editorial guidelines.

- 1.U.S. Small Business Administration. SOP 50 10. Accessed May 28, 2026.

- 2.U.S. Small Business Administration. 504 Fees for Fiscal Year 2026. Accessed May 28, 2026.

- 3.Code of Federal Regulations. § 120.861 and § 120.862. Accessed Oct 1, 2025.

- 4.U.S. Small Business Administration. 7(a) and 504 Segment Report.