Your credit scores are determined by several factors, such as paying your bills on time, how much credit you're using and how long you've used credit. Understanding what factors affect credit scores helps you plan the most effective way to build your credit and protect it.

» Get your free credit score from NerdWallet

Credit scoring companies calculate your scores from data in your credit reports. While they won’t reveal their exact formulas, they share the basic ingredients they use to calculate scores.

What affects your credit scores the most?

The two major scoring companies in the U.S., FICO and VantageScore, differ in how they weight the factors in the calculations, but they agree on the two factors that are most important: Payment history and credit utilization. Together, these two factors make up more than half of your credit scores.

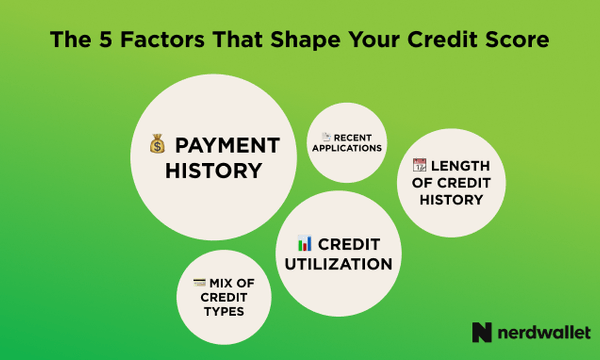

Here's a breakdown of all the factors that affect your scores:

Payment history: 35% to 40%

Your credit reports reveal your payment history, or whether you've consistently paid bills and other obligations on time. FICO says payment history accounts for 35% of your score. VantageScore says payment history counts for 40% of its 3.0 scoring model.

- What to do: Pay all bills on time. Late payments by 30 days or more can ding your scores — and the later you pay, the greater the damage. Set up autopay or calendar reminders so you don't miss due dates. You might also want to ask creditors to move your due dates so they better align with when you get paid.

» Learn more: What is credit and why is it important?

Credit utilization: 20% to 30%

The amount of your credit limit you use, expressed as a percentage, is called credit utilization. FICO says the amount of available credit you use counts for 30% of your score, while VantageScore 3.0 puts credit utilization at 20%.

Experts generally recommend the 30% utilization rule, meaning you use no more than 30% of your available credit. People with the highest scores tend to use much less than that.

- What to do: To lower your credit utilization, you can try things like setting balance alerts or making extra payments during the month.

The good news is that score damage from having high credit utilization can be reversed. Once you pay a high balance down and the creditor reports it to the credit bureaus, the damage disappears.

Meet MoneyNerd, your weekly news decoder

So much news. So little time. NerdWallet's new weekly newsletter makes sense of the headlines that affect your wallet.

Once you’ve mastered paying on time and keeping credit utilization low, turn your attention to other credit factors. These also affect your scores, though not nearly as much:

The length of time you’ve had credit: 15% to 21%

Credit scoring companies look at your credit age (sometimes called "depth of credit"), or how long you've been managing credit, to determine your score. The "older" your credit history, the better because they're relying on this long view to assess your ability to manage credit and debt. Their assessment informs decisions about whether to lend you money in the future.

- What to do: Keep old accounts open unless there is a compelling reason to close them, such as an annual fee on a card you no longer use. You also might be able to help yourself by becoming an authorized user on a trusted person's credit card. Look for someone with a long credit history and an excellent payment record.

The kinds of credit you have, or credit mix: 10% to 21%

It's best to have a mix of installment accounts — those with a set number of equal payments, such as car payments or mortgages — and credit card accounts.

Having a good mix of at least five accounts is a sweet spot for credit scoring. Anything less can create a thin credit file, which can make generating a score difficult.

- What to do: Don't open accounts just to "game" your score. Instead, fill in the gaps naturally. When you're ready to borrow, take that moment to improve your mix. For example, if you only have a student loan or auto loan, a credit card can help. But make sure your credit habits are strong before adding another account.

The length of time since you've applied for new credit: 5% to 11%

Each application that causes a hard inquiry on your credit may take a few points off your score.

- What to do: Space new applications out by at least six months to keep your score healthy and growing.

Factors that don't affect your credit score

Checking your own score

If you get your score through your bank or a free credit score service, it does not affect your score. That's because checking your own score is considered a soft pull on your credit. You can check it as many times as you want with no impact to your score.

Rent and utility payments

In most cases, your rent payments and your utility payments are not reported to the credit bureaus, so they do not count toward your score.

The exception is if you use a rent-reporting service or if you are late on utility payments. The utility company may charge it off or sell it to a collector, who can report it to the credit bureaus and hurt your score.

Some products, such as Experian Boost, allow you to add utility and eligible rent payment information to your Experian credit report, which can influence your credit.

Income and bank balances

Credit reports list only credit accounts — not savings, checking or investment accounts — so other balances won't help (or hurt) your score.

Your age

Credit scoring companies don't take your age into account, but your age can still unofficially influence your scores.

Credit scoring companies review your credit reports to see how you’re doing on all these factors. Then they build your scores from that data. You can see the same things they do by checking your credit reports.

Focus your credit-building efforts on on-time payments and keeping balances low relative to credit limits, because those factors have the biggest effect on your scores.

» Next: Get your free credit reports

How to request your credit reports in Spanish

You can request your credit report in Spanish directly from each of the three major credit bureaus:

- TransUnion: Call 800-916-8800.

- Equifax: Visit the link or call 888-378-4329.

- Experian: Click on the link or call 888-397-3742.

Usted puede solicitar una copia de su informe crediticio (gratis y en español) de cada una de las tres principales agencias de crédito:

- TransUnion: Llame al 800-916-8800.

- Equifax: Visite el enlace o llame al 888-378-4329.

- Experian: Haga clic en el enlace o llame al 888-397-3742.

Meet MoneyNerd, your weekly news decoder

So much news. So little time. NerdWallet's new weekly newsletter makes sense of the headlines that affect your wallet.