Tracking your expenses on a regular basis can give you an accurate picture of where your money is going — and where you’d like it to go instead.

Then, by using a budget, you can accurately account for all the bills you need to pay going forward. But before you start plugging numbers into a spreadsheet or app, take a minute to list out each of your expenses.

Here’s how to get started.

1. Determine your monthly net income

How much money do you bring in each month? If you have a full-time salary or hourly job, look at your paychecks for the month. Your net income is how much money comes to you after any taxes, benefits and retirement withholdings. Once you know how much is coming in, you can start to figure out where it all goes.

» Nerd out with us! Take our quick reader survey to help us give you a better, Nerdier experience.

2. Check your account statements

Pinpoint your money habits by taking inventory of all of your accounts, including your checking account and all credit cards you have. Looking at your accounts will help you identify your spending patterns.

Your spending will consist of fixed and variable expenses. Fixed expenses are less likely to change from month to month. They include mortgage or rent, utilities, insurance and debt payments. You'll have more room to adjust variable expenses like food, clothing and travel.

3. Categorize your expenses

Begin by grouping your expenses into different categories. Categorizing your expenses will help you track how much you’re spending, and see where your money is going.

Some personal finance websites and credit cards automatically tag your purchases in categories like “department store” or “automotive” to help you identify themes. You might find that those impulse buys at Target are costing you a lot. Or maybe you’ll realize you’re paying for recurring subscription services, such as Spotify or Babbel.

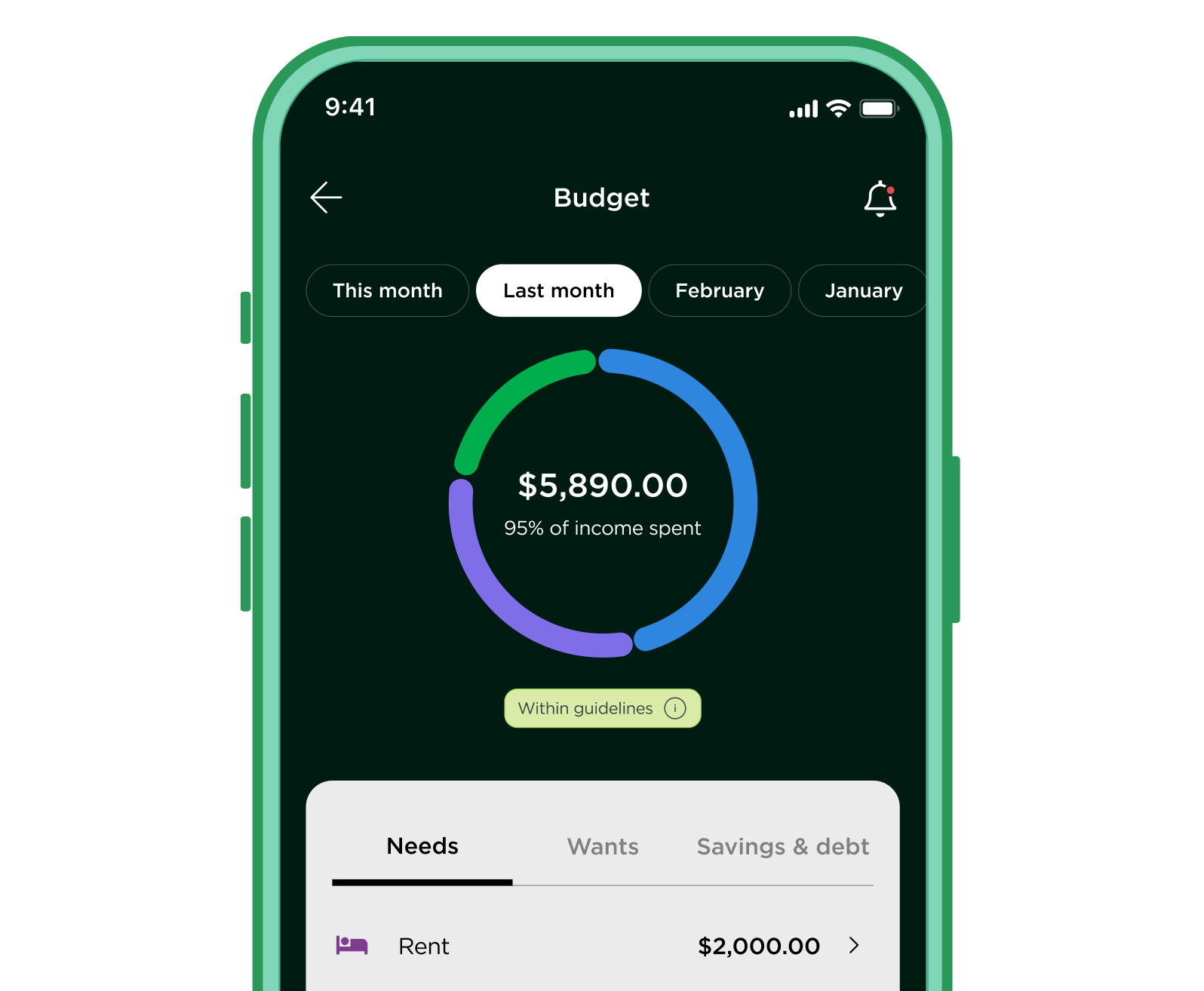

Another way to categorize your expenses is by organizing them into needs, wants and savings/debts using the 50/30/20 budget.

Meet MoneyNerd, your weekly news decoder

So much news. So little time. NerdWallet's new weekly newsletter makes sense of the headlines that affect your wallet.

4. Build a budget that works for your life

A spending plan can help you take actions to reduce your spending where necessary. The 50/30/20 budget is one option, but there are other budgeting methods that might be a better fit for you, such as the envelope system or zero-based budgeting. If you live in a high-cost-of-living area, the 60/30/10 budget might work best.

If you're using the 50/30/20 budget, divide your net income into three categories: 50% for needs, including minimum payments on debt; 30% for wants; and 20% for savings and debt paydown beyond minimums.

Sorting expenses into needs and wants can help you organize your budget and prioritize spending, especially if you need to cut costs to make room for savings or debt repayment. Here is a breakdown of each category in the 50/30/20 budget.

Needs

These are expenses you cannot avoid, including monthly bills. If you use the 50/30/20 , these should account for 50% of your spending. Necessities often include the following:

- Housing: Mortgage or rent; homeowners or renters insurance; property tax (if not already in the mortgage payment).

- Transportation: Car payment; gas; maintenance; auto insurance; public transportation.

- Health care: Health insurance; out-of-pocket medical costs.

- Life insurance.

- Utilities: Electricity; natural gas; water; sanitation/garbage; internet; phone.

- Groceries, toiletries, hair care and other essentials.

- Child care, child support or alimony.

- Minimum payments on debt: credit cards; student loans; other loans.

Wants

These expenses, also called discretionary expenses, may be harder to account for in a budget, as they don’t always come with a set monthly fee. If you use the 50/30/20 budget, wants can account for up to 30% of your spending.

- Clothing, jewelry, etc.

- Dining out, special meals in.

- Alcohol.

- Movie, concert and event tickets.

- Gym or club memberships.

- Travel expenses (airline tickets, hotels, rental cars, etc.).

- Cable or streaming packages.

- Self-care treats, such as spa visits and pedicures.

- Home decor.

Savings and debt repayment

This is the money you’re putting toward your retirement, emergency fund and other savings, and using to pay down high-interest credit cards and payday loans. It also includes anything over the minimum payment on other debts, such as your student loans and mortgage. In the 50/30/20 budget, this should account for 20% of your income:

- Emergency fund.

- Savings account.

- 401(k).

- Individual retirement account.

- Other investments.

- Extra debt payments on credit cards, mortgage, student loans, etc.

If you pay off your credit cards in full each month, classify the expenses according to what you buy — groceries under needs, for example. However, if you maintain a balance and are accruing interest and fees, list payments beyond the minimum under debt repayment.

» MORE: What's the range for average monthly expenses, and how do you compare?

Your budget builds itself, instantly

5. Use budgeting or expense-tracking apps

Consider using a budget app to track your expenses and save time. Budgeting apps are designed for on-the-go money management. They let you allocate a certain amount of spendable income each month, depending on what you’re taking in, and what you’re paying out.

These types of apps will work if you’re willing to log your purchases, put in the time and stick to your budget. The key is to regularly monitor your expenses. Consider setting a schedule for yourself, such as reviewing your budget on a monthly or quarterly basis.

NerdWallet has also identified the best expense tracking apps based on ratings and popularity among users.

6. Explore other expense-tracking methods

Not a fan of apps? A spreadsheet is another valuable money-tracking tool. You can find free budget spreadsheets online, and NerdWallet also offers a free online budget template.

If you have a more complex financial situation, such as investments or a small business, you might consider Quicken, which lets you import bank transactions and monitor your investments. Quicken offers customers cloud and desktop software with extensive budgeting and tracking features.

7. Monitor regularly

The key to successful tracking is to regularly monitor your income and expenses. By paying attention to where your money goes, you can identify patterns in spending that can help you make better financial decisions.

Set a schedule for yourself. Review your budget on a monthly or quarterly basis and make adjustments as necessary. An annual review may also be helpful to discover which months you tend to overspend.

8. Look for ways to lower your expenses

As you track, be ready to make adjustments. Lowering the big bills in your life, like the cost of housing, vehicles and utilities, can make a significant impact on your budget.

Beyond that, look for additional ways to save money that can give you some breathing room.

If you’ve exhausted your options for lowering expenses, you can try to make money to add more cash into your budgeting equation. You could take on a side gig, sell stuff online or explore money-making apps.

Your budget builds itself, instantly