If you apply for a loan or a credit card, forgetting your credit is frozen, your application likely won’t be approved. That’s because a credit freeze blocks anyone from accessing your credit reports, and a potential lender is unlikely to extend credit without a credit check. That means the freeze is doing its job.

Some good news: The failed application won’t hurt your credit — there was no hard inquiry on your credit because your file couldn’t be accessed. You'll just need to unfreeze and apply again.

» Learn how to unfreeze your credit at all three bureaus

How to check if your credit is frozen

Here’s how to find out at each credit bureau whether your credit is already frozen.

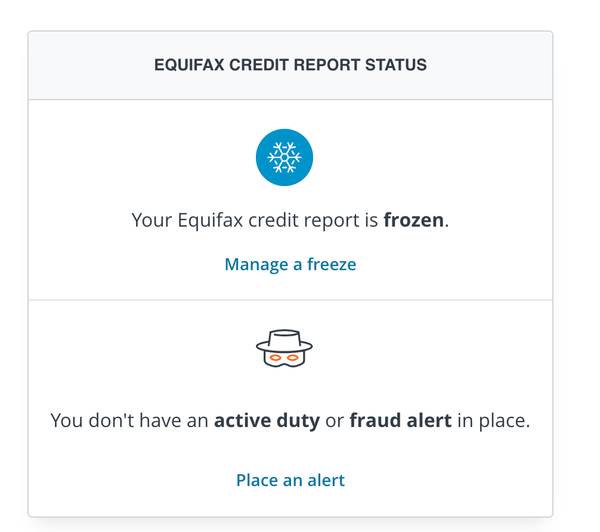

Equifax

The easiest way to check if you have a credit freeze in place is to log into your myEquifax account. When you log in at myEquifax.com, you can view your freeze status.

If you don’t have an account, or simply would rather use the phone, call 888-298-0045 and follow the prompts to verify your identity. If your credit report is not frozen, you will only hear options for freezing it. If it is frozen, you will hear only options for unfreezing.

» Learn how to manage an Equifax credit freeze

Meet MoneyNerd, your weekly news decoder

So much news. So little time. NerdWallet's new weekly newsletter makes sense of the headlines that affect your wallet.

TransUnion

If you already have a TransUnion account, the fastest way to check is online at the TransUnion website. You’ll need your username and password. After you log in, click on the “Credit Freeze” tile to see whether your account is frozen.

You can also call 800-916-8800. You’ll go through a verification process before you can get the information. Be prepared to provide information like your date of birth, address and Social Security number.

» Learn how to manage a TransUnion credit freeze

Experian

You can go online to Experian’s “Security Freeze Center” page, which looks like this:

You can also call 888-397-3742 and follow the prompts. You will be asked for your Social Security number. That, plus the number you are calling from, will be used to identify you and you'll be given the option to unfreeze if your account is frozen, or to freeze if the account is not frozen.

» Learn how to manage an Experian credit freeze

Frequently Asked Questions

What are my options for unfreezing credit?

You have two options for thawing your credit. You can choose to lift the freeze for a specified time, and it will automatically be reinstated at the end of the period. This is a hassle-free way to make sure your credit stays safe when you’re making a purchase that requires a credit check. You can also manually add the freeze back when your purchase is complete. You can also unfreeze permanently, but that leaves you vulnerable to criminals opening accounts in your name.

How long should I lift the freeze?

For a credit card or loan application, unfreezing your credit for a week or two should suffice. For a mortgage application, keep your credit thawed through your closing date.

How do I refreeze my credit?

If you lifted the freeze temporarily, your security freeze will be automatically applied at the end of the time period you selected. If you permanently lifted the freeze, you can refreeze just as you would if you were freezing your credit for the first time.

Can I get approved with a freeze in place?

In general, you will not get approved for credit or loans with a freeze in place. Creditors routinely check your credit before making a decision on an application. If they can’t see it, they won't approve you.

There are a few exceptions: You might slide through if you don’t have your credit frozen at all three bureaus, and the creditor checks the one where your credit is not frozen, or if you apply for a “no credit-check” product.

What if my mortgage closing is late and my credit refroze?

Most mortgage lenders recheck your credit just before closing. If your temporary thaw expires before then, you can unfreeze your credit and set a new date for the freeze to be reinstated.