A home equity loan is one way to tap into your home's value without having to sell it. As you make mortgage payments on the property and its value appreciates with time, the share of the home that you actually own — your equity — grows. By taking out a home equity loan, you convert that equity back into debt in exchange for cash.

HELOC & Home Equity Loans from our partners

at Rocket Mortgage, LLC

Rocket Mortgage

Min. credit score

680

Max. loan amount

$350,000

at Spring EQ

Spring EQ

Min. credit score

640

Max. loan amount

$500,000

at Better

Better

Min. credit score

640

Max. loan amount

$500,000

at Farmers Bank of Kansas City

Farmers Bank of Kansas City

Min. credit score

660

Max. loan amount

$250,000

at Splash

Splash

Min. credit score

670

Max. loan amount

$250,000

HELOC & Home Equity Loans from our partners

at Spring EQ

Spring EQ

Min. credit score

640

Max. loan amount

$500,000

at Farmers Bank of Kansas City

Farmers Bank of Kansas City

Min. credit score

660

Max. loan amount

$250,000

at Splash

Splash

Min. credit score

670

Max. loan amount

$250,000

Home equity loans are a popular choice for homeowners who want to take on some kind of home improvement project. You can use your money however you see fit, but it’s recommended that you reserve it for expenses that help build wealth, such as renovations that will grow your home’s value.

Because your home is the collateral for an equity loan, failure to repay could put you at risk of foreclosure. If you're considering a home equity loan, here's what you should know.

What is a home equity loan?

A home equity loan allows you to tap into some of your home’s equity for cash, which you receive in the form of a lump-sum payment that you pay back at a fixed interest rate over an agreed period of time. This is typically from five to 30 years.

A home equity loan generally allows you to borrow around 80% to 85% of your home’s value, minus what you owe on your mortgage. Some lenders allow you to borrow significantly more — even as much as 100% in some instances.

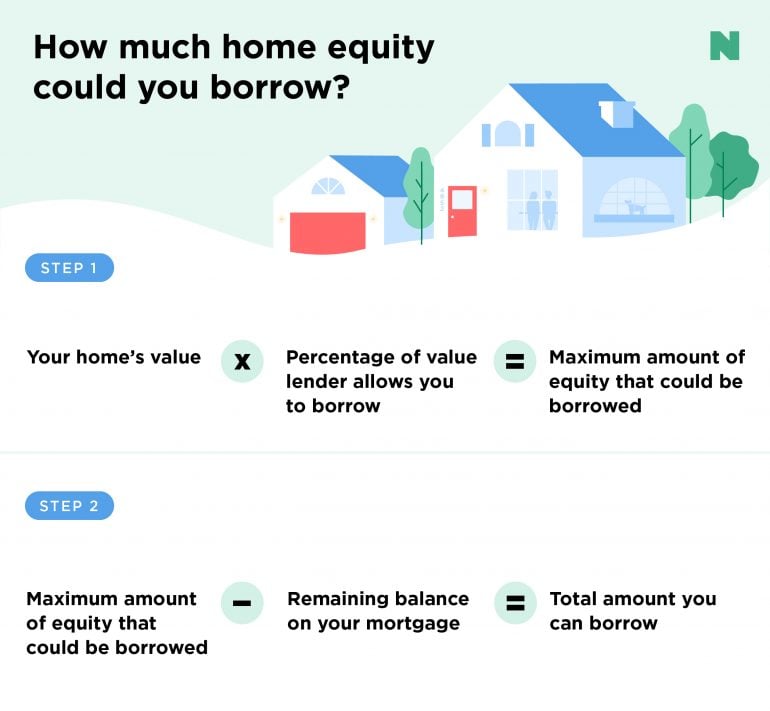

Calculating your maximum loan amount

Say your home is worth $350,000, your mortgage balance is $200,000, and your lender allows you to borrow up to 85% of your home’s value.

Multiply your home’s value by the percentage that you can borrow:

$350,000 × 0.85 = $297,500

Then, subtract your remaining mortgage balance:

$297,500 − $200,000 = $97,500

This gives you your estimated maximum loan amount — in this case, $97,500.

Alternatively, you can ditch the math and use our home equity loan calculator.

Home equity loan rates in 2026

Most home equity loan rates are indexed to an industry base rate called the prime rate. This represents the lowest credit rate lenders are able to offer their most attractive borrowers, though most lenders will add a margin to calculate their final rate offer. For example, if a lender applies a margin of 1.45% to a prime rate of 6.75%, that borrower’s home equity loan rate will be 8.20%.

This margin varies among lenders, so it’s in your best interest to shop around for quotes. No matter which lender you choose, borrowers with higher credit scores and lower debt-to-income ratios are more likely to qualify for the best rates.

Prime Rate, Effective 12/11/25

Current prime rate — last changed Dec. 2025 | Prime rate last week | Prime rate in the past year — low | Prime rate in the past year — high | Projected median prime rate for 2026 |

|---|---|---|---|---|

6.75% | 6.75% | 6.75% | 7.5% | 6.8% |

» MORE: Compare home equity loan rates

Ways to get the best home equity loan rates

When you’re shopping for a home equity loan, it’s smart to make sure your financials are in as good a shape as possible. This means pulling your credit reports from the three main credit reporting agencies — Experian, Equifax and TransUnion — and addressing any errors you find. You might also pay down any larger balances, which has the added benefit of improving your debt-to-income ratio. This could also improve the rates you’re offered.

Once you’re feeling confident about your application, compare mortgage rates among at least three home equity loan lenders. Even small differences in the rate you pay could add up over your loan term. You may also want to consider other funding methods, including home equity lines of credit, cash-out refinances or personal loans, which may offer lower rates or terms that work better for you.

How does a home equity loan work?

Home equity loans are commonly known as “second liens” or “second mortgages.” They finance a portion of the total value of the home, with the property acting as collateral. You’ll receive the full amount at closing, and you’ll repay the home equity loan — principal and interest each month — at a fixed rate, which doesn’t affect your primary mortgage rate. Be sure that you can afford this second mortgage payment in addition to your current mortgage, as well as your other monthly expenses.

You’ll likely qualify for a better rate with a home equity loan than you would with a loan that isn’t secured by an asset. However, you’re also exposing yourself to risk because the lender can foreclose on your home if you can’t make your payments.

If you’re interested in a home equity loan, the first thing you’ll have to do is figure out how much you need to borrow. Unlike a home equity line of credit — or HELOC — which allows you to draw from a line of credit as needed, home equity loans require you to have a real sense of what your project is going to cost upfront. Once you know how much you’ll need, you’ll want to calculate the value of your equity relative to the value of the home.

Your next step is to shop around for a lender. It’s recommended that you reach out to more than one so you can find the best available rate and terms. NerdWallet's list of the top home equity loan lenders is a great place to start.

How to use a home equity loan

Homeowners can use a home equity loan for anything they like, but it’s wise to avoid using equity to finance purchases that can’t be recouped, like vacations. It’s better to leverage your equity in ways that will help build your wealth, such as consolidating and paying down high-interest debt.

A home equity loan is best used for a repair, renovation or project that will add to the value of the home. The interest paid on a home equity loan may be tax-deductible when the loan is used to improve your home. Interest is generally not deductible when the loan is used for other purposes.

Home equity loan requirements

Qualification requirements for home equity loans will vary by lender, but here's an idea of what you'll likely need to get approved:

- Home equity of at least 15% to 20%

- A credit score of 620 or higher

- Debt-to-income ratio of 43% or lower

In order to confirm your home's fair market value, your lender may also require an appraisal to determine how much you're eligible to borrow.

Home equity loan pros and cons

Whether a home equity loan is a good idea or not depends on your financial situation and what you plan to do with the money. Using your home as collateral carries substantial risk, so it's worth the time to weigh the pros and cons of a home equity loan.

Pros:

- Fixed rates provide predictable payments, which makes budgeting easier.

- You may get a lower interest rate than with a personal loan or credit card.

- If your mortgage rate is lower than current rates, you don’t have to give that up.

- If you use the loan for home improvements or renovation, the interest may be deductible.

Cons:

- Less flexibility than a HELOC.

- You’ll pay interest on the entire loan amount, even if you’re using it incrementally, such as for an ongoing remodeling project.

- You may have to pay closing costs.

- If you use the loan for something other than home improvements or renovation, the interest isn’t tax-deductible.

Home equity loans vs. alternatives

Home equity loans vs. HELOCs

Unlike the single lump sum of a home equity loan, a HELOC provides flexibility. There's still a total loan amount, but you only borrow what you need, then pay it off and borrow again. That also means you pay back a HELOC incrementally based on the amount you use rather than on the entire amount of the loan, like a credit card.

The other key difference is that HELOCs often have variable rates. Your rate could rise or fall over the life of the loan, making your payments less predictable. HELOC rates are sometimes discounted at the beginning of the loan. But after an introductory phase of around six to 12 months, the interest rate typically goes up. If you’re enticed by the predictable payments of a home equity loan but would prefer the flexible balance of a HELOC, consider exploring lenders that offer HELOCs with a fixed-rate option.

Features of the loan | HELOC | Home equity loan |

|---|---|---|

Loan funding | Borrowers can draw funds as needed, up to a certain limit (typically a percentage of their equity). | Borrowers receive a lump sum at closing (typically a percentage of their equity). |

Terms | Begins with a draw period (typically 10 years) with interest-only minimum payments, followed by a repayment period (often up to 20 years) that requires borrowers to pay back principal and interest. | Repayment periods are often up to 30 years. Minimum payments include both interest and principal. |

Rates | Variable, though some lenders offer a fixed-rate option. | Fixed. |

Borrowing limits | Borrowers can typically borrow between 80% and 85% of their equity in their home, though some lenders allow for more. Use NerdWallet's HELOC calculator for personalized details. | Borrowers can typically borrow between 80% and 85% of their equity in their home, though some lenders allow for more. Use NerdWallet’s home equity loan calculator for personalized details. |

Lenders |

Home equity loans vs. cash-out refinances

A cash-out refinance replaces your existing mortgage with a new, larger loan, allowing you to spend the difference. This means that you’ll have a new interest rate on your primary mortgage, which won’t be ideal if rates have risen since you initially bought your home. You’ll also have to pay closing costs.

Features of the loan | Cash-out refinance | Home equity loan |

|---|---|---|

Loan funding | Borrowers receive a lump sum a few days after closing. | Borrowers receive a lump sum at closing. |

Terms | The borrower’s mortgage terms will change. The new repayment period can be up to 30 years. | The terms of the borrower’s primary mortgage won’t change. Repayment periods are often up to 30 years. |

Rates | Changes the borrower’s primary mortgage rate. | Does not affect the borrower’s primary mortgage rate. |

Borrowing limits | Borrowers can typically borrow up to 80% of their equity in their primary home. Use NerdWallet’s cash-out refinance calculator to see how much you may be eligible to borrow. | Borrowers can typically borrow between 80% and 85% of their equity in their home, though some lenders allow for more. Use NerdWallet’s home equity loan calculator for personalized details. |

Lenders |

NerdWallet writer Isabella Angelos contributed to this story.

Explore more on